Loss aversion

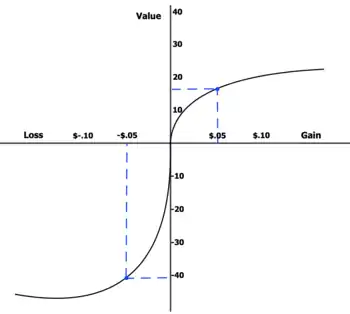

Loss aversion is the tendency to prefer avoiding losses to acquiring equivalent gains. The principle is prominent in the domain of economics. What distinguishes loss aversion from risk aversion is that the utility of a monetary payoff depends on what was previously experienced or was expected to happen. Some studies have suggested that losses are twice as powerful, psychologically, as gains.[1] Loss aversion was first identified by Amos Tversky and Daniel Kahneman.[2]

Loss aversion implies that one who loses $100 will lose more satisfaction than the same person will gain satisfaction from a $100 windfall. In marketing, the use of trial periods and rebates tries to take advantage of the buyer's tendency to value the good more after the buyer incorporates it in the status quo. In past behavioral economics studies, users participate up until the threat of loss equals any incurred gains. Recent methods established by Botond Kőszegi and Matthew Rabin[3] in experimental economics illustrates the role of expectation, wherein an individual's belief about an outcome can create an instance of loss aversion, whether or not a tangible change of state has occurred.

Whether a transaction is framed as a loss or as a gain is important to this calculation. The same change in price framed differently, for example as a $5 discount or as a $5 surcharge avoided, has a significant effect on consumer behavior.[4] Although traditional economists consider this "endowment effect", and all other effects of loss aversion, to be completely irrational, that is why it is so important to the fields of marketing and behavioral finance. Users in behavioral and experimental economics studies decided to cease participation in iterative money-making games when the threat of loss was close to the expenditure of effort, even when the user stood to further their gains. Loss aversion coupled with myopia has been shown to explain macroeconomic phenomena, such as the equity premium puzzle.[5]

Daniel Kahneman and his contributions.

Daniel Kahneman and his associate Amos Tversky originally coined the term loss aversion in 1979 in a paper on subjective probability. Kahneman published “Thinking, Fast and Slow” in 2013. This book covered psychological systems and economic strategies. Loss aversion being one of the main focuses throughout the book. “The response to losses is stronger than the response to corresponding gains” is Kahneman’s definition of loss aversion. There is an analogy mentioned of a coin toss, one side will lose you $100 and the other will win you $150. Which one is more attractive to you? The psychological benefit of winning the $150 or losing the $100? “Losses loom larger than gains” meaning that people by nature are aversive to losses. Loss aversion gets stronger as the stakes of a gamble or choice grow larger. Also consider you have a 50% chance of losing $100 and a 50% chance to win $200, one might be likely to take it, weighing that one positive outcome outweighs negative outcomes. If stakes were increased, raising the loss to $200 and the winnings to $100, loss aversion takes effect and the person is less likely to take the gamble. Prospect theory and utility theory follow and allow the person to feel regret and anticipated disappointment for that said gamble.

Kahneman goes into detail about two systems of the mind and how the psychological roles in loss aversion. System 1 being fast, intuitive, and emotional. This helps us make quick answers, think of substitutions, and helps our coherence in each situation. System 1 is who we are, it occurs as X. System 2 being slower, deliberate, and logical. This helps us find unintended answers, such as riddles or an algebraic problem. It also helps with forecasting and in-depth evaluations. System 2 is dependent on System 1, making System 2 Y. X predicts Y. The feelings of rejecting a gamble come from System 2, but the emotional responses come from System 1. Both systems follow a person’s adaption level, evaluating skills, and their need for immediate gratification. Maintained routines determine a person’s rational and adventurous choices, and shapes that person’s definitions of rational/adventurous.[6] Prospect theory incorporates adaption level, evaluating skills, and gratification. Prospect theory is the person’s most fundamental ways of functioning and thinking that dictate decisions made based on the potential impact of the decision.

A person’s adaption level is their evaluation from a neutral point where outcomes are based on personal reference points. Evaluation is defined by Kahneman as what we distinguish as valid and those, we conclude are likely bogus. Past associations play a contributing factor in how a person evaluates a choice. Our heuristic judgments come into play when past associations influence our present decisions. Evaluating is associated with the word bias because it tends to be a deciding factor in a “zero validity” situation. Bias tends to go hand in hand with seeking immediate gratification. Individuals seek patterns impulsively to gain that instant gratification of winning a gamble. Rationality is distinguished from intelligence when it comes to gratification and which system of the mind a person relies on. Functioning within system 1 makes an individual vulnerable and susceptible to gambling and accepting losses, without IQ being a factor.

System 1 and System 2 both go hand in hand when a person is seeking out a pattern. People tend not to focus on statistical standpoints but look for an answer in relation to a specific event occurring. When gambling, nobody expects a random process to be regular following a pattern. Most try to establish a rule to predict sequences that can occur within a game. Difficult outcomes are typically associated with blind luck and that there is no such thing as sequence of successes that are not random. This is referred to as an illusionary pattern.

