Private equity

Private equity (PE) typically refers to investment funds, generally organized as limited partnerships, that buy and restructure companies that are not publicly traded.

| Financial market participants |

|---|

Private equity is a type of equity and one of the asset classes consisting of equity securities and debt in operating companies that are not publicly traded on a stock exchange.[1]

A private-equity investment will generally be made by a private-equity firm, a venture capital firm or an angel investor. Each of these categories of investors has its own set of goals, preferences and investment strategies; however, all provide working capital to a target company to nurture expansion, new-product development, or restructuring of the company's operations, management, or ownership.[2]

Common investment strategies in private equity include leveraged buyouts, venture capital, growth capital, distressed investments and mezzanine capital. In a typical leveraged-buyout transaction, a private-equity firm buys majority control of an existing or mature firm. This is distinct from a venture-capital or growth-capital investment, in which the investors (typically venture-capital firms or angel investors) invest in young, growing or emerging companies, and rarely obtain majority control.

Private equity is also often grouped into a broader category called private capital, generally used to describe capital supporting any long-term, illiquid investment strategy.[3]

The key features of private-equity operations are generally as follows.

- A private-equity manager uses the money of investors to fund its acquisitions – investors are e.g. hedge funds, pension funds, university endowments or wealthy individuals.

- It restructures the acquired firm (or firms) and attempts to resell at a higher value, aiming for a high return on equity. The restructuring often involves cutting costs, which produces higher profits in the short term, but can probably do long-term damage to customer relationships and workforce morale.

- Private equity makes extensive use of debt financing to purchase companies in use of leverage – hence the earlier name for private-equity operations: leveraged buy-outs. (A small increase in firm value – for example, a growth of asset price by 20% – can lead to 100% return on equity, if the amount the private-equity fund put down to buy the company in the first place was only 20% down and 80% debt. However, if the private-equity firm fails to make the target grow in value, losses will be large.) Additionally, debt financing reduces corporate taxation burdens, as interest payments are tax-deductible, and is one of the principal ways in which profits for investors are enhanced.

- Because innovations tend to be produced by outsiders and founders in startups, rather than existing organizations, private equity targets startups to create value by overcoming agency costs and better aligning the incentives of corporate managers with those of their shareholders. This means a greater share of firm retained earnings is taken out of the firm to distribute to shareholders than is reinvested in the firm's workforce or equipment. When private equity purchases a very small startup it can behave like venture capital and help the small firm reach a wider market. However, when private equity purchases a larger firm, the experience of being managed by private equity may lead to loss of product quality and low morale among the employees.[4][5]

- Private-equity investors often syndicate their transactions to other buyers to achieve benefits that include diversification of different types of target risk, the combination of complementary investor information and skillsets, and an increase in future deal flow.[6]

Bloomberg Businessweek has called "private equity" a rebranding of leveraged-buyout firms after the 1980s.

Strategies

The strategies private-equity firms may use are as follows, leveraged buyout being the most important.

Leveraged buyout

Leveraged buyout, LBO, or Buyout refers to a strategy of making equity investments as part of a transaction in which a company, business unit, or business assets is acquired from the current shareholders typically with the use of financial leverage.[7] The companies involved in these transactions are typically mature and generate operating cash flows.[8]

Private-equity firms view target companies as either Platform companies which have sufficient scale and a successful business model to act as a stand-alone entity, or as add-on / tuck-in / bolt-on acquisitions, which would include companies with insufficient scale or other deficits.[9][10]

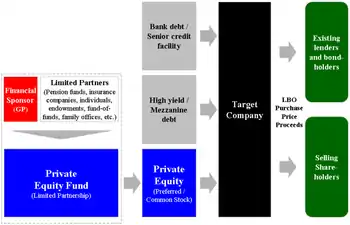

Leveraged buyouts involve a financial sponsor agreeing to an acquisition without itself committing all the capital required for the acquisition. To do this, the financial sponsor will raise acquisition debt which ultimately looks to the cash flows of the acquisition target to make interest and principal payments.[11] Acquisition debt in an LBO is often non-recourse to the financial sponsor and has no claim on other investments managed by the financial sponsor. Therefore, an LBO transaction's financial structure is particularly attractive to a fund's limited partners, allowing them the benefits of leverage but greatly limiting the degree of recourse of that leverage. This kind of financing structure leverage benefits an LBO's financial sponsor in two ways: (1) the investor itself only needs to provide a fraction of the capital for the acquisition, and (2) the returns to the investor will be enhanced (as long as the return on assets exceeds the cost of the debt).[12]

