Freddie Mac

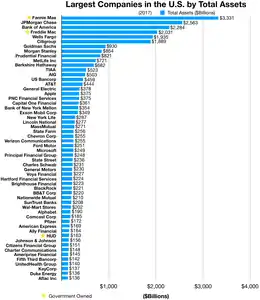

The Federal Home Loan Mortgage Corporation (FHLMC), known as Freddie Mac, is a public government-sponsored enterprise (GSE), headquartered in Tysons Corner, Virginia.[3][4] Freddie Mac is ranked No. 41 on the 2020 Fortune 500 list of the largest United States corporations by total revenue, and has $2.063 trillion assets under management.[5]

| |

| Type | Government-sponsored enterprise and public company |

|---|---|

| OTCQB: FMCC | |

| Industry | Financial services |

| Founded | 1970 |

| Headquarters | Tysons Corner, Virginia, U.S. (McLean mailing address) |

Key people | Sara Mathew (Non-Executive Chair) David Brickman (Executive VP & CEO) |

| Products | Diversified financials |

| Services | Credit services Diversified investments |

| Revenue | |

| Total assets | |

| Total equity | |

Number of employees | 6,892 (February 2019)[1] |

| Website | FreddieMac.com |

| Footnotes / references [2] | |

The FHLMC was created in 1970 to expand the secondary market for mortgages in the US. Along with the Federal National Mortgage Association (Fannie Mae), Freddie Mac buys mortgages on the secondary market, pools them, and sells them as a mortgage-backed security to investors on the open market. This secondary mortgage market increases the supply of money available for mortgage lending and increases the money available for new home purchases. The name "Freddie Mac" is a variant of the initialism of the company's full name that was adopted officially for ease of identification.

On September 7, 2008, Federal Housing Finance Agency (FHFA) director James B. Lockhart III announced he had put Fannie Mae and Freddie Mac under the conservatorship of the FHFA (see Federal takeover of Fannie Mae and Freddie Mac). The action has been described as "one of the most sweeping government interventions in private financial markets in decades".[6][7][8]

Moody's gave Freddie Mac's preferred stock an investment grade credit rating of A1 until August 22, 2008, when Warren Buffett said publicly that both Freddie Mac and Fannie Mae had tried to attract him and others. Moody's changed the rating on that day to Baa3, the lowest investment-grade rating. Freddie's senior debt credit rating remains Aaa/AAA from each of the major rating agencies: Moody's, S&P, and Fitch.[9]

As of the start of the conservatorship, the United States Department of the Treasury had contracted to acquire US$1 billion in Freddie Mac senior preferred stock, paying at a rate of 10% per year, and the total investment may subsequently rise to as much as US$100 billion.[10] Shares of Freddie Mac stock, however, plummeted to about one U.S. dollar on September 8, 2008, and dropped a further 50% on June 16, 2010, when the Federal Housing Finance Agency ordered the stocks delisted.[11] In 2008, the yield on U.S Treasury securities rose in anticipation of increased U.S. federal debt.[12] The housing market and economy eventually recovered, making Freddie Mac profitable once again.

History

From 1938 to 1968, the Federal National Mortgage Association (Fannie Mae) was the sole institution that bought mortgages from depository institutions, principally savings and loan associations, which encouraged more mortgage lending and effectively insured the value of mortgages by the US government. In 1968, Fannie Mae split into a private corporation and a publicly financed institution. The private corporation was still called Fannie Mae and its charter continued to support the purchase of mortgages from savings and loan associations and other depository institutions, but without an explicit insurance policy that guaranteed the value of the mortgages. The publicly financed institution was named the Government National Mortgage Association (Ginnie Mae) and it explicitly guaranteed the repayments of securities backed by mortgages made to government employees or veterans (the mortgages themselves were also guaranteed by other government organizations).

To provide competition for the newly private Fannie Mae and to further increase the availability of funds to finance mortgages and home ownership, Congress then established the Federal Home Loan Mortgage Corporation (Freddie Mac) as a private corporation through the Emergency Home Finance Act of 1970. The charter of Freddie Mac was essentially the same as Fannie Mae's newly private charter: to expand the secondary market for mortgages and mortgage-backed securities by buying mortgages made by savings and loan associations and other depository institutions. Initially, Freddie Mac was owned by the Federal Home Loan Bank System and governed by the Federal Home Loan Bank Board.