Most people flock to the “sure thing”. People are drawn by specific priming and memories to pick an option that benefits them the most. Loss aversion is an instinct that involves a person comparing, reasoning, and ultimately making a choice. Loss aversion also occurs when a person is in a situation where they have an absence of a required skill. Heuristics (System 2) takes over and the person begins to problem solve and try to find a valid solution. Both systems work together to help a person avoid losses and gain what is possible.[7]

The endowment effect

Humans are theorized to be hardwired to be loss averse due to asymmetric evolutionary pressure on losses and gains: "for an organism operating close to the edge of survival, the loss of a day's food could cause death, whereas the gain of an extra day's food would not cause an extra day of life (unless the food could be easily and effectively stored)".[8] Loss aversion was first proposed as an explanation for the endowment effect—the fact that people place a higher value on a good that they own than on an identical good that they do not own—by Kahneman, Knetsch, and Thaler (1990).[9] Loss aversion and the endowment effect lead to a violation of the Coase theorem—that "the allocation of resources will be independent of the assignment of property rights when costless trades are possible" (p. 1326).

In several studies, the authors demonstrated that the endowment effect could be explained by loss aversion but not five alternatives: (1) transaction costs, (2) misunderstandings, (3) habitual bargaining behaviors, (4) income effects, or (5) trophy effects. In each experiment half of the subjects were randomly assigned a good and asked for the minimum amount they would be willing to sell it for while the other half of the subjects were given nothing and asked for the maximum amount they would be willing to spend to buy the good. Since the value of the good is fixed and individual valuation of the good varies from this fixed value only due to sampling variation, the supply and demand curves should be perfect mirrors of each other and thus half the goods should be traded. The authors also ruled out the explanation that lack of experience with trading would lead to the endowment effect by conducting repeated markets.

The first two alternative explanation are that under-trading was due to transaction costs or misunderstanding—were tested by comparing goods markets to induced-value markets under the same rules. If it was possible to trade to the optimal level in induced value markets, under the same rules, there should be no difference in goods markets.The results showed drastic differences between induced-value markets and goods markets. The median prices of buyers and sellers in induced-value markets matched almost every time leading to near perfect market efficiency, but goods markets sellers had much higher selling prices than buyers' buying prices. This effect was consistent over trials, indicating that this was not due to inexperience with the procedure or the market. Since the transaction cost that could have been due to the procedure was equal in the induced-value and goods markets, transaction costs were eliminated as an explanation for the endowment effect.

The third alternative explanation was that people have habitual bargaining behaviors, such as overstating their minimum selling price or understating their maximum bargaining price, that may spill over from strategic interactions where these behaviors are useful to the laboratory setting where they are sub-optimal. An experiment was conducted to address this by having the clearing prices selected at random. Buyers who indicated a willingness-to-pay higher than the randomly drawn price got the good, and vice versa for those who indicated a lower WTP. Likewise, sellers who indicated a lower willingness-to-accept than the randomly drawn price sold the good and vice versa. This incentive compatible value elicitation method did not eliminate the endowment effect but did rule out habitual bargaining behavior as an alternative explanation.

Income effects were ruled out by giving one third of the participants mugs, one third chocolates, and one third neither mug nor chocolate. They were then given the option of trading the mug for the chocolate or vice versa and those with neither were asked to merely choose between mug and chocolate. Thus, wealth effects were controlled for those groups who received mugs and chocolate. The results showed that 86% of those starting with mugs chose mugs, 10% of those starting with chocolates chose mugs, and 56% of those with nothing chose mugs. This ruled out income effects as an explanation for the endowment effect. Also, since all participants in the group had the same good, it could not be considered a "trophy", eliminating the final alternative explanation.[10]

Thus, the five alternative explanations were eliminated in the following ways:

- 1 and 2: Induced-value market vs. consumption goods market;

- 3: Incentive compatible value elicitation procedure;

- 4 and 5: Choice between endowed or alternative good.[11]

Questions about its existence

Multiple studies have questioned the existence of loss aversion. In several studies examining the effect of losses in decision making under risk and uncertainty no loss aversion was found.[12] There are several explanations for these findings: one, is that loss aversion does not exist in small payoff magnitudes (called magnitude dependent loss aversion by Mukherjee et al.(2017);[13] the other, is that the generality of the loss aversion pattern is lower than that thought previously. Finally, losses may have an effect on attention but not on the weighting of outcomes; as suggested, for instance, by the fact that losses lead to more autonomic arousal than gains even in the absence of loss aversion.[14] This latter effect is sometimes known as Loss Attention.[15]

Loss aversion may be more salient when people compete. Gill and Prowse (2012) provide experimental evidence that people are loss averse around reference points given by their expectations in a competitive environment with real effort.[16]

David Gal (2006) argued that many of the phenomena commonly attributed to loss aversion, including the status quo bias, the endowment effect, and the preference for safe over risky options, are more parsimoniously explained by psychological inertia than by a loss/gain asymmetry. Gal and Rucker (2018) made similar arguments.[17][18] Mkrva, Johnson, Gächter, and Herrmann (2019)[19] cast doubt on these critiques, replicating loss aversion in five unique samples while also showing how the magnitude of loss aversion varies in theoretically predictable ways. A paper by John Staddon,[20] citing Claude Bernard, pointed out that effects like loss aversion represent the average behavior of groups. There are many individual exceptions. To use these effects as something more than the results of an opinion poll means identifying the sources of variation, so that they can be demonstrated reliably in individual subjects. Group polling is rarely even attempted.