As a percentage of the purchase price for a leverage buyout target, the amount of debt used to finance a transaction varies according to the financial condition and history of the acquisition target, market conditions, the willingness of lenders to extend credit (both to the LBO's financial sponsors and the company to be acquired) as well as the interest costs and the ability of the company to cover those costs. Historically the debt portion of a LBO will range from 60%–90% of the purchase price.[13] Between 2000–2005 debt averaged between 59.4% and 67.9% of total purchase price for LBOs in the United States.[14]

Simple example of leveraged buyout

A private-equity fund, ABC Capital II, borrows $9bn from a bank (or other lender). To this, it adds $2bn of equity – money from its own partners and from limited partners. With this $11bn it buys all the shares of an underperforming company, XYZ Industrial (after due diligence, i.e. checking the books). It replaces the senior management in XYZ Industrial, and they set out to streamline it. The workforce is reduced, some assets are sold off, etc. The objective is to increase the value of the company for an early sale.

The stock market is experiencing a bull market, and XYZ Industrial is sold two years after the buy-out for $13bn, yielding a profit of $2bn. The original loan can now be paid off with interest of, say, $0.5bn. The remaining profit of $1.5bn is shared among the partners. Taxation of such gains is at capital gains rates.

Note that part of that profit results from turning the company around, and part results from the general increase in share prices in a buoyant stock market, the latter often being the greater component.[15]

Notes:

- The lenders (the people who put up the $9bn in the example) can insure against default by syndicating the loan to spread the risk, or by buying credit default swaps (CDSs) or selling collateralised debt obligations (CDOs) from/to other institutions (although this is no business of the private-equity firm).

- Often the loan/equity ($11bn above) is not paid off after sale but left on the books of the company (XYZ Industrial) for it to pay off over time. This can be advantageous since the interest is largely offsettable against the profits of the company, thus reducing, or even eliminating, tax.

- Most buyout deals are much smaller; the global average purchase in 2013 was $89m, for example.[16]

- The target company (XYZ Industrials here) does not have to be floated on the stock market; indeed most buyout exits are not IPOs.

- Buy-out operations can go wrong and in such cases, the loss is increased by leverage, just as the profit is if all goes well.

Growth capital

Growth Capital refers to equity investments, most often minority investments, in relatively mature companies that are looking for capital to expand or restructure operations, enter new markets or finance a major acquisition without a change of control of the business.[17]

Companies that seek growth capital will often do so in order to finance a transformational event in their life cycle. These companies are likely to be more mature than venture capital-funded companies, able to generate revenue and operating profits but unable to generate sufficient cash to fund major expansions, acquisitions or other investments. Because of this lack of scale, these companies generally can find few alternative conduits to secure capital for growth, so access to growth equity can be critical to pursue necessary facility expansion, sales and marketing initiatives, equipment purchases, and new product development.[18]

The primary owner of the company may not be willing to take the financial risk alone. By selling part of the company to private equity, the owner can take out some value and share the risk of growth with partners.[19] Capital can also be used to effect a restructuring of a company's balance sheet, particularly to reduce the amount of leverage (or debt) the company has on its balance sheet.[20]

A Private investment in public equity, or PIPEs, refer to a form of growth capital investment made into a publicly traded company. PIPE investments are typically made in the form of a convertible or preferred security that is unregistered for a certain period of time.[21][22]

The Registered Direct, or RD, is another common financing vehicle used for growth capital. A registered direct is similar to a PIPE but is instead sold as a registered security.

Mezzanine capital

Mezzanine capital refers to subordinated debt or preferred equity securities that often represent the most junior portion of a company's capital structure that is senior to the company's common equity. This form of financing is often used by private-equity investors to reduce the amount of equity capital required to finance a leveraged buyout or major expansion. Mezzanine capital, which is often used by smaller companies that are unable to access the high yield market, allows such companies to borrow additional capital beyond the levels that traditional lenders are willing to provide through bank loans.[23] In compensation for the increased risk, mezzanine debt holders require a higher return for their investment than secured or other more senior lenders.[24][25] Mezzanine securities are often structured with a current income coupon.