In 1989, the Financial Institutions Reform, Recovery and Enforcement Act of 1989 ("FIRREA") revised and standardized the regulation of Fannie Mae and Freddie Mac. It also severed Freddie Mac's ties to the Federal Home Loan Bank System. The Federal Home Loan Bank Board (FHLBB) was abolished and replaced by different and separate entities. An 18-member board of directors for Freddie Mac was formed, and subjected to oversight by the U.S. Department of Housing and Urban Development (HUD). Separately, The Federal Housing Finance Board (FHFB) was created as an independent agency to take the place of the FHLBB, to oversee the 12 Federal Home Loan Banks (also called district banks).

In 1995, Freddie Mac began receiving affordable housing credit for buying subprime securities, and by 2004, HUD suggested the company was lagging behind and should "do more".[13]

Freddie Mac was put under a conservatorship of the U.S. federal government on Sunday, September 7, 2008.[14]

Business

Freddie Mac's primary method of making money is by charging a guarantee fee on loans that it has purchased and securitized into mortgage-backed security (MBS) bonds. Investors, or purchasers of Freddie Mac MBS, are willing to let Freddie Mac keep this fee in exchange for assuming the credit risk. That is, Freddie Mac guarantees that the principal and interest on the underlying loan will be paid back regardless of whether the borrower actually repays. Owing to Freddie Mac's financial guarantee, these MBS are particularly attractive to investors and, like other Agency MBS, are eligible to be traded in the "to-be-announced", or "TBA" market.[15]

Conforming loans

The GSEs are allowed to buy only conforming loans, which limits secondary market demand for non-conforming loans. The relationship between supply and demand typically renders the non-conforming loan harder to sell (fewer competing buyers); thus it would cost the consumer more (typically 1/4 to 1/2 of a percentage point, and sometimes more, depending on credit market conditions). OFHEO, now merged into the new FHFA, annually sets the limit of the size of a conforming loan in response to the October to October change in mean home price. Above the conforming loan limit, a mortgage is considered a jumbo loan. The conforming loan limit is 50 percent higher in such high-cost areas as Alaska, Hawaii, Guam and the US Virgin Islands,[16] and is also higher for 2–4 unit properties on a graduating scale. Modifications to these limits were made temporarily to respond to the housing crisis, see Jumbo loan for recent events.

No actual guarantees

The FHLMC states, "securities, including any interest, are not guaranteed by, and are not debts or obligations of, the United States or any agency or instrumentality of the United States other than Freddie Mac."[17] The FHLMC and FHLMC securities are not funded or protected by the US Government. FHLMC securities carry no government guarantee of being repaid. This is explicitly stated in the law that authorizes GSEs, on the securities themselves, and in public communications issued by the FHLMC.

Assumed guarantees

There is a widespread belief that FHLMC securities are backed by some sort of implied federal guarantee and a majority of investors believe that the government would prevent a disastrous default. Vernon L. Smith, 2002 Nobel Laureate in economics, has called FHLMC and FNMA "implicitly taxpayer-backed agencies".[18] The Economist has referred to "the implicit government guarantee"[19] of FHLMC and FNMA.

The then director of the Congressional Budget Office, Dan L. Crippen, testified before Congress in 2001, that the "debt and mortgage-backed securities of GSEs are more valuable to investors than similar private securities because of the perception of a government guarantee."[20]

Federal subsidies

The FHLMC receives no direct federal government aid. However, the corporation and the securities it issues are thought to benefit from government subsidies. The Congressional Budget Office writes, "There have been no federal appropriations for cash payments or guarantee subsidies. But in the place of federal funds the government provides considerable unpriced benefits to the enterprises. Government-sponsored enterprises are costly to the government and taxpayers. The benefit is currently worth $6.5 billion annually." [21]

The mortgage crisis from late 2007

As mortgage originators began to distribute more and more of their loans through private label MBS, GSEs lost the ability to monitor and control mortgage originators. Competition between the GSEs and private securitizers for loans further undermined GSEs power and strengthened mortgage originators. This contributed to a decline in underwriting standards and was a major cause of the financial crisis.