Alternatives to loss aversion: Loss attention

Loss attention refers to the tendency of individuals to allocate more attention to a task or situation when it involve losses than when it does not involve losses. What distinguishes loss attention from loss aversion is that it does not imply that losses are given more subjective weight (or utility) than gains. Moreover, under loss aversion losses have a biasing effect whereas under loss attention they can have a debiasing effect. Loss attention was proposed as a distinct regularity from loss aversion by Eldad Yechiam and Guy Hochman.[21] [22]

Specifically, the effect of losses is assumed to be on general attention rather than plain visual or auditory attention. The loss attention account assumes that losses in a given task mainly increase the general attentional resource pool available for that task. The increase in attention is assumed to have an inverse-U shape effect on performance (following the so called Yerkes-Dodson law).[21] The inverse U-shaped effect implies that the effect of losses on performance is most apparent in settings where task attention is low to begin with, for example in a monotonous vigilance task or when a concurrent task is more appealing. Indeed, it was found that the positive effect of losses on performance in a given task was more pronounced in a task performed concurrently with another task which was primary in its importance.[23] Loss attention is consistent with several empirical findings in economics , finance, marketing, and decision making. Some of these effects have been previously attributed to loss aversion, but can be explained by a mere attention asymmetry between gains and losses. An example is the performance advantage attributed to golf rounds where a player is under par (or in a disadvantage) compared to other rounds where a player is at an advantage.[24] Clearly, the difference could be attributed to increased attention in the former type of rounds.

Recently, studies have suggested that loss aversion mostly occur for very large losses[21] though the exact boundaries of the effect are unclear. On the other hand, loss attention was found even for small payoffs, such as $1.[22] This suggests that loss attention may be more robust than loss aversion. Still, one might argue that loss aversion is more parsimonious than loss attention.

Additional phenomena explained by loss attention:

Increased expected value maximization with losses – It was found that individuals are more likely to select choice options with higher expected value (namely, mean outcome) in tasks where outcomes are framed as losses than when they are framed as gains. Yechiam and Hochman[22] found that this effect occurred even when the alternative producing higher expected value was the one that included minor losses. Namely, a highly advantageous alternative producing minor losses was more attractive compared when it did not produce losses. Therefore, paradoxically, in their study minor losses led to more selection from the alternative generating them (refuting an explanation of this phenomenon based on loss aversion).

Loss arousal – Individuals were found to display greater Autonomic Nervous System activation following losses than following equivalent gains.[25] For example, pupil diameter and heart rate were found to increase following both gains and losses, but the size of the increase was higher following losses. Importantly, this was found even for small losses and gains where individuals do not show loss aversion. Similarly, a positive effect of losses compared to equivalent gains was found on activation of midfrontal cortical networks 200 to 400 milliseconds after observing the outcome.[26] This effect as well was found in the absence of loss aversion.[26]

Increased hot stove effect for losses – The hot stove effect is the finding that individuals avoid a risky alternative when the available information is limited to the obtained payoffs. A relevant example (proposed by Mark Twain) is of a cat which jumped of a hot stove and will never do it again, even when the stove is cold and potentially contains food. Apparently, when a given option produces losses this increases the hot stove effect,[27] a finding which is consistent with the notion that losses increase attention.

The out of pocket phenomenon – In financial decision making, it has been shown that people are more motivated when their incentives are to avoid losing personal resources, as opposed to gaining equivalent resources. Traditionally, this strong behavioral tendency was explained by loss aversion. However, it could also be explained simply as increased attention.[21][28]

The allure of minor disadvantages – In marketing studies it has been demonstrated that products whose minor negative features are highlighted (in addition to positive features) are perceived as more attractive.[29] Similarly, messages discussing both the advantages and disadvantages of a product were found to be more convincing than one-sided messages.[30] Loss attention explains this as due to attentional competition between options, and increased attention following the highlighting of small negatives, which can increase the attractiveness of a product or a candidate either due to exposure or learning.[21]

In nonhuman subjects

In 2005, experiments were conducted on the ability of capuchin monkeys to use money. After several months of training, the monkeys began showing behavior considered to reflect understanding of the concept of a medium of exchange. They exhibited the same propensity to avoid perceived losses demonstrated by human subjects and investors.[31] While a subsequent study suggested that the 2005 results were not indicative of loss aversion because of timing differences in the presentation of gains and losses to the monkeys,[32] a follow-up 2008 study by Laksminaryanan, Chen and Santos ruled out this alternative explanation.[33]

Expectation-based

Expectation-based loss aversion is a phenomenon in behavioral economics. When the expectations of an individual fail to match reality, they lose an amount of utility from the lack of experiencing fulfillment of these expectations. Analytical framework by Botond Kőszegi and Matthew Rabin provides a methodology through which such behavior can be classified and even predicted.[34] An individual's most recent expectations influences loss aversion in outcomes outside the status quo; a shopper intending to buy a pair of shoes on sale experiences loss aversion when the pair they had intended to buy is no longer available.[35]

Subsequent research performed by Johannes Abeler, Armin Falk, Lorenz Goette, and David Huffman in conjunction with the Institute of Labor Economics used the framework of Kőszegi and Rabin to prove that people experience expectation-based loss aversion at multiple thresholds.[36] The study evinced that reference points of people causes a tendency to avoid expectations going unmet. Participants were asked to participate in an iterative money-making task given the possibilities that they would receive either an accumulated sum for each round of "work", or a predetermined amount of money. With a 50% chance of receiving the "fair" compensation, participants were more likely to quit the experiment as this amount approached the fixed payment. They chose to stop when the values were equal as no matter which random result they received, their expectations would be matched. Participants were reluctant to work for more than the fixed payment as there was an equal chance their expected compensation would not be met.[37]

