Universities Superannuation Scheme

The Universities Superannuation Scheme is a pension scheme in the United Kingdom with over £67 billion under management as of March 2019.[1] It has over 400,000 members, made up of active and retired academic and academic-related staff (including senior administrative staff) mostly from those universities established prior to 1992 (staff in the post-1992 universities are mostly members of the Teachers Pension Scheme). In 2006, it was the second largest private pension scheme in the UK by fund size.[2] The headquarters of Universities Superannuation Scheme Limited (USS) are in Liverpool.[3]

History

The Federated Superannuation Scheme for Universities, 1913–1974

In 1911 the President of the Board of Education established an Advisory Committee on University Grants. This research formed the basis of the predecessor of USS, the Federated Superannuation System for Universities, which was approved by the Board of Education and membership became compulsory for new appointees post 1 October 1913. The basic plan criteria were:

- The benefit was an annuity or cash payment through an insurance policy maturing at age 60.

- Optionally, benefits were available for dependants on death in service.

- The policy was held in trust by the member’s institution and was transferable to a new institution if required or to an individual on leaving the University service.

- Members contributed 5% of salary and the employer matched this until 1920 when the employer contribution was increased to 10%.

- Administrative staff on salaries comparable to academic staff were also eligible to join.

However, perceived drawbacks of the scheme were that it did not link to final pay, access was contingent on a medical examination, there was no guarantee for dependents, little provision for risk benefits, and no indexation of benefits. Hence it compared unfavourably to the defined benefit scheme already enjoyed by school teachers under the School Teachers (Superannuation) Act 1918. From 1958 to 1969 several committees were established to review the present arrangements. The recommendations for a defined benefit scheme were initially rejected by universities in 1960 and again by a committee in 1964, who concluded it was “unable to make a clear recommendation in favour of either system”.[4]

Universities Superannuation Scheme, 1974–2011

In 1969, a Joint Consultative Committee (JCC) for the reform of FSSU was established, and commissioned a report from G. Heywood (the FSSU Consulting Actuary) that included a proposed outline for USS. It was to be a one-eightieth scheme with a three times annuity lump sum, available to new entrants only. No medical examination was required and pensions would not be increased.

A meeting to discuss the structure of USS took place in Liverpool on the 28 December 1970. The proposal for an independent company was approved by the JCC in November 1971, and endorsed by the CVCP in December 1971. The FSSU Executive Committee was “unenthusiastic”. Drafting of the rules began in 1971, with the seventh draft being agreed in August 1973 and circulated to universities along with an explanatory booklet. The scheme was finally introduced on 1 April 1975.[4] The scheme was a 'balance of cost' scheme in which the sponsors bear the risk of default, and specifically a 'last-man-standing multi-employer scheme', meaning that if an employer collapsed, the others would bear its responsibilities to its pensioners, such that 'default would require the bankruptcy of every institution, that is, the collapse of the UK university and research community'. Combined with extensive state funding of the higher education sector, this has been thought to make the risk of default very low.[5]:9

At the scheme's inception, contributions were 16% of salary, with employers paying 10%, and members paying 6% plus a 2% surcharge aimed at covering benefits for service prior to the scheme's inception.[4] From 1983 to 1997, the employers' contribution rate increased to 18.55%. From January 1997 to September 2009 it decreased to 14%, and employee contribution reduced to 6.35%.[6][7] The employer contribution was increased to 16% in October 2009.[6]

The defined benefit of the scheme was to consist of a one-time cash lump sum of 3/80 of the final salary and an annual income of 1/80 of retiree's final salary, both multiplied by years of contributions. For purposes of calculation, the final salary was revalued each year in line with inflation.[8]

From its inception, USS was the main pension scheme for UK academics and senior administrative staff of universities and similar higher-education or research institutions.[4] This predominance was lessened, however, when the Further and Higher Education Act 1992 created numerous 'new universities', whose employees (old and new) remained in the state-run Teachers' Pension Scheme.[9] From 10 December 1999, any employee of a UK higher education institution became eligible to join USS if they wished.[7]

