Stamp duty in the United Kingdom

Stamp duty in the United Kingdom is a form of tax charged on legal instruments (written documents), and historically required a physical stamp to be attached to or impressed upon the document in question.[1][2] The more modern versions of the tax no longer require a physical stamp.

| Taxation in the United Kingdom |

|---|

.svg.png.webp) |

| UK Government Departments |

| UK Government |

|

| Scottish Government |

| Welsh Government |

| Local Government |

|

History of UK stamp duties

Stamp duty was first introduced in England on 28 June 1694, during the reign of William III and Mary II, under "An act for granting to their Majesties several duties upon vellum, parchment and paper, for four years, towards carrying on the war against France".[3] In the 1702/03 financial year 3,932,933 stamps were embossed in England for a total value of £91,206.10s.4d.[4] Stamp duty was so successful that it continues to this day through a series of Stamp Acts. Similar duties have been levied in the Netherlands, France and elsewhere.

During the 18th and early 19th centuries, stamp duties were extended to cover newspapers, pamphlets, lottery tickets, apprentices' indentures, advertisements, playing cards, dice, hats, gloves, patent medicines, perfumes, insurance policies, gold and silver plate, hair powder and armorial bearings.[5]

The attempted enforcement of the Stamp Act 1765 in the British colonies in America led to the outcry of "no taxation without representation". The argument over stamp duty contributed to the outbreak of the American War of Independence.

Until 1793 stamp duty was always imposed as a fixed amount, regardless of the size of the transaction. In 1808 stamp duty on conveyances of sale, including transfers of land and shares, became an ad valorem tax.[6]

Historically, stamp taxes were administered by the Board of Stamps. This merged with the Board of Taxes in 1833/34, and the Board of Inland Revenue was created under the Inland Revenue Board Act 1849 by merger of the Board of Excise and Board of Stamps and Taxes. Stamp taxes were then administered by the Inland Revenue Stamp Taxes business stream (formerly the Stamp Office). Another merger occurred in 2004, when the Inland Revenue and HM Customs & Excise formed HM Revenue & Customs which now itself manages stamp duty.

The Stamp Duties Management Act 1891 and the Stamp Act 1891 still contain much of the operative law on stamp duties, although there have since been significant amendments and a partial consolidation was made in the Finance Act 1999. The Stamp Act 1891 was the inspiration for many of the older Australian stamp duty Acts.

Between 1782 and 1971, a tax was charged on cheques in the United Kingdom. The charge was one penny until 1918, when Chancellor of the Exchequer Bonar Law raised it to twopence. The tax was abolished shortly before decimalisation.[7]

List of items subject to Stamp Duty

The Stamps Act of 1694 imposed Stamp Duty on a range of legal instruments.[8] During the early part of the 18th century, the duty was extended to cover a number of other paper items (plus dice, which were stamped on their packaging) including the following:

- Playing cards (1711-1960) (became excise duty from 1864)

- Dice (1711-1862)

- Almanacks (1711-1834)

- Advertisements (1712-1853)

- Newspapers (1712-1855)

Later, because of the perceived efficiency of Stamp Duty as a means of raising revenue, Stamp Duty was levied on a whole variety of items, whether or not paper-based, including:

- Patent medicines (1783-1941)

- Gold and silver plate (1783-1890) (Stamp duty was also payable on licences to deal in plate)

- Hats (1784-1811)

- Game certificates (1784-2007) (became assessed tax from 1808 and excise licence from 1860)

- Gloves and mittens (1785-1794)

- Attorneys' and solicitors' licences (1785-1949)

- Pawnbrokers' licences (1785-1974) (excise licence from 1864)

- Hair powder (1786-1800)

- Perfumes and cosmetics (1786-1800)

- Receipts (1795)

- Paper (1795)

Current scope

The scope of stamp duty has been reduced dramatically in recent years. Apart from transfers of shares and securities, the issue of bearer instruments and certain transactions involving partnerships, stamp duty was largely abolished in the UK from 1 December 2003. "Stamp duty land tax" (SDLT), a new transfer tax derived from stamp duty, was introduced for land transactions from 1 December 2003. "Stamp duty reserve tax" (SDRT) was introduced on agreements to transfer uncertificated shares and other securities in 1986, and with the growth of paperless transactions SDRT rather than stamp duty now applies to most transfers of shares and securities. Stamp duty land tax on transactions was replaced in Scotland by the new Land and Buildings Transaction Tax (LBTT) from 1 April 2015 and replaced in Wales by Land Transaction Tax on 1 April 2018.[9]

Stamp Duty Reserve Tax

Aside from an exemption for 'qualifying intermediaries' such as market makers at large banks,[10] Stamp Duty Reserve Tax (SDRT) was introduced under the Finance Act 1986 to ensure that a form of tax equivalent to stamp duty would continue to be payable on the transfer of uncertificated shares. At that time, it was expected that the TAURUS share trading system would come into operation. In the event, SDRT was adapted for the change to trading in uncertificated shares in CREST, and is charged on agreements to transfer shares and other securities. SDRT is not a stamp tax, but a self-assessed transfer tax which is usually collected automatically by stock market participants (such as brokers) when a transaction takes place.