Within education

Loss aversion experimentation has most recently been applied within an educational setting in an effort to improve achievement within the U.S. Recent results from Program for International Student Assessment (PISA) 2009 ranked the US ranks #31 in math[38] and #17 in Reading.[39] In this latest experiment, Fryer et al. posits framing merit pay in terms of a loss in order to be most effective. This study was performed in the city of Chicago Heights within nine K-8 urban schools, which included 3,200 students. 150 out of 160 eligible teachers participated and were assigned to one of four treatment groups or a control group. Teachers in the incentive groups received rewards based on their students' end of the year performance on the ThinkLink Predictive Assessment and K-2 students took the Iowa Test of Basic Skills (ITBS) in March. The control group followed the traditional merit pay process of receiving "bonus pay" at the end of the year based on student performance on standardized exams. However, the experimental groups received a lump sum given at beginning of the year, that would have to be paid back. The bonus was equivalent to approximately 8% of the average teacher salary in Chicago Heights, approximately $8,000.

Methodology—"Gain" and "Loss" teachers received identical net payments for a given level of performance. The only difference is the timing and framing of the rewards. An advance on the payment and the re framing of the incentive as avoidance of a loss, the researchers observed treatment effects in excess of 0.20 and some as high as 0.398 standard deviations. According to the authors, 'this suggests that there may be significant potential for exploiting loss aversion in the pursuit of both optimal public policy and the pursuit of profits'.[40]

Utilizing loss aversion, specifically within the realm of education, has gotten much notoriety in blogs and mainstream media.

The Washington Post discussed merit pay in a 2012 article and specifically the study conducted by Fryer et al. The article discusses the positive results of the experiment and estimates the testing gains of those of the "loss" group are associated with an increase in lifetime earnings of between $37,180 and $77,740. They also comment on the fact that it didn't matter much whether the pay was tied to the performance of a given teacher or to the team to which that teacher was assigned. They state that "a merit pay regime need not pit teachers in a given school against each other to get results".[41]

Science Daily specifically covers the Fryer study stating that the study showed that "students gained as much as a 10 percentile increase in their scores compared to students with similar backgrounds – if their teacher received a bonus at the beginning of the year, with conditions attached." It also explains how there was no gain for students when teachers were offered the bonus at the end of the school year.

Thomas Amadio, superintendent of Chicago Heights Elementary School District 170, where the experiment was conducted, is quoted in this article stating "the study shows the value of merit pay as an encouragement for better teacher performance".[42]

Education weekly also weighs in and discusses utilizing loss aversion within education, specifically merit pay. The article states there are "few noteworthy limitations to the study, particularly relative to scope and sample size; further, the outcome measure was a 'low-stakes' diagnostic assessment, not the state test—it's unclear if findings would look the same if the test was used for accountability purposes. Still Fryer et al. have added an interesting tumbling element to the merit-pay routine".[43]

The Sun Times interviewed John List, Chairman of the University of Chicagos' department of economics. He stated "It's a deeply ingrained behavioral trait. .. that all human beings have—this underlying phenomenon that 'I really, really dislike losses, and I will do all I can to avoid losing something'." The article also speaks to only one other study to enhance performance in a work environment. The only prior field study of a "loss aversion" payment plan, they said, "occurred in Nanjing, China, where it improved productivity among factory workers who made and inspected DVD players and other consumer electronics". The article also covers a reaction by Barnett Berry, president of the Center for Teaching Quality, who stated "the study seems to suggest that districts pay 'teachers working with children and adolescents' in the same way 'Chinese factory workers' were paid for 'producing widgets'. I think this suggests a dire lack of understanding of the complexities of teaching."[44]

There has also been other criticism of the notion of loss aversion as an explanation of greater effects. Indeed, all of the noted findings in education can be explained simply by the additional attention to a task when it includes losses (i.e., loss attention), independently of the weighting to gains and losses. Larry Ferlazzo in his blog questioned what kind of positive classroom culture a "loss aversion" strategy would create with students, and what kind of effect a similar plan with teachers would have on school culture. He states that "the usual kind of teacher merit pay is bad enough, but a threatened 'take-away' strategy might even be more offensive".[45]

Neural aspect of loss aversion

In earlier studies, both bidirectional mesolimbic responses of activation for gains and deactivation for losses (or vica versa) and gain or loss-specific responses have been seen. While reward anticipation is associated with ventral striatum activation,[46][47] negative outcome anticipation engages the amygdala. However, only some studies have shown involvement of amygdala[48] during negative outcome anticipation but not others[49] which has led to some inconsistencies. It has later been proven that inconsistencies may only have been due to methodological issues including the utilisation of different tasks and stimuli, coupled with ranges of potential gains or losses sampled from either payoff matrices rather than parametric designs, and most of the data are reported in groups, therefore ignoring the variability amongst individuals. Thus later studies[50] rather than focusing on subjects in groups, focus more on individual differences in the neural bases by jointly looking at behavioural analyses and neuroimaging.

Neuroimaging studies on loss aversion involves measuring brain activity with functional magnetic resonance imaging (fMRI) to investigate whether individual variability in loss aversion were reflected in differences in brain activity through bidirectional or gain or loss specific responses, as well as multivariate source-based morphometry[51] (SBM) to investigate a structural network of loss aversion and univariate voxel-based morphometry (VBM) to identify specific functional regions within this network.