Venture capital

Venture capital[26] or VC is a broad subcategory of private equity that refers to equity investments made, typically in less mature companies, for the launch of a seed or startup company, early-stage development, or expansion of a business. Venture investment is most often found in the application of new technology, new marketing concepts and new products that do not have a proven track record or stable revenue streams.[27][28]

Venture capital is often sub-divided by the stage of development of the company ranging from early-stage capital used for the launch of startup companies to late stage and growth capital that is often used to fund expansion of existing business that are generating revenue but may not yet be profitable or generating cash flow to fund future growth.[29]

Entrepreneurs often develop products and ideas that require substantial capital during the formative stages of their companies' life cycles.[30] Many entrepreneurs do not have sufficient funds to finance projects themselves, and they must, therefore, seek outside financing.[31] The venture capitalist's need to deliver high returns to compensate for the risk of these investments makes venture funding an expensive capital source for companies. Being able to secure financing is critical to any business, whether it is a startup seeking venture capital or a mid-sized firm that needs more cash to grow.[32] Venture capital is most suitable for businesses with large up-front capital requirements which cannot be financed by cheaper alternatives such as debt. Although venture capital is often most closely associated with fast-growing technology, healthcare and biotechnology fields, venture funding has been used for other more traditional businesses.[27][33]

Investors generally commit to venture capital funds as part of a wider diversified private-equity portfolio, but also to pursue the larger returns the strategy has the potential to offer. However, venture capital funds have produced lower returns for investors over recent years compared to other private-equity fund types, particularly buyout.

Distressed and special situations

Distressed or Special Situations is a broad category referring to investments in equity or debt securities of financially stressed companies.[34][35][36] The "distressed" category encompasses two broad sub-strategies including:

- "Distressed-to-Control" or "Loan-to-Own" strategies where the investor acquires debt securities in the hopes of emerging from a corporate restructuring in control of the company's equity;[37]

- "Special Situations" or "Turnaround" strategies where an investor will provide debt and equity investments, often "rescue financing" to companies undergoing operational or financial challenges.[38]

In addition to these private-equity strategies, hedge funds employ a variety of distressed investment strategies including the active trading of loans and bonds issued by distressed companies.[39]

Secondaries

Secondary investments refer to investments made in existing private-equity assets. These transactions can involve the sale of private-equity fund interests or portfolios of direct investments in privately held companies through the purchase of these investments from existing institutional investors.[40] By its nature, the private-equity asset class is illiquid, intended to be a long-term investment for buy and hold investors. Secondary investments provide institutional investors with the ability to improve vintage diversification, particularly for investors that are new to the asset class. Secondaries also typically experience a different cash flow profile, diminishing the j-curve effect of investing in new private-equity funds.[41][42] Often investments in secondaries are made through third-party fund vehicle, structured similar to a fund of funds although many large institutional investors have purchased private-equity fund interests through secondary transactions.[43] Sellers of private-equity fund investments sell not only the investments in the fund but also their remaining unfunded commitments to the funds.

Other strategies

Other strategies that can be considered private equity or a close adjacent market include:

- Real estate: in the context of private equity this will typically refer to the riskier end of the investment spectrum including "value-added" and opportunity funds where the investments often more closely resemble leveraged buyouts than traditional real estate investments. Certain investors in private equity consider real estate to be a separate asset class.

- Infrastructure: investments in various public works (e.g., bridges, tunnels, toll roads, airports, public transportation, and other public works) that are made typically as part of a privatization initiative on the part of a government entity.[44][45][46]

- Energy and Power: investments in a wide variety of companies (rather than assets) engaged in the production and sale of energy, including fuel extraction, manufacturing, refining and distribution (Energy) or companies engaged in the production or transmission of electrical power (Power).