Investment bank securitizers were more willing to securitize risky loans because they generally retained minimal risk. Whereas the GSEs guaranteed the performance of their MBS, private securitizers generally did not, and might only retain a thin slice of risk.

From 2001 to 2003, financial institutions experienced high earnings due to an unprecedented re-financing boom brought about by historically low interest rates. When interest rates eventually rose, financial institutions sought to maintain their elevated earnings levels with a shift toward riskier mortgages and private label MBS distribution. Earnings depended on volume, so maintaining elevated earnings levels necessitated expanding the borrower pool using lower underwriting standards and new products that the GSEs would not (initially) securitize. Thus, the shift away from GSE securitization to private-label securitization (PLS) also corresponded with a shift in mortgage product type, from traditional, amortizing, fixed-rate mortgages (FRMs) to nontraditional, structurally riskier, nonamortizing, adjustable-rate mortgages (ARMs), and in the start of a sharp deterioration in mortgage underwriting standards.[22] The growth of PLS, however, forced the GSEs to lower their underwriting standards in an attempt to reclaim lost market share to please their private shareholders. Shareholder pressure pushed the GSEs into competition with PLS for market share, and the GSEs loosened their guarantee business underwriting standards in order to compete. In contrast, the wholly public FHA/Ginnie Mae maintained their underwriting standards and instead ceded market share.[22]

The growth of private-label securitization and lack of regulation in this part of the market resulted in the oversupply of underpriced housing finance[22] that led, in 2006, to an increasing number of borrowers, often with poor credit, who were unable to pay their mortgages—particularly with adjustable rate mortgages (ARM)—caused a precipitous increase in home foreclosures. As a result, home prices declined as increasing foreclosures added to the already large inventory of homes and stricter lending standards made it more and more difficult for borrowers to get mortgages. This depreciation in home prices led to growing losses for the GSEs, which back the majority of US mortgages. In July 2008, the government attempted to ease market fears by reiterating their view that "Fannie Mae and Freddie Mac play a central role in the US housing finance system". The U.S. Treasury Department and the Federal Reserve took steps to bolster confidence in the corporations, including granting both corporations access to Federal Reserve low-interest loans (at similar rates as commercial banks) and removing the prohibition on the Treasury Department to purchase the GSEs' stock. Despite these efforts, by August 2008, shares of both Fannie Mae and Freddie Mac had tumbled more than 90% from their one-year prior levels.

Company

Awards

- Freddie Mac was named one of the Best Places to Work for LGBTQ Equality in Human Rights Campaign's 2018 Corporate Equality Index[23]

- Freddie Mac was named one of the 100 Best Companies for Working Mothers in 2004 by Working Mothers magazine.

- Freddie Mac was ranked number 50 in the Fortune 500's 2007 rankings.[24]

- Freddie Mac was ranked number 20 in Forbes's Global 2,000 public companies rankings for 2009.

Credit rating

As of February 28, 2020.[25]

| Standard & Poor's | Moody's | Fitch | |

|---|---|---|---|

| Senior Long-Term Debt | AA+ | Aaa | AAA |

| Short-Term Debt | A-1+ | P-1 | F1+ |

| Subordinated Debt | A- | Aa2 | AA- |

| Preferred Stock | D | Ca | C/RR6 |

| Outlook | Stable | Stable | Stable |

Investigations

In 2003, Freddie Mac revealed that it had understated earnings by almost $5 billion, one of the largest corporate restatements in U.S. history. As a result, in November, it was fined $125 million—an amount called "peanuts" by Forbes magazine.[26]

On April 18, 2006, Freddie Mac was fined $3.8 million, by far the largest amount ever assessed by the Federal Election Commission, as a result of illegal campaign contributions. Freddie Mac was accused of illegally using corporate resources between 2000 and 2003 for 85 fundraisers that collected about $1.7 million for federal candidates. Much of the illegal fund raising benefited members of the House Financial Services Committee, a panel whose decisions can affect Freddie Mac. Notably, Freddie Mac held more than 40 fundraisers for House Financial Services Chairman Michael Oxley (R-OH).[27]

