Straddle

In finance, a straddle strategy refers to two transactions that share the same security, with positions that offset one another. One holds long risk, the other short. As a result, it involves the purchase or sale of particular option derivatives that allow the holder to profit based on how much the price of the underlying security moves, regardless of the direction of price movement.

A straddle involves buying a call and put with same strike price and expiration date. If the stock price is close to the strike price at expiration of the options, the straddle leads to a loss. However, if there is a sufficiently large move in either direction, a significant profit will result. A straddle is appropriate when an investor is expecting a large move in a stock price but does not know in which direction the move will be.[1]

The purchase of particular option derivatives is known as a long straddle, while the sale of the option derivatives is known as a short straddle.

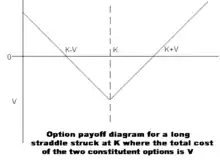

Long straddle

A long straddle involves "going long," in other words, purchasing both a call option and a put option on some stock, interest rate, index or other underlying. The two options are bought at the same strike price and expire at the same time. The owner of a long straddle makes a profit if the underlying price moves a long way from the strike price, either above or below. Thus, an investor may take a long straddle position if he thinks the market is highly volatile, but does not know in which direction it is going to move. This position is a limited risk, since the most a purchaser may lose is the cost of both options. At the same time, there is unlimited profit potential.[2]

For example, company XYZ is set to release its quarterly financial results in two weeks. A trader believes that the release of these results will cause a large movement in the price of XYZ's stock, but does not know whether the price will go up or down. He can enter into a long straddle, where he gets a profit no matter which way the price of XYZ stock moves, if the price changes enough either way. If the price goes up enough, he uses the call option and ignores the put option. If the price goes down, he uses the put option and ignores the call option. If the price does not change enough, he loses money, up to the total amount paid for the two options. The risk is limited by the total premium paid for the options, as opposed to the short straddle where the risk is virtually unlimited.

If the stock is sufficiently volatile and option duration is long, the trader could profit from both options. This would require the stock to move both below the put option's strike price and above the call option's strike price at different times before the option expiration date.

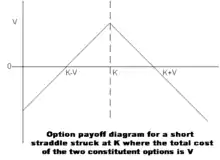

Short straddle

A short straddle is a non-directional options trading strategy that involves simultaneously selling a put and a call of the same underlying security, strike price and expiration date. The profit is limited to the premium received from the sale of put and call. The risk is virtually unlimited as large moves of the underlying security's price either up or down will cause losses proportional to the magnitude of the price move. A maximum profit upon expiration is achieved if the underlying security trades exactly at the strike price of the straddle. In that case both puts and calls comprising the straddle expire worthless allowing straddle owner to keep full credit received as their profit. This strategy is called "nondirectional" because the short straddle profits when the underlying security changes little in price before the expiration of the straddle. The short straddle can also be classified as a credit spread because the sale of the short straddle results in a credit of the premiums of the put and call.

A risk for holder of a short straddle position is unlimited due to the sale of the call and the put options which expose the investor to unlimited losses (on the call) or losses limited to the strike price (on the put), whereas maximum profit is limited to the premium gained by the initial sale of the options. Losses from a short straddle trade placed by Nick Leeson were a key part of the collapse of Barings Bank.[3]

Tax straddle

A tax straddle is straddling applied specifically to taxes, typically used in futures and options to create a tax shelter.[4]

For example, an investor with a capital gain manipulates investments to create an artificial loss from an unrelated transaction to offset their gain in a current year, and postpone the gain till the following tax year. One position accumulates an unrealized gain, the other a loss. Then the position with the loss is closed prior to the completion of the tax year, countering the gain. When the new year for tax begins, a replacement position is created to offset the risk from the retained position. Through repeated straddling, gains can be postponed indefinitely over many years.[5]

Further reading

| Library resources about Fiscal policy |

- Publication 17 Your Federal Income Tax

- Form 1040 series of forms and instructions

- Social Security's booklet "Medicare Premiums: Rules for Higher-Income Beneficiaries" and the calculation of the Social Security MAGI.

- McMillan, Lawrence G. (2002). Options as a Strategic Investment (4th ed.). New York : New York Institute of Finance. ISBN 978-0-7352-0197-2.

- McMillan, Lawrence G. (2012). Options as a Strategic Investment (5th ed.). Prentice Hall Press. ISBN 978-0-7352-0465-2.

- Specific

- S, Suresh A. (2015-12-28). "ANALYSIS OF OPTION COMBINATION STRATEGIES". Management Insight. 11 (1). ISSN 0973-936X.

- Barrie, Scott (2001). The Complete Idiot's Guide to Options and Futures. Alpha Books. pp. 120–121. ISBN 0-02-864138-8.

- Monthe, Paul. "Stories - How Nick Leeson caused the collapse of Barings Bank". Next Finance.

- "Passthrough Entity Straddle Tax Shelter". IRS.gov. Retrieved Jan 9, 2015.

- Brabec, Barbara (Nov 26, 2014). How to Maximize Schedule C Deductions & Cut Self-Employment Taxes to the BONE -. Barbara Brabec Productions. p. 107. ISBN 978-0985633318.