- Merchant banking: negotiated private-equity investment by financial institutions in the unregistered securities of either privately or publicly held companies.[47]

- Fund of funds: investments made in a fund whose primary activity is investing in other private-equity funds. The fund of funds model is used by investors looking for:

- Diversification but have insufficient capital to diversify their portfolio by themselves

- Access to top-performing funds that are otherwise oversubscribed

- Experience in a particular fund type or strategy before investing directly in funds in that niche

- Exposure to difficult-to-reach and/or emerging markets

- Superior fund selection by high-talent fund of fund managers/teams

- Royalty fund: an investment that purchases a consistent revenue stream deriving from the payment of royalties. One growing subset of this category is the healthcare royalty fund, in which a private-equity fund manager purchases a royalty stream paid by a pharmaceutical company to a drug patent holder. The drug patent holder can be another company, an individual inventor, or some sort of institution, such as a research university.[48]

History and development

| History of private equity and venture capital |

|---|

.jpg.webp) |

| Early history |

| (origins of modern private equity) |

| The 1980s |

| (leveraged buyout boom) |

| The 1990s |

| (leveraged buyout and the venture capital bubble) |

| The 2000s |

| (dot-com bubble to the credit crunch) |

Early history and the development of venture capital

The seeds of the US private-equity industry were planted in 1946 with the founding of two venture capital firms: American Research and Development Corporation (ARDC) and J.H. Whitney & Company.[49] Before World War II, venture capital investments (originally known as "development capital") were primarily the domain of wealthy individuals and families. In 1901 J.P. Morgan arguably managed the first leveraged buyout of the Carnegie Steel Company using private equity.[50] Modern era private equity, however, is credited to Georges Doriot, the "father of venture capitalism" with the founding of ARDC[51] and founder of INSEAD, with capital raised from institutional investors, to encourage private sector investments in businesses run by soldiers who were returning from World War II. ARDC is credited with the first major venture capital success story when its 1957 investment of $70,000 in Digital Equipment Corporation (DEC) would be valued at over $355 million after the company's initial public offering in 1968 (representing a return of over 5,000 times on its investment and an annualized rate of return of 101%).[52][53] It is commonly noted that the first venture-backed startup is Fairchild Semiconductor (which produced the first commercially practicable integrated circuit), funded in 1959 by what would later become Venrock Associates.[54]

Origins of the leveraged buyout

The first leveraged buyout may have been the purchase by McLean Industries, Inc. of Pan-Atlantic Steamship Company in January 1955 and Waterman Steamship Corporation in May 1955[55] Under the terms of that transaction, McLean borrowed $42 million and raised an additional $7 million through an issue of preferred stock. When the deal closed, $20 million of Waterman cash and assets were used to retire $20 million of the loan debt.[56] Lewis Cullman's acquisition of Orkin Exterminating Company in 1964 is often cited as the first leveraged buyout.[57][58] Similar to the approach employed in the McLean transaction, the use of publicly traded holding companies as investment vehicles to acquire portfolios of investments in corporate assets was a relatively new trend in the 1960s popularized by the likes of Warren Buffett (Berkshire Hathaway) and Victor Posner (DWG Corporation) and later adopted by Nelson Peltz (Triarc), Saul Steinberg (Reliance Insurance) and Gerry Schwartz (Onex Corporation). These investment vehicles would utilize a number of the same tactics and target the same type of companies as more traditional leveraged buyouts and in many ways could be considered a forerunner of the later private-equity firms. In fact it is Posner who is often credited with coining the term "leveraged buyout" or "LBO".[59]

The leveraged buyout boom of the 1980s was conceived by a number of corporate financiers, most notably Jerome Kohlberg Jr. and later his protégé Henry Kravis. Working for Bear Stearns at the time, Kohlberg and Kravis along with Kravis' cousin George Roberts began a series of what they described as "bootstrap" investments. Many of these companies lacked a viable or attractive exit for their founders as they were too small to be taken public and the founders were reluctant to sell out to competitors and so a sale to a financial buyer could prove attractive.[60] In the following years the three Bear Stearns bankers would complete a series of buyouts including Stern Metals (1965), Incom (a division of Rockwood International, 1971), Cobblers Industries (1971), and Boren Clay (1973) as well as Thompson Wire, Eagle Motors and Barrows through their investment in Stern Metals.[61] By 1976, tensions had built up between Bear Stearns and Kohlberg, Kravis and Roberts leading to their departure and the formation of Kohlberg Kravis Roberts in that year.