Government subsidies and bailout

Both Fannie Mae and Freddie Mac often benefited from an implied guarantee of fitness equivalent to truly federally backed financial groups.[28]

As of 2008, Fannie Mae and Freddie Mac owned or guaranteed about half of the U.S.'s $12 trillion mortgage market.[29] This made both corporations highly susceptible to the subprime mortgage crisis of that year. Ultimately, in July 2008, the speculation was made reality, when the US government took action to prevent the collapse of both corporations. The US Treasury Department and the Federal Reserve took several steps to bolster confidence in the corporations, including extending credit limits, granting both corporations access to Federal Reserve low-interest loans (at similar rates as commercial banks), and potentially allowing the Treasury Department to own stock.[30] This event also renewed calls for stronger regulation of GSEs by the government.

President Bush recommended a significant regulatory overhaul of the housing finance industry in 2003, but many Democrats opposed his plan, fearing that tighter regulation could greatly reduce financing for low-income housing, both low- and high-risk.[31] Bush opposed two other acts of legislation:[32][33] Senate Bill S. 190, the Federal Housing Enterprise Regulatory Reform Act of 2005, which was introduced in the Senate on January 26, 2005, sponsored by Senator Chuck Hagel (R–NE) and co-sponsored by Senators Elizabeth Dole (R–NC) and John Sununu (R–NH). S. 190 was reported out of the Senate Banking Committee on July 28, 2005, but never voted on by the full Senate.

On May 23, 2006, the Fannie Mae and Freddie Mac regulator, the Office of Federal Housing Enterprise Oversight, issued the results of a 27-month-long investigation.[34]

On May 25, 2006, Senator McCain joined as a co-sponsor to the Federal Housing Enterprise Regulatory Reform Act of 2005 (first put forward by Sen. Chuck Hagel)[35] where he pointed out that Fannie Mae and Freddie Mac's regulator reported that profits were "illusions deliberately and systematically created by the company's senior management".[36] However, this regulation too met with opposition from both Democrats and Republicans.[37]

Several executives of Fannie Mae or Freddie Mac include Kenneth Duberstein, former Chief of Staff to President Reagan, advisor to John McCain's Presidential Campaign in 2000, and President George W. Bush's transition team leader (Fannie Mae board member 1998–2007);[38] Franklin Raines, former Budget Director for President Clinton, CEO from 1999 to 2004—statements about his role as an advisor to the Obama presidential campaign have been determined to be false;[39] James Johnson, former aide to Democratic Vice-President Walter Mondale and ex-head of Obama's Vice-Presidential Selection Committee, CEO from 1991 to 1998; and Jamie Gorelick, former Deputy Attorney General to President Clinton, and Vice-Chairman from 1998 to 2003. In his position, Johnson earned an estimated $21 million; Raines earned an estimated $90 million; and Gorelick earned an estimated $26 million.[40] Three of these four top executives were also involved in mortgage-related financial scandals.[41][42]

The top 10 recipients of campaign contributions from Freddie Mac and Fannie Mae during the 1989 to 2008 time period include five Republicans and five Democrats. Top recipients of PAC money from these organizations include Roy Blunt (R-MO) $78,500 (total including individuals' contributions $96,950), Robert Bennett (R-UT) $71,499 (total $107,999), Spencer Bachus (R-AL) $70,500 (total $103,300), and Kit Bond (R-MO) $95,400 (total $64,000). The following Democrats received mostly individual contributions from employees, rather than PAC money: Christopher Dodd, (D-CT) $116,900 (but also $48,000 from the PACs), John Kerry, (D-MA) $109,000 ($2,000 from PACs), Barack Obama, (D-IL) $120,349 (only $6,000 from the PACs), Hillary Clinton, (D-NY) $68,050 (only $8,000 from PACs).[43] John McCain received $21,550 from these GSEs during this time, mostly individual money.[44] Freddie Mac also contributed $250,000 to the 2008 Republican National Convention in St. Paul, Minnesota according to FEC filings.[45] The organizers of the Democratic National Convention have not yet submitted their filings on how much they received from Freddie Mac and Fannie Mae.[45]