Brain activity in a right ventral striatum cluster increases particularly when anticipating gains. This involves the ventral caudate nucleus, pallidum, putamen, bilateral orbitofrontal cortex, superior frontal and middle gyri, posterior cingulate cortex, dorsal anterior cingulate cortex, and parts of the dorsomedial thalamus connecting to temporal and prefrontal cortex. There is a significant correlation between degree of loss aversion and strength of activity in both the frontomedial cortex and the ventral striatum. This is shown by the slope of brain activity deactivation for increasing losses being significantly greater than the slope of activation for increasing gains in the appetitive system involving the ventral striatum in the network of reward-based behavioural learning. On the other hand, when anticipating loss, the central and basal nuclei of amygdala, right posterior insula extending into the supramarginal gyrus mediate the output to other structures involved in the expression of fear and anxiety, such as the right parietal operculum and supramarginal gyrus. Consistent with gain anticipation, the slope of the activation for increasing losses was significantly greater than the slope of the deactivation for increasing gains.

Multiple neural mechanisms are recruited while making choices, showing functional and structural individual variability. Biased anticipation of negative outcomes leading to loss aversion involves specific somatosensory and limbic structures. fMRI test measuring neural responses in striatal, limbic and somatosensory brain regions help track individual differences in loss aversion. Its limbic component involved the amygdala (associated with negative emotion and plays a role in the expression of fear) and putamen in the right hemisphere. The somatosensory component included the middle cingulate cortex, as well as the posterior insula and rolandic operculum bilaterally. The latter cluster partially overlaps with the right hemispheric one displaying the loss-oriented bidirectional response previously described, but, unlike that region, it mostly involved the posterior insula bilaterally. All these structures play a critical role in detecting threats and prepare the organism for appropriate action, with the connections between amygdala nuclei and the striatum controlling the avoidance of aversive events. There are functional differences between the right and left amygdala. Overall, the role of amygdala in loss anticipation suggested that loss aversion may reflect a Pavlovian conditioned approach-avoidance response. Hence, there is a direct link between individual differences in the structural properties of this network and the actual consequences of its associated behavioral defense responses.

The neural activity involved in the processing of aversive experience and stimuli is not just a result of a temporary fearful overreaction prompted by choice-related information, but rather a stable component[52] of one's own preference function, reflecting a specific pattern of neural activity encoded in the functional and structural construction of a limbic-somatosensory neural system anticipating heightened aversive state of the brain. Even when no choice is required, individual differences in the intrinsic responsiveness of this interoceptive system reflect the impact of anticipated negative effects on evaluative processes, leading preference for avoiding losses rather than acquiring greater but riskier gains.

Individual differences in loss aversion are related to variables such as age,[53] gender, and genetic factors[54] affecting thalamic norepinephrine transmission, as well as neural structure and activities. Outcome anticipation and ensuing loss aversion involve multiple neural systems, showing functional and structural individual variability directly related to the actual outcomes of choices.

In a study, adolescents and adults are found to be similarly loss-averse on behavioural level but they demonstrated different underlying neural responses to the process of rejecting gambles. Although adolescents rejected the same proportion of trials as adults, adolescents displayed greater caudate and frontal pole activation than adults to achieve this. These findings suggest a difference in neural development during the avoidance of risk. It is possible that adding affectively arousing factors (e.g. peer influences) may overwhelm the reward-sensitive regions of the adolescent decision making system leading to risk-seeking behaviour. On the other hand, although men and women did not differ on their behavioural task performance, men showed greater neural activation than women in various areas during the task. Loss of striatal dopamine neurons is associated with reduced risk-taking behaviour. Acute administration of D2 dopamine agonists may cause an increase in risky choices in humans. This suggests dopamine acting on stratum and possibly other mesolimbic structures can modulate loss aversion by reducing loss prediction signalling.[55]

See also

- Capital Asset Pricing under Loss Aversion

- Equity premium puzzle

- Escalation of commitment

- List of cognitive biases

- Risk aversion

- Status quo bias

- Sunk cost fallacy

References

- Kahneman, D. & Tversky, A. (1992). "Advances in prospect theory: Cumulative representation of uncertainty". Journal of Risk and Uncertainty. 5 (4): 297–323. CiteSeerX 10.1.1.320.8769. doi:10.1007/BF00122574. S2CID 8456150.

- Kahneman, D. & Tversky, A. (1979). "Prospect Theory: An Analysis of Decision under Risk". Econometrica. 47 (4): 263–291. CiteSeerX 10.1.1.407.1910. doi:10.2307/1914185. JSTOR 1914185.

- Kőszegi, Botond; Rabin, Matthew (September 2007). "Reference-Dependent Risk Attitudes". American Economic Review. 97 (4): 1047–1073. doi:10.1257/aer.97.4.1047. ISSN 0002-8282.

- Levin, Irwin P., Sandra L. Schneider, and Gary J. Gaeth. "All frames are not created equal: A typology and critical analysis of framing effects." Organizational behavior and human decision processes 76.2 (1998): 149–188.

- Larson, F., List, J.A., & Metcalfe, R.D. (2016). Can Myopic Loss Aversion Explain the Equity Premium Puzzle? Evidence from a Natural Field Experiment with Professional Traders. NBER Working Paper No. 22605. https://www.nber.org/papers/w22605

- Tay, Shu Wen; Ryan, Paul; Ryan, C Anthony (2016-10-18). "Systems 1 and 2 thinking processes and cognitive reflection testing in medical students". Canadian Medical Education Journal. 7 (2): e97–e103. doi:10.36834/cmej.36777. ISSN 1923-1202. PMC 5344059. PMID 28344696.

- Kahneman, David (2013). Thinking, Fast and Slow. New York, NY: Farrar, Straus, and Giroux. pp. 10, 48, 119, 242–244, 271, 282–286, 289–299, 415–417. ISBN 978-0-374-53355-7.