Stamp duty remains in force for shares and securities that are held in certificated form which can only be transferred by using a physical stock transfer form, and runs in parallel to SDRT on agreements to transfer shares. Since 1986, both stamp duty and SDRT have been charged at a rate of 0.5% of the consideration for the transfer of shares (in the case of stamp duty, rounded up to the nearest £5). The same transaction may include an agreement to transfer shares which may trigger a liability to SDRT, and the agreement may later be completed by a transfer of the shares which is liable to stamp duty. Provided that the transfer is stamped within 6 years, the charge to SDRT is cancelled to avoid a double charge. Stamp duty on repurchases of shares with a value of less than £1000 was abolished from 13 March 2008.[11]

A higher rate of SDRT at 1.5% is charged for the issue or transfer of shares to a person who operates a depositary receipt scheme or a clearance service (other than CREST, which is exempted). The higher charge compensates for the fact that later transfers of depositary interests or through the clearance services will not attract SDRT. This type of SDRT is by nature paid almost exclusively by offshore (i.e. non-UK) investors, primarily US fund managers and amounts to approx. 25% of the total SDRT collected annually.

A unique feature of SDRT, compared to other purely domestic taxes in the United Kingdom, is that more than 40% of the annual intake is collected from outside the UK, thus creating an annual inflow of approx. £1.5 billion from foreign investors to the UK government.

Stamp Duty Land Tax

Stamp Duty Land Tax (SDLT) is a tax on land transactions in England and Northern Ireland. It was introduced by the Finance Act 2003. It largely replaced stamp duty with effect from 1 December 2003. SDLT is not a stamp duty, but a form of self-assessed transfer tax charged on "land transactions".

In Scotland, a Land and Buildings Transaction Tax was introduced from April 1, 2015, replacing SDLT.[12]

In Wales, Land Transaction Tax replaced Stamp Duty in 2018.[13][14]

For typical transactions in land, such as the buying and selling of a residential house, there is little change from stamp duty, except that a tax return is required to be made to the HM Revenue & Customs (previously Inland Revenue) and documents no longer need to be given a physical stamp. Like any other self-assessed tax, but unlike stamp duty, HM Revenue & Customs is able to enquire into an SDLT return and raise assessments to recover unpaid SDLT.

Whether or not tax is payable, HM Revenue and Customs require a return to be received by them within four weeks of the transaction completing, failing which they have power to levy a fine on the tax payer – the fine is not for failure to pay the tax but for failure to make the return. When a return is accepted by HMRC they provide a certificate without which it is impossible to register a change in the land ownership. Even though the HMRC website itself says that Stamp Duty Land Tax is due within 14 days of the transaction completing,[15] Mortgage lenders may require that the Stamp Duty is paid upon completion itself. For example, see Barclays/Woolwich section 10.5 here:.[16]

Recent history of SDLT

In years prior to 2005, there had been a high level of house price inflation in the UK but no change in these thresholds, leading to a substantial increase in the revenue from SDLT through bracket creep. In 2000–01, the Inland Revenue received £2.145bn from residential stamp duty. In 2002–03, it received £3.59bn,[17] rising to £6.5bn in 2007-8 [18] In 2005, the threshold for paying SDLT was raised from £60,000 to £120,000. In 2006, the threshold was further raised to £125,000. In certain disadvantaged areas, the threshold is raised to £150,000. In 2007, at the Conservative Party Conference in Blackpool, George Osborne, the Shadow Chancellor, announced that a Conservative Government would abolish Stamp Duty for first-time buyers on properties up to £250,000. This pledge was abandoned when the Coalition Government was formed in 2010.