Private equity in the 1980s

In January 1982, former United States Secretary of the Treasury William E. Simon and a group of investors acquired Gibson Greetings, a producer of greeting cards, for $80 million, of which only $1 million was rumored to have been contributed by the investors. By mid-1983, just sixteen months after the original deal, Gibson completed a $290 million IPO and Simon made approximately $66 million.[62][63]

The success of the Gibson Greetings investment attracted the attention of the wider media to the nascent boom in leveraged buyouts. Between 1979 and 1989, it was estimated that there were over 2,000 leveraged buyouts valued in excess of $250 million.[64]

During the 1980s, constituencies within acquired companies and the media ascribed the "corporate raid" label to many private-equity investments, particularly those that featured a hostile takeover of the company, perceived asset stripping, major layoffs or other significant corporate restructuring activities. Among the most notable investors to be labeled corporate raiders in the 1980s included Carl Icahn, Victor Posner, Nelson Peltz, Robert M. Bass, T. Boone Pickens, Harold Clark Simmons, Kirk Kerkorian, Sir James Goldsmith, Saul Steinberg and Asher Edelman. Carl Icahn developed a reputation as a ruthless corporate raider after his hostile takeover of TWA in 1985.[65][66][67] Many of the corporate raiders were onetime clients of Michael Milken, whose investment banking firm, Drexel Burnham Lambert helped raise blind pools of capital with which corporate raiders could make a legitimate attempt to take over a company and provided high-yield debt ("junk bonds") financing of the buyouts.

One of the final major buyouts of the 1980s proved to be its most ambitious and marked both a high-water mark and a sign of the beginning of the end of the boom that had begun nearly a decade earlier. In 1989, KKR (Kohlberg Kravis Roberts) closed in on a $31.1 billion takeover of RJR Nabisco. It was, at that time and for over 17 years, the largest leveraged buyout in history. The event was chronicled in the book (and later the movie), Barbarians at the Gate: The Fall of RJR Nabisco. KKR would eventually prevail in acquiring RJR Nabisco at $109 per share, marking a dramatic increase from the original announcement that Shearson Lehman Hutton would take RJR Nabisco private at $75 per share. A fierce series of negotiations and horse-trading ensued which pitted KKR against Shearson and later Forstmann Little & Co. Many of the major banking players of the day, including Morgan Stanley, Goldman Sachs, Salomon Brothers, and Merrill Lynch were actively involved in advising and financing the parties. After Shearson's original bid, KKR quickly introduced a tender offer to obtain RJR Nabisco for $90 per share—a price that enabled it to proceed without the approval of RJR Nabisco's management. RJR's management team, working with Shearson and Salomon Brothers, submitted a bid of $112, a figure they felt certain would enable them to outflank any response by Kravis's team. KKR's final bid of $109, while a lower dollar figure, was ultimately accepted by the board of directors of RJR Nabisco.[68] At $31.1 billion of transaction value, RJR Nabisco was by far the largest leveraged buyouts in history. In 2006 and 2007, a number of leveraged buyout transactions were completed that for the first time surpassed the RJR Nabisco leveraged buyout in terms of nominal purchase price. However, adjusted for inflation, none of the leveraged buyouts of the 2006–2007 period would surpass RJR Nabisco. By the end of the 1980s the excesses of the buyout market were beginning to show, with the bankruptcy of several large buyouts including Robert Campeau's 1988 buyout of Federated Department Stores, the 1986 buyout of the Revco drug stores, Walter Industries, FEB Trucking and Eaton Leonard. Additionally, the RJR Nabisco deal was showing signs of strain, leading to a recapitalization in 1990 that involved the contribution of $1.7 billion of new equity from KKR.[69] In the end, KKR lost $700 million on RJR.[70]

Drexel reached an agreement with the government in which it pleaded nolo contendere (no contest) to six felonies – three counts of stock parking and three counts of stock manipulation.[71] It also agreed to pay a fine of $650 million – at the time, the largest fine ever levied under securities laws. Milken left the firm after his own indictment in March 1989.[72][73] On 13 February 1990 after being advised by United States Secretary of the Treasury Nicholas F. Brady, the U.S. Securities and Exchange Commission (SEC), the New York Stock Exchange and the Federal Reserve, Drexel Burnham Lambert officially filed for Chapter 11 bankruptcy protection.[72]