On Oct 21, 2010, government estimates revealed that the bailout of Freddie Mac and Fannie Mae will likely cost taxpayers $154 billion.[46]

Conservatorship

| Wikinews has related news: |

On September 7, 2008, Federal Housing Finance Agency (FHFA) Director James B. Lockhart III announced pursuant to the financial analysis, assessments and statutory authority of the FHFA, he had placed Fannie Mae and Freddie Mac under the conservatorship of the FHFA. FHFA has stated that there are no plans to liquidate the company.[6][7]

The announcement followed reports two days earlier that the Federal government was planning to take over Fannie Mae and Freddie Mac and had met with their CEOs on short notice.[47][48][49]

Under the reported plan, the federal government, via the FHFA, would place the two firms into conservatorship and for each entity, dismiss the chief executive officer, the present board of directors, elect a new board of directors, and cause to be issued new common stock to the federal government. The value of the common stock to pre-conservatorship holders would be greatly diminished, in the effort to maintain the value of company debt and of mortgage-backed securities.[8][47][48][49]

The authority of the U.S. Treasury to advance funds for the purpose of stabilizing Fannie Mae or Freddie Mac is limited only by the amount of debt that the entire federal government is permitted by law to commit to. The July 30, 2008, law enabling expanded regulatory authority over Fannie Mae and Freddie Mac increased the national debt ceiling by US$800 billion, to a total of US$10.7 trillion in anticipation of the potential need for the Treasury to have the flexibility to support the federal home loan banks.[50][51][52]

On September 7, 2008, the U.S. government took control of both Fannie Mae and Freddie Mac. Daniel Mudd (CEO of Fannie Mae) and Richard Syron (CEO of Freddie Mac) were replaced. Herbert M. Allison, former vice chairman of Merrill Lynch, took over Fannie Mae, and David M. Moffett, former vice chairman of US Bancorp, took over Freddie Mac.[53]

Related legislation

On May 8, 2013, Representatives Scott Garrett introduced the Budget and Accounting Transparency Act of 2014 (H.R. 1872; 113th Congress) into the United States House of Representatives during the 113th United States Congress. The bill, if it were passed, would modify the budgetary treatment of federal credit programs, such as Fannie Mae and Freddie Mac.[54] The bill would require that the cost of direct loans or loan guarantees be recognized in the federal budget on a fair-value basis using guidelines set forth by the Financial Accounting Standards Board.[54] The changes made by the bill would mean that Fannie Mae and Freddie Mac were counted on the budget instead of considered separately and would mean that the debt of those two programs would be included in the national debt.[55] These programs themselves would not be changed, but how they are accounted for in the United States federal budget would be. The goal of the bill is to improve the accuracy of how some programs are accounted for in the federal budget.[56]

See also

- Agency Securities

- Maxine B. Baker – President and CEO of the Freddie Mac Foundation, 1997–present

- Canada Mortgage and Housing Corporation

- Derivative (finance)

- Fannie Mae and Freddie Mac: A Bibliography

- Fannie Mae

- Farm Credit System

- Farmer Mac

- Ginnie Mae

- Government sponsored enterprise

- David Kellermann – late CFO of Freddie Mac

- Mortgage law

- Mortgage loan

- Sallie Mae

- Securitization

- USA Funds

References

- "Federal Home Loan Mortgage Corporation 2018 Annual Report (Form 10-K)". last10k.com. U.S. Securities and Exchange Commission. February 2019.

- "US SEC: Form 10-K Federal Home Loan Mortgage Corporation". U.S. Securities and Exchange Commission. Retrieved February 17, 2018.

- "Tysons Corner CDP, Virginia Archived 2011-11-10 at the Wayback Machine". United States Census Bureau. Retrieved on May 7, 2009.

- "Contact Us Archived 2009-05-14 at the Wayback Machine". Freddie Mac. Retrieved on May 12, 2009.