On 2 September 2008, the UK Government announced that the threshold for paying SDLT would be raised from £125k to £175k for one year, as from 3 September 2008.[19] In the 2009 Budget, the Chancellor extended this "stamp duty holiday" until the end of 2009.[20] In the 2010 budget, the Chancellor ended stamp duty on homes under £250,000 for first-time buyers for a two-year period only, while introducing a new 5% rate for properties over £1,000,000. In the budget of 2012, Chancellor George Osborne introduced a new 7% level for properties over £2,000,000 to assuage Liberal Democrat demands for a mansion tax. Some research has indicated this tax, at the lower end of the housing market, might depress mobility and lead to inefficient allocation of housing.[21]

In the 2014 Autumn Statement, Chancellor George Osborne announced reform to Stamp Duty to remove the slab element - stamp duty is now paid on the amount above certain thresholds rather than one rate on the total amount which depends on the amount, as detailed in the section above.[22]

In the 2015 Autumn Statement, Chancellor George Osborne announced further reforms to Stamp Duty. With effect from April 2016, buyers of second homes (whether Buy to let or holiday homes) will pay a 3% surcharge over the standard rate for any particular price.

Current position

For residential house purchases, the current rates in England & Northern Ireland from 8 July 2020 to 31 March 2021 are as follows:[23]

| Consideration | Rate (paid on portion in band) | Additional Property Rate |

|---|---|---|

| from £40,000 to £500,000 | 0% | 3% |

| from £500,001 to £925,000 | 5% | 8% |

| from £925,001 to £1,500,000 | 10% | 13% |

| over £1,500,000 | 12% | 15% |

The 2020 Summer Statement introduced a temporary reduction in Stamp Duty for buyers in England and Northern Ireland completing purchases before 31st March 2021 with no Stamp Duty due on the first £500,000 of property value.[24]

The government defines first-time buyers as '. . . an individual or individuals who have never owned an interest in a residential property in the United Kingdom or anywhere else in the world and who intends to occupy the property as their main residence.'

Position prior to December 2014

Prior to 4 December 2014 the rates were as follows:[25]

| Consideration | Rate (paid on total value) |

|---|---|

| up to £125,000 | 0% |

| from £125,001 to £250,000 | 1% |

| from £250,001 to £500,000 | 3% |

| from £500,001 to £1,000,000 | 4% |

| from £1,000,001 to £2,000,000 | 5% |

| over £2,000,000 | 7% (bought by individuals) 15% (bought by corporations) |

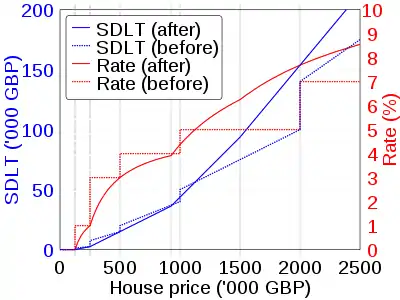

At this time, SDLT worked on a "slab" basis, so the above percentages apply to the whole of the purchase price. For example, a house priced at £250,000 would attract an SDLT of £2,500, but one of £250,001 would be liable to SDLT of £7,500, while one of £500,000 would be liable for £15,000 but a purchase of £500,001 would be liable for £20,000. The result is that SDLT had a distorting effect on the housing market, because a house is very difficult to sell at prices just above each threshold, for example, £250,001. There were regular calls for a different structure for stamp duty to avoid the distorting effect that the slab tax structure has on the housing market.

The effect at each trigger point is shown in the table below.

| House price £ | SDLT £ until 2014 | SDLT £ from 2014 |

|---|---|---|

| 125,000 | 0 | 0 |

| 125,001 | 1,250 | 0 |

| 250,000 | 2,500 | 2,500 |

| 250,001 | 7,500 | 2,500 |

| 500,000 | 15,000 | 15,000 |

| 500,001 | 20,000 | 15,000 |

| 1,000,000 | 40,000 | 43,750 |

| 1,000,001 | 50,000 | 43,750 |

| 2,000,000 | 100,000 | 153,750 |

| 2,000,001 | 140,000 (bought by individuals) 300,000 (bought by corporations) | 153,750 |

Leases

In addition to SDLT on the purchase price for land, SDLT is also charged when a lease is granted. Any premium for the grant is charged to SDLT at the same rates as for the purchase price for a sale of land; SDLT is also charged on the rent payable under the lease, at the rate of 1% of the (discounted) net present value of rent passing under the whole term of the lease. Previously, stamp duty was charged at rate of up to 24% of the annual rent. The amount of SDLT due on the grant of a typical commercial lease generally amounts to a substantial increase from the amount of stamp duty that would have been due previously.

