Diminishing returns

In economics, diminishing returns is the decrease in the marginal (incremental) output a production process as the amount of a single factor of production is incrementally increased, while the amounts of all other factors of production stay constant.

| Part of a series on |

| Economics |

|---|

|

The law of diminishing returns states that in productive processes, increasing a factor of production by one, while holding all others constant ("ceteris paribus"), will at some point return lower output per incremental input unit.[1] The law of diminishing returns does not decrease the total production, a condition known as negative returns. Under diminishing returns, returns remain positive, though they approach zero.

The modern understanding of the law adds the dimension of holding other outputs equal, since a given process is understood to be able to produce co-products.[2] An example would be a factory increasing its saleable product, but also increasing its CO2 production, for the same input increase.

The law of diminishing returns is a fundamental principle of economics.[1] It plays a central role in production theory.[3]

History

The concept of diminishing returns can be traced back to the concerns of early economists such as Johann Heinrich von Thünen, Jacques Turgot, Adam Smith,[4] James Steuart, Thomas Robert Malthus, and David Ricardo. However, classical economists such as Malthus and Ricardo attributed the successive diminishment of output to the decreasing quality of the inputs. Neoclassical economists assume that each "unit" of labor is identical. Diminishing returns are due to the disruption of the entire productive process as additional units of labor are added to a fixed amount of capital. The law of diminishing returns remains an important consideration in farming.

Proposed on the cusp of the First Industrial Revolution, it was motivated with single outputs in mind. In recent years, economists since the 1970s have sought to redefine the theory, appropriate for the modern age.[2] Specifically, what assumptions can be made regarding input number, quality, substitution and complement, and output co-production, number and quality?

Example

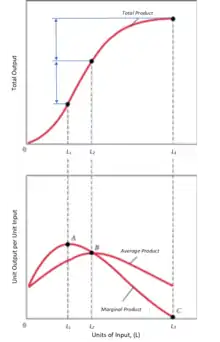

A common example is hiring more people on a factory floor. Given that the capital on the floor (production machines) is held constant, increasing from one employee to two is, theoretically, going to more than double production. This is increasing returns.

At some point, say, 50 employees, increasing the number of employees by two percent (from 50 to 51) would increase output by 2 percent. This is constant returns.

Look further along the production curve, say, 100 employees, floor space is getting crowded, and workers are getting in each other's way. Increasing the number of employees by 2 percent (from 100 to 102) would increase output by less than 2 percent. This is diminishing returns.

Through each of these examples, the floor space and capital of the factor remained constant. I.e. all other inputs were constant.

Mathematics

Signify

Increasing Returns:

Constant Returns:

Diminishing Returns:

Link with Output Elasticity

Start from the equation for the Marginal Product:

To demonstrate diminishing returns, two conditions are satisfied; marginal product is positive, and marginal product is decreasing.

Elasticity, a function of Input and Output, , can be taken for small input changes. If the above two conditions are satisfied, then .[5]

This works intuitively;

- If is positive, since negative inputs and outputs are impossible,

- And is positive, since a positive return for inputs is required for diminishing returns

- Then

- is relative change in output, is relative change in input

- The relative change in output is smaller than the relative change in input; ~input requires increasing effort to change output~

- Then

Returns and costs

There is an inverse relationship between returns of inputs and the cost of production, although other features such as input market conditions can also affect production costs. Suppose that a kilogram of seed costs one dollar, and this price does not change. Assume for simplicity that there are no fixed costs. One kilogram of seeds yields one ton of crop, so the first ton of the crop costs one dollar to produce. That is, for the first ton of output, the marginal cost as well as the average cost of the output is $1 per ton. If there are no other changes, then if the second kilogram of seeds applied to land produces only half the output of the first (showing diminishing returns), the marginal cost would equal $1 per half ton of output, or $2 per ton, and the average cost is $2 per 3/2 tons of output, or $4/3 per ton of output. Similarly, if the third kilogram of seeds yields only a quarter ton, then the marginal cost equals $1 per quarter ton or $4 per ton, and the average cost is $3 per 7/4 tons, or $12/7 per ton of output. Thus, diminishing marginal returns imply increasing marginal costs and increasing average costs.

Cost is measured in terms of opportunity cost. In this case the law also applies to societies – the opportunity cost of producing a single unit of a good generally increases as a society attempts to produce more of that good. This explains the bowed-out shape of the production possibilities frontier.

Justification

Ceteris Paribus

Part of the reason one input is altered ceteris paribus, is the idea of disposability of inputs.[6] With this assumption, essentially that some inputs are above the efficient level. Meaning, they can decrease without perceivable impact on output, after the manner of excessive fertiliser on a field.

If input disposability is assumed, then increasing the principal input, while decreasing those excess inputs, could result in the same 'diminished return', as if the principal input was changed certeris paribus. While considered as 'hard' inputs, like labour and assets, diminishing returns would hold true. In the modern accounting era where inputs can be traced back to movements of financial capital, the same case may reflect constant, or increasing returns.

It is necessary to be clear of the 'fine structure'[2] of the inputs before proceeding. In this, ceteris paribus is disambiguating.

See also

- Diminishing marginal utility, also not to be mistaken for 'diminishing returns'

- Diseconomies of scale, does not assume fixed inputs, and considers costs, thus differing from 'diminishing returns'

- Economies of scale

- Gold plating (project management)

- Learning curve and Experience curve effects

- Liebig's Law of the minimum

- Marginal value theorem

- Opportunity cost

- Returns to scale

- Pareto efficiency

- Submodular set function

- Sunk-cost fallacy

- Tendency of the rate of profit to fall

- Analysis paralysis

- Teamwork

- Amdahl's law

References

Citations

- Samuelson, Paul A.; Nordhaus, William D. (2001). Microeconomics (17th ed.). McGraw-Hill. p. 110. ISBN 0071180664.

- Shephard, Ronald W.; Färe, Rolf (1974-03-01). "The law of diminishing returns". Zeitschrift für Nationalökonomie. 34 (1): 69–90. doi:10.1007/BF01289147. ISSN 1617-7134.

- Encyclopædia Britannica. Encyclopædia Britannica, Inc. 26 Jan 2013. ISBN 9781593392925.

- Smith, Adam. The wealth of nations. Thrifty books. ISBN 9780786514854.

- Robinson, R. Clark (July 2006). "Math 285-2 - Handouts for Math 285-2 - Marginal Product of Labor and Capital" (PDF). Northwestern - Weinberg College of Arts & Sciences -Department of Mathematics. Retrieved 1 November 2020.

- Shephard, Ronald W. (1970-03-01). "Proof of the law of diminishing returns". Zeitschrift für Nationalökonomie. 30 (1): 7–34. doi:10.1007/BF01289990. ISSN 1617-7134.

Sources

- Case, Karl E.; Fair, Ray C. (1999). Principles of Economics (5th ed.). Prentice-Hall. ISBN 0-13-961905-4.