By 2014, USS had become the UK's second-largest pension scheme, with 316,440 active members, deferred pensioners and pensioners. It was, by this measure, the world's 36th-largest. 374-79 separate institutions participated in the scheme, and its assets were valued at £42 billion.[5]:9[10]:15 In 2017 it had 190,546 active members.[11]

Changes of 2011

Few changes to USS's rules were made until October 2011, when dramatic changes were implemented,[12]:3[10]:25 partly in response to losses resulting from the Great Recession, and consequent increased projected scheme deficit:[9]

- USS closed its final salary scheme to new members, replacing it with a career average revalued earnings (CARE) scheme for new members.

- The retirement age was linked to the UK state retirement age.

- Contribution rates for members still in the final salary section rose from 6.35% to 7.5%.

- The scheme changed from being 'balance-of-cost' (in which sponsors are ultimately responsible for meeting promised pensions) to a 'cap-and-share' rule, in which extra contributions would, if necessary, be met 35% by members and 65% by sponsors.

- The indexation of deferred pensions and pensions in payment was changed from the retail price index to the less generous consumer price index, and uprating of accrued benefits was capped.[13]

The changes were the subject of 'heated public controversy' between USS's institutional sponsors and the scheme's members, represented by the University and College Union, and involved lengthy industrial action.[10]:15 Researchers did find, however, that 'the pre-October 2011 scheme was not viable in the long run', whereas the post-October 2011 scheme was 'probably viable in the long run', though it faced medium-term problems as the effects of the changes on the state of the fund would take time to be felt.[10]:14

Subsequent research found that reductions in payout reduced the effective value of making (pre-tax contributions) to USS pension versus having to make after-tax contributions to a private savings by £2.86 billion (£1.86 billion attributable to loss of value fore the member contribution and the rest in loss of return to members from the employer contribution) Whereas young members joining the pre-2011 scheme could expect their net wealth to increase by £181,000 (£133,000 gross) relative to opting out of the scheme, those joining the post-2011 CARE section could expect a much smaller increase: £98,000 (£46,000 gross).[12]:21 An earlier study by the same researchers concluded that the reduced wealth of post-2011 entrants was equivalent to an 11% drop in their total compensation or a 13% drop in their salaries.[10]:25 The researchers nonetheless found that the scheme remained attractive.[12]:21

Changes of 2016

Despite the changes of 2011, with ongoing weak economic performance associated with the Great Recession, USS continued to identify deficits, leading to further negotiations, industrial action, and eventually dramatic changes being implemented in April 2016.[9] The key changes were:[14]

- The final-salary pension scheme (only available to members who joined before the 2011 changes) was closed. Benefits previously accrued were protected, but were frozen at a level relating to an employee’s salary as of March 2016 (uprated annually by inflation).

- All active members thereafter switched to the CARE scheme, with benefits being based on career-average earnings.

- Employee contributions rose to 8%, and employer contributions from 16% to 18% of salary.

- Defined benefits could now only be earned on the first £55,000 of a salary. For salary over £55,000, employers paid only 12% (rather than 18%) of salary into this defined contribution scheme (6% being diverted from higher earner's pension toward paying down the scheme deficit). Staff had the option of making an additional 1% payment which would be matched by the employer.

- Defined benefit accrual was raised from one eightieth to one seventy-fifth of pensionable salary.

2018 Proposed changes

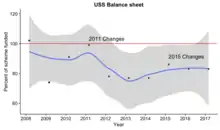

By 2017, the scheme had over 400,000 members.[15] The USS scheme reported a technical deficit of £17.5 billion in July 2017, reported as the largest such shortfall in the UK at that time.[15] Under diverse conventional accounting rules, the scheme has been in deficit for several years (see Figure). This varies depending on the rules used. For instance as of March 2010,[16] the actuary estimated the scheme was 91% funded (£3.1 billion deficit) according to the scheme specific funding regime, 80% funded on an FRS17 basis, and 57% funded on a buy-out basis.[16]

The USS Joint Negotiating Committee therefore made the following proposals, to be introduced after 1 April 2019:[17]

- The defined benefits section of the scheme would close (with a possibility of reintroducing it). All future benefits (apart from death in service and ill health retirement benefits) would be transferred to the defined contribution (DC) scheme.