Criticism of SDLT

Prior to the 2014 change, it was said that SDLT distorted[26] or depressed the housing market due to the sharp increases above certain thresholds (sometimes known as the "slab" system).[27] Campaigners like the Taxpayers Alliance and Stamp Duty Reform UK, argued for a progressive tax based on incremental tax bands.[28][29] In November 2013 the Council of Mortgage Lenders produced a detailed report calling for reform.[30]

The changes made in the 2014 Autumn Statement have caused a collapse in the number of sales of more expensive properties.[31][32]

In October 2015 the Spatial Economics Research Centre produced a report detailing the distorting effects of Stamp Duty on the housing market.[33]

See also

References

- "HMRC Stamp Taxes Manual" (PDF). hmrc.gov.uk. p. 7. Archived from the original (PDF) on 6 February 2014. Retrieved 6 March 2019.

- Dr. Stephen Spratt of Intelligence Capital (September 2006). "A Sterling Solution" (PDF). Stamp Out Poverty report. Stamp Out Poverty Campaign. pp. 15–16. Retrieved 6 March 2019.

- Dagnall, H. (1994) Creating a Good Impression: three hundred years of The Stamp Office and stamp duties. London: HMSO, p. 3. ISBN 0116414189

- Dagnall, p. 10.

- "Records of stamp duties and related responsibilities". National Archives. Retrieved 4 April 2018.

- "Stamp Taxes Manual" (PDF). HM Revenue and Customs. Archived from the original (PDF) on 6 February 2014. Retrieved 6 November 2011. paras 1.34 to 1.40

- Taxes and stamp duty. Cheque and Credit Clearing Company, 2012. Retrieved 26 June 2013. Archived here.

- Full text of the 1694 Act

- https://www.gov.uk/stamp-duty-land-tax

- "HMRC Stamp Taxes Manual" (PDF). hmrc.gov.uk. pp. 9, 15. Archived from the original (PDF) on 6 February 2014. Retrieved 6 January 2016.

- Archived 24 July 2008 at the Wayback Machine

- Archived 14 September 2015 at the Wayback Machine

- https://gov.wales/funding/fiscal-reform/welsh-taxes/land-transaction-tax/?lang=en

- https://debitoor.com/dictionary/land-transaction-tax

- "Pay Stamp Duty Land Tax - Detailed guidance - GOV.UK". Hmrc.gov.uk. Retrieved 6 January 2016.

- cml.org.uk Archived 30 July 2013 at the Wayback Machine

- "HM Revenue & Customs: Home Page" (PDF). Inlandrevenue.gov.uk. 28 June 2011. Retrieved 24 August 2013.

- "UK | UK Politics | Government 'may defer' stamp duty". BBC News. 5 August 2008. Retrieved 24 August 2013.

- "Stamp duty axed below £175,000". BBC News. 2 September 2008. Retrieved 24 May 2010.

- Gammell, Kara (22 April 2009). "Housing market in the Budget 2009: stamp duty". The Daily Telegraph. London. Retrieved 24 May 2010.

- "SERC: Spatial Economics Research Centre: Does stamp duty stop people moving house?". Spatial-economics.blogspot.co.uk. 24 July 2012. Retrieved 24 August 2013.

- Hilary Osborne. "Stamp duty reform: the key facts | Money". The Guardian. Retrieved 6 January 2016.

- "Stamp duty reforms – factsheet". GOV.UK. HM Treasury. 3 December 2014. Retrieved 3 December 2014.

- https://www.gov.uk/guidance/stamp-duty-land-tax-temporary-reduced-rates

- "Stamp Duty Land Tax rates". GOV.UK. 19 August 2013. Retrieved 24 August 2013.

- "House of Commons - HC 1652 Communities and Local Government Committee: Written submission from the National Association of Estate Agents and the Association of Residential Letting Agents". Publications.parliament.uk. 1 May 2012. Retrieved 23 September 2012.

- Dr. Christian Hilber (24 July 2012). "SERC: Spatial Economics Research Centre: Does stamp duty stop people moving house?". Spatial-economics.blogspot.co.uk. Retrieved 23 September 2012.

- Stamp Out Stamp Duty, The TaxPayers' Alliance, 2013. Retrieved 15 September 2013. Archived here.

- Archived 3 January 2014 at the Wayback Machine

- Stamp duty: growth in revenue reinforces case for reform CML News and Views, No. 21, Council of Mortgage Lenders, 5 November 2013. Retrieved 6 November 2013. Archived here.

- "Stamp duty: has London finally lost its status as the luxury property hotspot of the world?". Telegraph. 30 November 2015. Retrieved 6 January 2016.

- Jonathan Prynn; Joanna Bourke (24 July 2015). "Stamp duty rise hits London home prices with fastest fall since the crash". Standard.co.uk. Retrieved 6 January 2016.

- "Transfer Taxes and Household Mobility: Distortion on the Housing or Labor Market?" (PDF). Spatialeconomics.ac.uk. Retrieved 6 January 2016.