- bayersatseguridad.com.ar http://bayersatseguridad.com.ar/docs/99byr4w.php?0732dc=loss-and-gain-meaning. Retrieved 2020-07-02. Missing or empty

|title=(help) - Kahneman, D.; Knetsch, J.; Thaler, R. (1990). "Experimental Test of the endowment effect and the Coase Theorem". Journal of Political Economy. 98 (6): 1325–1348. doi:10.1086/261737. JSTOR 2937761. S2CID 154889372.

- Kahneman, Daniel (1991). "Anomalies: The Endowment Effect, Loss Aversion, and Status Quo Bias" (PDF). Princeton.edu. Retrieved 2020-07-19.

- Kahneman, Daniel (December 1990). "Experimental Tests of the Endowment Effect and the Coase Theorem". The Journal of Political Economy. 98 (6): 1325–1348. doi:10.1086/261737. S2CID 154889372 – via Researchgate.net.

- Erev, Ert & Yechiam, 2008; Ert & Erev, 2008; Harinck, Van Dijk, Van Beest, & Mersmann, 2007; Kermer, Driver-Linn, Wilson, & Gilbert, 2006; Nicolau, 2012; Yechiam & Telpaz, in press

- Mukherjee, S., Sahay, A., Pammi, V.S.C., & Srinivasan, N. (2017). Is loss-aversion magnitude-dependent? Measuring prospective affective judgments regarding gains and losses. Judgment and Decision Making, 12(1), 81–89.

- Hochman & Yechiam, 2011

- Yechiam & Hochman, 2013

- Gill, David & Victoria Prowse (2012). "A structural analysis of disappointment aversion in a real effort competition". American Economic Review. 102 (1): 469–503. CiteSeerX 10.1.1.650.2595. doi:10.1257/aer.102.1.469. S2CID 7842439. SSRN 1578847.

- Gal, David; Rucker, Derek D. (2018-04-20). "The Loss of Loss Aversion: Will It Loom Larger Than Its Gain?". Journal of Consumer Psychology. 28 (3): 497–516. doi:10.1002/jcpy.1047. ISSN 1057-7408. S2CID 148956334.

- Gal, David; Rucker, Derek D. (2018-04-16). "Loss Aversion, Intellectual Inertia, and a Call for a More Contrarian Science: A Reply to Simonson & Kivetz and Higgins & Liberman". Journal of Consumer Psychology. 28 (3): 533–539. doi:10.1002/jcpy.1044. ISSN 1057-7408. S2CID 149965278.

- Mrkva, Kellen; Johnson, Eric J.; Gächter, Simon; Herrmann, Andreas (2020). "Moderating Loss Aversion: Loss Aversion Has Moderators, But Reports of its Death are Greatly Exaggerated" (PDF). Journal of Consumer Psychology. n/a (n/a): 407–428. doi:10.1002/jcpy.1156. ISSN 1532-7663. S2CID 212850733.

- Staddon, John (June 2019). "Object of Inquiry: Psychology's Other (Non-replication) Problem". Academic Questions. 32 (2): 246–256. doi:10.1007/s12129-019-09778-5. S2CID 150617862.

- Yechiam, E.; Hochman, G. (2013). "Losses as modulators of attention: Review and analysis of the unique effects of losses over gains". Psychological Bulletin. 139 (2): 497–518. doi:10.1037/a0029383. PMID 22823738. S2CID 10521233.

- Yechiam, E.; Hochman, G. (2013). "Loss-aversion or loss-attention: The impact of losses on cognitive performance". Cognitive Psychology. 66 (2): 212–231. doi:10.1016/j.cogpsych.2012.12.001. PMID 23334108. S2CID 1898874.

- Yechiam, E.; Hochman, G. (2014). "Loss attention in a dual task setting". Psychological Science. 25 (2): 494–502. doi:10.1177/0956797613510725. PMID 24357614. S2CID 76424.

- Pope, D.G; Schweitzer, M.E (2011). "Is Tiger Woods Loss Averse? Persistent Bias in the Face of Experience, Competition, and High Stakes". American Economic Review. 101: 129–157. CiteSeerX 10.1.1.183.2072. doi:10.1257/aer.101.1.129.

- Hochman, G.; Yechiam, E. (2011). "Loss aversion in the eye and in the heart: The Autonomic Nervous System's responses to losses". Journal of Behavioral Decision Making. 24 (2): 140–156. doi:10.1002/bdm.692.

- Gehring, W.J.; Willoughby, A.R (2002). "The medial frontal cortex and the rapid processing of monetary gains and losses". Science. 295 (2): 2279–2282. Bibcode:2002Sci...295.2279G. doi:10.1002/bdm.692. PMID 11910116.

- Yechiam, E.; Hochman, G.; Ashby, NJS. (2019). "Are we attracted by losses? Boundary conditions for the approach and avoidance effects of losses". Journal of Experimental Psychology: Learning, Memory, and Cognition. 45 (4): 591–605. doi:10.1037/xlm0000607. PMID 29999403. S2CID 38961229.

- Hochman, G.; Ayal, S.; Ariely, D. (2014). "Keeping your gains close but your money closer: The effect of prepayment on choice and behavior". Journal of Economic Behavior and Organization. 107: 582–594. doi:10.1016/j.jebo.2014.01.014.

- Ein-Gar, D.; Shiv, B.; Tormala, Z. (2012). "When blemishing leads to blossoming: The positive effect of negative information". Journal of Consumer Research. 38 (5): 846–859. doi:10.1086/660807. S2CID 144281463.