- "Fortune 500 Companies 2020: Who Made the List". Fortune. Retrieved 2020-11-10.

- Lockhart III, James B. (2008-09-07). "Statement of FHFA Director James B. Lockhart". Federal Housing Finance Agency. Archived from the original on 2008-09-12. Retrieved 2008-09-07.

- "Fact Sheet: Questions and Answers on Conservatorship" (PDF). Federal Housing Finance Agency. 2008-09-07. Archived from the original (PDF) on September 9, 2008. Retrieved 2008-09-07.

- Goldfarb, Zachary A.; David Cho; Binyamin Appelbaum (2008-09-07). "Treasury to Rescue Fannie and Freddie: Regulators Seek to Keep Firms' Troubles From Setting Off Wave of Bank Failures". The Washington Post. pp. A01. Retrieved 2008-09-07.

- "Freddie Mac courts investors, Buffett passes". August 22, 2008. Archived from the original on 2008-09-15. Retrieved 2017-01-03.

- Christie, Rebecca (September 7, 2008). "Paulson Engineers U.S. Takeover of Fannie, Freddie (Update4)". Bloomberg. Retrieved 2008-09-07.

- Adler, Lynn (June 16, 2010). "Fannie Mae, Freddie Mac to delist shares on NYSE". Reuters. Retrieved 2010-06-16.

- Grynbaum, Michael; Jolly, David (September 8, 2008). "U.S. Takeover of Mortgage Giants Lifts Stock Markets". The New York Times. Retrieved 2008-09-08.

- Leonnig, Carol D. (June 10, 2008). "How HUD Mortgage Policy Fed The Crisis". The Washington Post.

- "History of Fannie Mae & Freddie Mac Conservatorships | Federal Housing Finance Agency". www.fhfa.gov. Retrieved 2020-03-25.

- Lemke, Lins and Picard, Mortgage-Backed Securities, Chapters 2 and 4 (Thomson West, 2013 ed.).

- "Conforming Loan Limit". FHFA. Archived from the original on 15 March 2014. Retrieved 17 March 2014.

- "Freddie Mac Debt Securities: Freddie Notes FAQ". Freddiemac.com. Archived from the original on 2014-07-05. Retrieved 2014-06-19.

- Vernon L. Smith, "The Clinton Housing Bubble", The Wall Street Journal, December 18, 2007, pA20

- The Economist, "Fannie and Freddie ride again", July 5, 2007

- "CBO TESTIMONY Statement of Dan L. Crippen Director, Federal Subsidies for the Housing GSEs before the Subcommittee on Capital Markets, Insurance, and Government Sponsored Enterprises Committee on Financial Services U.S. House of Representatives, May 23, 2001". Cbo.gov. 2001-05-23. Retrieved 2014-06-19.

- Congressional Budget Office, Assessing the Public Costs and Benefits of Fannie Mae and Freddie Mac, May 1996

- Levitin, Adam J.; Wachter, Susan M. (April 12, 2012). "Explaining the Housing Bubble". Georgetown Law Journal. SSRN 1669401.

- "Best Places to Work 2018". Human Rights Campaign. Retrieved 2020-03-25.

- "Fortune 500 2007 - Freddie Mac". Fortune. Retrieved 2020-03-25.

- "Credit Ratings - Freddie Mac". Freddiemac.com. n.d. Retrieved 2014-06-19.

- "Shaking Steady Freddie". Forbes. 2003-12-11.

- "Freddie Mac pays record $3.8 million fine". NBC News. 2006-04-18. Retrieved 2014-06-19.

- Goodman, Wes; Shenn, Jody (February 20, 2009). "Fannie Mae Rescue Hindered as Asians Seek Guarantee (Update2)". Bloomberg. Retrieved 2009-02-20.

- Duhigg, Charles, "Loan-Agency Woes Swell From a Trickle to a Torrent", The New York Times, Friday, July 11, 2008

- Luhby, Tami, , CNN Money, July 14, 2008

- Labaton, Steven (2003-09-11). "New Agency Proposed to Oversee Freddie Mac and Fannie Mae". The New York Times. Retrieved 2009-08-25.