- Member contributions would remain at 8%. Members would gain an option of paying in only 4% while still receiving the full employer contribution. The employer match of the first 1% of any voluntary employee savings would be lost. Members’ contributions would include a contribution to finance death in service and ill-health retirement benefits.

- Employer contributions would remain at 18%. Of this 13.25% would build employee DC pension pots, with the other 4.75% used for deficit recovery (plus management and running costs).

UCU, whose objections to these proposals had been overruled, proceeded to ballot successfully for industrial action in an attempt to secure a more favourable settlement for members, leading to the 2018 USS pension dispute.[18][19][20]

2019 Scheme cost increases

Following the 2018 strike action, contributions from employees and employers increased substantially:[21] Member contributions increased, initially from 8% to 8.8% of salary. Then from 1 October 2019, to 9.6%. Subject to review, this is planned to increase to 11% from 1 October 2021. Corresponding employer contributions increased from 18% to 19.5%, then (from 1 October) to 21.1%, with a planned increase to 23.7% planned for 2021. For members earning over the salary cap (~£58,000), employer contribution dropped to 12% for earnings above this threshold, with the difference (about 9% of salary) being used to pay down the overall scheme deficit.

2019 exit by Trinity College, Cambridge

On 15 March 2019, in a move that came to be dubbed 'Trexit' (an allusion to Brexit), the Council of Trinity College, Cambridge voted to withdraw the college unilaterally from USS as of 31 May 2019, replacing the USS scheme with a defined benefits scheme, to avoid the college bearing any responsibility for other pensions in the UK higher education system in the event of foreclosures in the sector. USS noted that this development would not in itself significantly affect the strength of the scheme, but that if a further financially secure employer left the scheme, the scheme would be markedly weaker. The move prompted some Cambridge academics to begin boycotting supervising Trinity College students,[22][23][24][25] with over 450 Cambridge academics pledging to withdraw all labour from the college by 19 June.[26] Cambridge University's graduate student union supported the boycott, discouraging postgraduate students from taking up teaching for Trinity.[27] The General Secretary elect of UCU, Jo Grady, published an open letter calling on the college's fellows to change their course, arguing that to do so was in their interest and the interest of the USS pension scheme generally.[28][29]

On 21 June, however, Trinity's fellows voted by 73 votes to 46 to leave USS, prompting UCU to consider its second ever national boycott of a UK HE institution.[30][31]

In October 2019, as the 2019-20 academic year began, several fellows of Trinity resigned.[32] With the number of staff boycotting Trinity reported as standing at 550, Trinity students began to report difficulty finding supervisors, and protests were staged at the inauguration of Trinity's new master, Sally Davies. The University and College Union was reported at this time as preparing a national boycott of Trinity College.[27] In February 2020, Arundhati Roy had agreed to give Trinity College's annual Clark Lecture in English literature, but withdrew at the request of Cambridge UCU because of the boycott.[33][34] She did, however, supply her lecture to Trinity in written form, and it appeared on the college's website.[34][35][36]

Management and Investments

The scheme publishes detailed annual reports, available online.[37] Returns on the portfolio over 5 years to 31 March 2019 were an annualised 10.09% per yr.[1]

Through the 1990s and into 2020, the fund's main asset classes were UK, European and US equities; US and UK bonds; UK property; and cash. USS's liabilities are all in sterling and, from April 2006, USS began hedging all foreign exchange risk (having previously hedged none).[5]

In 2019, the largest asset classes were Listed Shares (40.92%), Other private markets (21%), Index-linked bonds (19.84%) with smaller holdings in fixed income (8.55%), property (5.51%), government bonds (4.85%) and cash (4.49%).[1] The fund is underweight US equities. A decade earlier (2011), the distributions were: 60% equities (UK 23.06%, EU 18.32%, US 18.32%), cash (5%), 10-year UK government bonds (12.3%), UK property (7%), hedge funds (8%), and commodities (8%).[10]:19