Age of the mega-buyout: 2005–2007

The combination of decreasing interest rates, loosening lending standards and regulatory changes for publicly traded companies (specifically the Sarbanes–Oxley Act) would set the stage for the largest boom private equity had seen. Marked by the buyout of Dex Media in 2002, large multibillion-dollar U.S. buyouts could once again obtain significant high yield debt financing and larger transactions could be completed. By 2004 and 2005, major buyouts were once again becoming common, including the acquisitions of Toys "R" Us,[74] The Hertz Corporation,[75][76] Metro-Goldwyn-Mayer[77] and SunGard[78] in 2005.

As 2005 ended and 2006 began, new "largest buyout" records were set and surpassed several times with nine of the top ten buyouts at the end of 2007 having been announced in an 18-month window from the beginning of 2006 through the middle of 2007. In 2006, private-equity firms bought 654 U.S. companies for $375 billion, representing 18 times the level of transactions closed in 2003.[79] Additionally, U.S.-based private-equity firms raised $215.4 billion in investor commitments to 322 funds, surpassing the previous record set in 2000 by 22% and 33% higher than the 2005 fundraising total[80] The following year, despite the onset of turmoil in the credit markets in the summer, saw yet another record year of fundraising with $302 billion of investor commitments to 415 funds[81] Among the mega-buyouts completed during the 2006 to 2007 boom were: EQ Office, HCA,[82] Alliance Boots[83] and TXU.[84]

In July 2007, the turmoil that had been affecting the mortgage markets, spilled over into the leveraged finance and high-yield debt markets.[85][86] The markets had been highly robust during the first six months of 2007, with highly issuer friendly developments including PIK and PIK Toggle (interest is "Payable In Kind") and covenant light debt widely available to finance large leveraged buyouts. July and August saw a notable slowdown in issuance levels in the high yield and leveraged loan markets with few issuers accessing the market. Uncertain market conditions led to a significant widening of yield spreads, which coupled with the typical summer slowdown led many companies and investment banks to put their plans to issue debt on hold until the autumn. However, the expected rebound in the market after 1 May 2007 did not materialize, and the lack of market confidence prevented deals from pricing. By the end of September, the full extent of the credit situation became obvious as major lenders including Citigroup and UBS AG announced major writedowns due to credit losses. The leveraged finance markets came to a near standstill during a week in 2007.[87] As 2007 ended and 2008 began, it was clear that lending standards had tightened and the era of "mega-buyouts" had come to an end. Nevertheless, private equity continues to be a large and active asset class and the private-equity firms, with hundreds of billions of dollars of committed capital from investors are looking to deploy capital in new and different transactions.

As a result of the global financial crisis, private equity has become subject to increased regulation in Europe and is now subject, among other things, to rules preventing asset stripping of portfolio companies and requiring the notification and disclosure of information in connection with buy-out activity.[88][89]

Staying private for longer

With the increased availability and scope of funding provided by private markets, many companies are staying private simply because they can. McKinsey & Company reports in its Global Private Markets Review 2018 that global private market fundraising increased by $28.2 billion from 2017, for a total of $748 billion in 2018.[90] Thus, given the abundance of private capital available, companies no longer require public markets for sufficient funding. Benefits may include avoiding the cost of an IPO (the average operating company going public in 2019 paid $750, 000 USD[91]), maintaining more control of the company, and having the 'legroom' to think long-term rather than focus on short-term or quarterly figures.

Investments in private equity

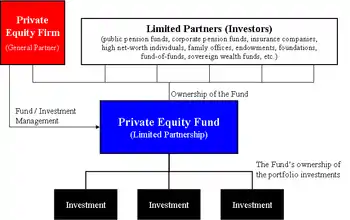

Although the capital for private equity originally came from individual investors or corporations, in the 1970s, private equity became an asset class in which various institutional investors allocated capital in the hopes of achieving risk-adjusted returns that exceed those possible in the public equity markets. In the 1980s, insurers were major private-equity investors. Later, public pension funds and university and other endowments became more significant sources of capital.[92] For most institutional investors, private-equity investments are made as part of a broad asset allocation that includes traditional assets (e.g., public equity and bonds) and other alternative assets (e.g., hedge funds, real estate, commodities).