- Mamins, M.A; Brand, M.J; Hoeke, S.A.; Moe, J.C (1989). "Two-sided versus one-sided celebrity endorsements: The impact on advertising effectiveness and credibility". Journal of Advertising. 18 (2): 4–10. doi:10.1080/00913367.1989.10673146. S2CID 18785479.

- Dubner, Stephen J.; Levitt, Steven D. (2005-06-05). "Monkey Business". Freakonomics column. New York Times. Retrieved 2010-08-23.

- Silberberg, Alan; Roma, Peter G; Huntsberry, Mary E; Warren-Boulton, Frederick R; Sakagami, Takayuki; Ruggiero, Angela M; Suomi, Stephen J (March 2008). "On Loss Aversion in Capuchin Monkeys". Journal of the Experimental Analysis of Behavior. 89 (2): 145–155. doi:10.1901/jeab.2008.89-145. ISSN 0022-5002. PMC 2251327. PMID 18422015.

- Lakshminaryanan, Venkat; Chen, M.; Santos, Laurie (2008-11-01). "Endowment effect in capuchin monkeys (Cebus apella)". Philosophical Transactions of the Royal Society of London. Series B, Biological Sciences. 363 (1511): 3837–44. doi:10.1098/rstb.2008.0149. PMC 2581778. PMID 18840573. S2CID 2799860.

- Kőszegi, Botond; Rabin, Matthew (2006-11-01). "A Model of Reference-Dependent Preferences". The Quarterly Journal of Economics. 121 (4): 1133–1165. CiteSeerX 10.1.1.197.5740. doi:10.1093/qje/121.4.1133. ISSN 0033-5533.

- Kahneman, David (1972). "Subjective probability: A judgment of representativeness". Cognitive Psychology. 3 (3): 430–454. doi:10.1016/0010-0285(72)90016-3.

- Abeler, Johannes; Falk, Armin; Goette, Lorenz; Huffman, David (2011-04-01). "Reference Points and Effort Provision". American Economic Review. 101 (2): 470–492. CiteSeerX 10.1.1.472.7268. doi:10.1257/aer.101.2.470. ISSN 0002-8282. S2CID 32974.

- Voslinsky, Alisa (February 13, 2005). "Beliefs and social behavior in a multi-period ultimatum game". Frontiers in Behavioral Neuroscience. 9: 29. doi:10.3389/fnbeh.2015.00029. PMC 4327742. PMID 25762909.

- "PISA 2009 Results: What Students Know and Can Do: Student Performance in Reading, Mathematics and Science (Volume I)". 2009. Archived from the original on December 1, 2012.

- Fryer et al., "Enhancing the efficacy of teacher incentives through loss aversion" Archived September 15, 2012, at the Wayback Machine, "Harvard University", 2012

- Dylan Matthews (July 23, 2012). "Does teacher merit pay work? A new study says yes". Washington Post.

- "Student Scores Improve If Teachers Given Incentives Upfront". Science Daily. Aug 8, 2012.

- Amber M. Winkler (August 2, 2012). "Enhancing the Efficacy of Teacher Incentives through Loss Aversion: A Field Experiment". Education weekly.

- ROSALIND ROSSI (August 24, 2012). "Cash upfront the way to get teachers to rack up better student test scores, study finds". Chicago Sun-Times. Archived from the original on December 29, 2013.

- ""If you only have a hammer, you tend to see every problem as a nail" — Economists Go After Schools Again". 2012-07-22.

- N. Tobler, Philippe (1 October 2008). "Explicit neural signals reflecting reward uncertainty". Philosophical Transactions of the Royal Society of London. Series B, Biological Sciences. 363 (1511): 3801–11. doi:10.1098/rstb.2008.0152. PMC 2581779. PMID 18829433.

- Knutson, Brian (2005). "Distributed Neural Representation of Expected Value" (PDF). The Journal of Neuroscience. 25 (19): 4806–12. doi:10.1523/JNEUROSCI.0642-05.2005. PMC 6724773. PMID 15888656.

- Seymour, B; Daw, N; Dayan, P; Singer, T; Dolan, R (2007-05-02). "Differential Encoding of Losses and Gains in the Human Striatum". J Neurosci. 27 (18): 4826–31. doi:10.1523/JNEUROSCI.0400-07.2007. PMC 2630024. PMID 17475790.

- M Smith, Stephen (2009). "Correspondence of the brain's functional architecture during activation and rest". Proceedings of the National Academy of Sciences. 106 (31): 13040–13045. Bibcode:2009PNAS..10613040S. doi:10.1073/pnas.0905267106. PMC 2722273. PMID 19620724.

- Canessa, Nicola (September 4, 2013). "The Functional and Structural Neural Basis of Individual Differences in Loss Aversion" (PDF). The Journal of Neuroscience. 33 (36): 14307–17. doi:10.1523/JNEUROSCI.0497-13.2013. PMC 6618376. PMID 24005284.

- Xu, L.; Pearlson, G.; Calhoun, V. D. (2008). "Joint source based morphometry identifies linked gray and white matter group differences". NeuroImage. 44 (3): 777–789. doi:10.1016/j.neuroimage.2008.09.051. PMC 2669793. PMID 18992825.

- Canessa, Nicole (19 November 2016). "Neural markers of loss aversion in resting-state brain activity". NeuroImage. 146: 257–265. doi:10.1016/j.neuroimage.2016.11.050. PMID 27884798. S2CID 3396784.