Commercial assets have included Telford Shopping Centre in Telford, Shropshire (sold to Hark Group and Apollo Real Estate), and the Grand Arcade development in Cambridge and Forestside Shopping Centre, Belfast. The latter was bought from Sainsbury's for £50 million in 1998 and sold in 2001 for £70 million. They currently own Moto Hospitality. In 2013, Australian train operator Airtrain Citylink was purchased.[38]

The scheme has investment costs of .34% in 2019[1] (compared to 0.32% (32 basis points) total annual administration costs of £124.9m in 2017),[11] and pension administration costs of £69 per member.

Criticisms

In 1997, following a sustained People & Planet campaign named 'Ethics for USS', USS established a policy on responsible investment, including appointing an advisor on the issue.[39] The scheme came under renewed pressure from 2015, via the 'USS: Step Up' campaign, which had noted investments in tobacco and fossil fuels.[39] As of 2019, USS offers four ethical investment options. Around 8% of members had taken advantage of these.[1]

In 2017, it was reported that the USS pension scheme has offshore investments in tax havens.[40] In 2014, USS's highest-paid executive, received a 50% pay increase, to £900,000[41] and criticism of the high pay of top USS employees grew. In 2018, it was noted that pay for USS's chief executive rose from £484,000 in 2017 to £566,000 in 2018, while two staff members earned over £1m, and running costs stood at £125m per annum.[42][43]

See also

- UK pensions

- UK labour law

Notes

- USS (Jan 2020). "USS Report and Accounts (2019)" (PDF). USS. Retrieved 18 Feb 2020.

- Universities Superannuation Scheme Limited. "History of the scheme". Archived from the original on 2006-10-06. Retrieved 2007-02-09.

- "Contact USS". Universities Superannuation Scheme Ltd. Retrieved 2012-04-09.

- Douglas Logan, The Birth of a Pension Scheme. A History of the Universities Superannuation Scheme (Liverpool University Press 1985).

- Emmanouil Platanakis and Charles Sutcliffe, 'Asset–Liability Modelling and Pension Schemes: The Application of Robust Optimization to USS', The European Journal of Finance (2015), 1-29, doi:10.1080/1351847X.2015.1071714.

- Susan Cooper, 'A Pensions Proposal: Constant Contributions' (p. 1).

- John Board and Charles Sutcliffe, 'Joined‐Up Pensions Policy in the UK: An Asset‐Liability Model for Simultaneously Determining the Asset Allocation and Contribution Rate', JEL, 40 (Autumn 2007), 87-118 (p. 102) (first published in Handbook of Asset and Liability Management, edited by Stavros A. Zenios and William T. Ziemba, (North Holland Handbooks in Finance, Elsevier Science B.V., Volume 2, 2007, pp. 1029‐67 ISBN 0444528024).

- "Benefits earned before April 2016 | The USS scheme | For members | USS". www.uss.co.uk. Retrieved 2018-09-08.

- 'What will the end of final-salary pensions mean for academics?', Times Higher Education (12 March 2015), URL.

- Emmanouil Platanakis and Charles Sutcliffe, 'Pension Scheme Redesign and Wealth Redistribution Between the Members and Sponsor: The USS Rule Change in October 2011', Insurance: Mathematics and Economics, 69 (2016), 14–28. doi:10.1016/j.insmatheco.2016.04.001

- USS. "2017 Report and Accounts.pdf" (PDF). Retrieved 28 February 2018.

- Emmanouil Platanakis and Charles Sutcliffe, 'Pension Schemes, Taxation and Stakeholder Wealth: The USS Rule Changes', ICMA Centre, Discussion Paper Number: ICM-2017-08 (23 January 2018): https://ssrn.com/abstract=3039364; doi:10.2139/ssrn.3039364

- 'USS to adopt CPI inflation measure', The Financial Times (23 January 2011).

- Jack Grove, 'New USS Pension Reform Plans to be Put to Union Vote', Times Higher Education (15 January 2015).