- "Statement of Administration Policy: H.R. 1461". Presidency.ucsb.edu. Retrieved 2014-06-19.

- "Statement of Administration Policy: H.R. 1427". Presidency.ucsb.edu. 2007-05-16. Retrieved 2014-06-19.

- "Report of the Special Examination of Fannie Mae May 2006" (PDF). Office of Federal Housing Enterprise Oversight. May 2006. Archived from the original (PDF) on 2008-09-16.

- govtrack.us

- govtrack.us, May 25, 2006 Archived October 10, 2008, at the Wayback Machine

- "Associated Press, Oct 20, 2008". NBC News. 2008-10-19. Retrieved 2014-06-19.

- PEU Report/State of the Division (2008-09-19). "State of the Division: Knowing McCain's Ken Duberstein". Stateofthedivision.blogspot.com. Retrieved 2014-06-19.

- "The Washington Post, Sept 19, 2008". Voices.washingtonpost.com. Retrieved 2014-06-19.

- "NationalPost, Jul 11, 2008". Retrieved October 20, 2008.

- "The Washington Post, Apr 6, 2005". Washingtonpost.com. Retrieved 2014-06-19.

- The New York Times, April 19, 2008

- OpenSecrets.org

- Lindsay Renick Mayer (2008-09-11). "OpenSecrets.org, Sep 11, 2008". Opensecrets.org. Retrieved 2014-06-19.

- Yahoo! News Archived October 25, 2008, at the Wayback Machine

- Davidson, Paul (2010-10-22). "Fannie, Freddie bailout to cost taxpayers $154 billion". USA Today.

- Hilzenrath, David S.; Zachary A. Goldfarb (2008-09-05). "Fannie Mae, Freddie Mac to be Put Under Federal Control, Sources Say". The Washington Post. Retrieved 2008-09-05.

- Labaton, Stephen; Andres Ross Sorkin (2008-09-05). "U.S. Rescue Seen at Hand for 2 Mortgage Giants". The New York Times. Retrieved 2008-09-05.

- Hilzenrath, David S.; Neil Irwin; Zachary A. Goldfarb (2008-09-06). "U.S. Nears Rescue Plan For Fannie And Freddie Deal Said to Involve Change of Leadership, Infusions of Capital". The Washington Post. pp. A1. Retrieved 2008-09-06.

- Herszenhorn, David (2008-07-27). "Congress Sends Housing Relief Bill to President". The New York Times. Retrieved 2008-09-06.

- Herszenhorn, David M. (2008-07-31). "Bush Signs Sweeping Housing Bill". The New York Times. Retrieved 2008-09-06.

- See HR 3221, signed into law as Public Law 110-289: A bill to provide needed housing reform and for other purposes.

Access to Legislative History: Library of Congress THOMAS: A bill to provide needed housing reform and for other purposes.

White House pre-signing statement: Statement of Administration Policy: H.R. 3221 – Housing and Economic Recovery Act of 2008 Archived September 9, 2008, at the Wayback Machine (July 23, 2008). Executive office of the President, Office of Management and Budget, Washington DC. - Ellis, David. "U.S. seizes Fannie and Freddie". CNN Money. Retrieved 2020-04-10.

- "H.R. 1872 - CBO" (PDF). United States Congress. Retrieved 28 March 2014.

- Kasperowicz, Pete (28 March 2014). "House to push budget reforms next week". The Hill. Retrieved 7 April 2014.

- Kasperowicz, Pete (4 April 2014). "Next week: Bring out the budget". The Hill. Retrieved 7 April 2014.

Further reading

- "Housing Policy and Debate" (PDF). Fannie Mae, Office of Housing Policy Research, Washington, DC.

- Labaton, Stephen; Weisman, Steven R. (2008-07-11). "U.S. Weighs Takeover of Two Mortgage Giants". The New York Times.

- Lemke, Thomas P.; Lins, Gerald T.; Picard, Marie E. (2013). Mortgage-Backed Securities. Thomson West.

External links

| By location | |

|---|---|

| Types | |

| Sectors | |

| Law and regulation | |

| Economics, financing and valuation | |

| Parties | |

| Other |

|

| |