- Barkley-Levenson, EE; Van Leijenhorst, L; Galván, A (2013). "Behavioral and neural correlates of loss aversion and risk avoidance in adolescents and adults". Dev Cogn Neurosci. 3: 72–83. doi:10.1016/j.dcn.2012.09.007. PMC 6987718. PMID 23245222.

- Senior, Carl; Lee, Nick; Braeutigam, Sven (2015-07-02). Society Organizations and the Brain: Building towards a UnifiedCognitive Neuroscience Perspective. ISBN 9782889195800.

- Barkley-Levenson, Emily (1 January 2013). "Behavioral and neural correlates of loss aversion and risk avoidance in adolescents and adults". Developmental Cognitive Neuroscience. 3: 72–83. doi:10.1016/j.dcn.2012.09.007. PMC 6987718. PMID 23245222.

Sources

- Ert, E.; Erev, I. (2008). "The rejection of attractive gambles, loss aversion, and the lemon avoidance heuristic". Journal of Economic Psychology. 29 (5): 715–723. doi:10.1016/j.joep.2007.06.003.

- Erev, I.; Ert, E.; Yechiam, E. (2008). "Loss aversion, diminishing sensitivity, and the effect of experience on repeated decisions". Journal of Behavioral Decision Making. 21 (5): 575–597. doi:10.1002/bdm.602. S2CID 143592144.

- Gal, D. (2006). "A psychological law of inertia and the illusion of loss aversion". Judgment and Decision Making. 1 (1): 23–32.

- Harinck, F.; Van Dijk, E.; Van Beest, I.; Mersmann, P. (2007). "When gains loom larger than losses: Reversed loss aversion for small amounts of money". Psychological Science. 18 (12): 1099–1105. doi:10.1111/j.1467-9280.2007.02031.x. PMID 18031418. S2CID 26981722.

- Hochman, G.; Yechiam, E. (2011). "Loss aversion in the eye and in the heart: The Autonomic Nervous System's responses to losses". Journal of Behavioral Decision Making. 24 (2): 140–156. doi:10.1002/bdm.692.

- Kahneman, D.; Knetsch, J.; Thaler, R. (1990). "Experimental Test of the endowment effect and the Coase Theorem". Journal of Political Economy. 98 (6): 1325–1348. doi:10.1086/261737. JSTOR 2937761. S2CID 154889372.

- Kahneman, D.; Tversky, A. (1979). "Prospect Theory: An Analysis of Decision under Risk". Econometrica. 47 (2): 263–291. CiteSeerX 10.1.1.407.1910. doi:10.2307/1914185. JSTOR 1914185.

- Kermer, D. A.; Driver-Linn, E.; Wilson, T. D.; Gilbert, D. T. (2006). "Loss aversion is an affective forecasting error". Psychological Science. 17 (8): 649–653. CiteSeerX 10.1.1.551.456. doi:10.1111/j.1467-9280.2006.01760.x. PMID 16913944. S2CID 1331820.

- McGraw, A. P.; Larsen, J. T.; Kahneman, D.; Schkade, D. (2010). "Comparing gains and losses". Psychological Science. 21 (10): 1438–1445. doi:10.1177/0956797610381504. PMID 20739673. S2CID 2290585.

- Nicolau, J. L. (2012). "Battle Royal: Zero-price effect vs relative vs referent thinking". Marketing Letters. 23 (3): 661–669. doi:10.1007/s11002-012-9169-2. S2CID 143589145.

- Silberberg, A.; et al. (2008). "On loss aversion in capuchin monkeys". Journal of the Experimental Analysis of Behavior. 89 (2): 145–155. doi:10.1901/jeab.2008.89-145. PMC 2251327. PMID 18422015.

- Tversky, A.; Kahneman, D. (1991). "Loss Aversion in Riskless Choice: A Reference Dependent Model". Quarterly Journal of Economics. 106 (4): 1039–1061. CiteSeerX 10.1.1.703.2614. doi:10.2307/2937956. JSTOR 2937956.

- Yechiam, E.; Hochman, G. (2013). "Losses as modulators of attention: Review and analysis of the unique effects of losses over gains". Psychological Bulletin. 139 (2): 497–518. doi:10.1037/a0029383. PMID 22823738. S2CID 10521233.

- Yechiam, E.; Telpaz, A. (2013). "Losses Induce Consistency in Risk Taking Even Without Loss Aversion". Journal of Behavioral Decision Making. 26 (1): 31–40. doi:10.1002/bdm.758.

- Canessa, Nicola; Crespi, Chiara; Baud-Bovy, Gabriel; Dodich, Alessandra; Falini, Andrea; Antonellis, Giulia; Cappa, Stefano F. (2017). "Neural markers of loss aversion in resting-state brain activity". NeuroImage. 146: 257–265. doi:10.1016/j.neuroimage.2016.11.050. PMID 27884798. S2CID 3396784.

- Barkley-Levenson, Emily E.; Van Leijenhorst, Linda; Galván, Adriana (2013). "Behavioral and neural correlates of loss aversion and risk avoidance in adolescents and adults". Developmental Cognitive Neuroscience. 3: 72–83. doi:10.1016/j.dcn.2012.09.007. PMID 23245222.

- Bulipipova, Ekaterina; Zhdanov, Vladislav; Simonov, Artem (2014). "Do investors hold that they know? Impact of familiarity bias on investor's reluctance to realize losses: Experimental approach". Finance Research Letters. 11 (4): 463–469. doi:10.1016/j.frl.2014.10.003.