- 'Universities’ main pension pot faces the biggest deficit of any British fund', The Economist (3 August 2017).

- USS (31 March 2010). "USS Report & Accounts for the year ended 31 March 2010. (pages 54 & 96)" (PDF): 1–100 – via USS. Cite journal requires

|journal=(help) - 'Proposed changes to future USS benefits'.

- "UCU announces 14 strike dates at 61 universities in pensions row". www.ucu.org.uk. Retrieved 2018-02-06.

- "University strike: What's it all about?". BBC News Online. BBC. Retrieved 24 February 2018.

- Jane Deith, 'University staff strike over pensions', Channel 4 News (22 February 2018).

- "Schedule of Contributions | Funding USS | Running USS | USS". www.uss.co.uk. Retrieved 2019-11-27.

- Noella Chye, 'Revealed: Trinity plans exit from national pension scheme, isolating college from higher education sector', Varsity (8 December 2018).

- Noella Chye, 'Leaked: Trinity has voted to leave the UK pensions scheme. If two employers exit, staff pensions may be in uncharted territory', Varsity (19 May 2019).

- Rosie Bradbury, 'Trinity confirms exit from national pensions scheme – over 230 academic staff will now boycott supervising Trinity students', Varsity (24 May 2019).

- Chris Havergal, 'Cambridge’s Trinity confirms departure from USS pension scheme', Times Higher Education (24 May 2019).

- Chloe Bayliss, '‘Arrogant and uncollegial’: Academics on Trinity’s USS withdrawal', Varsity (19 June 2019).

- Ellie Arden and Dylan Perera, 'Trexit conflicts continue as Trinity welcomes new master', Varsity (8 October 2019).

- Rosie Bradbury, 'Cambridge academics rally outside Trinity in protest of USS exit', Varsity (30 May 2019).

- Jo Grady, 'Open letter to Fellows of Trinity College, Cambridge' (29 May 2019).

- Natalie Tuck, 'UCU threatens boycott of Trinity College over USS exit', PensionsAge (21 June 2019).

- "Union censures Cambridge's Trinity College in row over pension scheme" (21 June 2019).

- Camilla Turner, "Cambridge college faces resignations over decision to switch pension plans for staff", The Telegraph (3 October 2019), p. 11.

- Anna Vassiliades, 'Trinity College’s 2020 Clark Lecturer pulls out in solidarity with the academic boycott', The Cambridge Tab (4 February 2020).

- Kenneth Yarhamby Beatriz Valero de Urquia, 'Ongoing academic boycott of Trinity College sees Clark Lecture cancelled', Varsity (14 February 2020).

- Arundhati Roy, 'The Graveyard Talks Back: Fiction in the Time of Fake News' (accessed 21 February 2020).

- 'Arundhati Roy's Clark Lecture 2020' (accessed 21 February 2020).

- "Report and accounts | Running USS | USS". www.uss.co.uk. Retrieved 2018-03-04.

- UK pension scheme buys Brisbane railway Money Management 27 March 2013.

- George Hammond, 'Universities encouraged to Step Up for more ethical pensions', Ethical Consumer (8 April 2016).

- "More than 100 universities and colleges in Offshore Leaks data - ICIJ". ICIJ. 2017-11-17. Retrieved 2017-12-14.

- "Subscribe to read". Financial Times. Cite uses generic title (help)

- Sean Coughlan, '[www.bbc.co.uk/news/education-43157711 University pension boss's £82,000 pay rise]', BBC News (22 February 2018).

- E.g. Christine Berry, 'USS is the tip of the iceberg. Our pensions system is a hot mess', OpenDemocracy (1 March 2018).

References

- GR Macdonald, Fifty years of the F.S.S.U. (1965).

External links

- Hillman, Nick, 'The USS: How did it come to this?', HEPI Report 115 (Higher Education Policy Unit, 2019)

- USS Website

- USS Actuarial Valuation, updated 8 December 2017

- USS Technical provisions consultation document, 1 September 2017

- USS Presentation to Imperial College, 23 November 2017