Investor categories

US, Canadian and European public and private pension schemes have invested in the asset class since the early 1980s to diversify away from their core holdings (public equity and fixed income).[93] Today pension investment in private equity accounts for more than a third of all monies allocated to the asset class, ahead of other institutional investors such as insurance companies, endowments, and sovereign wealth funds.

Direct vs. indirect investment

Most institutional investors do not invest directly in privately held companies, lacking the expertise and resources necessary to structure and monitor the investment. Instead, institutional investors will invest indirectly through a private-equity fund. Certain institutional investors have the scale necessary to develop a diversified portfolio of private-equity funds themselves, while others will invest through a fund of funds to allow a portfolio more diversified than one a single investor could construct.

Investment timescales

Returns on private-equity investments are created through one or a combination of three factors that include: debt repayment or cash accumulation through cash flows from operations, operational improvements that increase earnings over the life of the investment and multiple expansion, selling the business for a higher price than was originally paid. A key component of private equity as an asset class for institutional investors is that investments are typically realized after some period of time, which will vary depending on the investment strategy. Private-equity investment returns are typically realized through one of the following avenues:

- an initial public offering (IPO) – shares of the company are offered to the public, typically providing a partial immediate realization to the financial sponsor as well as a public market into which it can later sell additional shares;

- a merger or acquisition – the company is sold for either cash or shares in another company;

- a recapitalization – cash is distributed to the shareholders (in this case the financial sponsor) and its private-equity funds either from cash flow generated by the company or through raising debt or other securities to fund the distribution.

Large institutional asset owners such as pension funds (with typically long-dated liabilities), insurance companies, sovereign wealth and national reserve funds have a generally low likelihood of facing liquidity shocks in the medium term, and thus can afford the required long holding periods characteristic of private-equity investment.[93]

The median horizon for a LBO transaction is 8 years.[94]

Liquidity in the private-equity market

The private-equity secondary market (also often called private-equity secondaries) refers to the buying and selling of pre-existing investor commitments to private equity and other alternative investment funds. Sellers of private-equity investments sell not only the investments in the fund but also their remaining unfunded commitments to the funds. By its nature, the private-equity asset class is illiquid, intended to be a long-term investment for buy-and-hold investors. For the vast majority of private-equity investments, there is no listed public market; however, there is a robust and maturing secondary market available for sellers of private-equity assets.

Increasingly, secondaries are considered a distinct asset class with a cash flow profile that is not correlated with other private-equity investments. As a result, investors are allocating capital to secondary investments to diversify their private-equity programs. Driven by strong demand for private-equity exposure, a significant amount of capital has been committed to secondary investments from investors looking to increase and diversify their private-equity exposure.

Investors seeking access to private equity have been restricted to investments with structural impediments such as long lock-up periods, lack of transparency, unlimited leverage, concentrated holdings of illiquid securities and high investment minimums.

Secondary transactions can be generally split into two basic categories:

- Sale of limited-partnership interests

- The most common secondary transaction, this category includes the sale of an investor's interest in a private-equity fund or portfolio of interests in various funds through the transfer of the investor's limited-partnership interest in the fund(s). Nearly all types of private-equity funds (e.g., including buyout, growth equity, venture capital, mezzanine, distressed and real estate) can be sold in the secondary market. The transfer of the limited partnership interest typically will allow the investor to receive some liquidity for the funded investments as well as a release from any remaining unfunded obligations to the fund.

- Sale of direct interests, secondary directs or synthetic secondaries

- This category refers to the sale of portfolios of direct investments in operating companies, rather than limited partnership interests in investment funds. These portfolios historically have originated from either corporate development programs or large financial institutions.

Private-equity firms

According to an updated 2017 ranking created by industry magazine Private Equity International[95] (published by PEI Media called the PEI 300), the largest private-equity firm in the world today is The Blackstone Group based on the amount of private-equity direct-investment capital raised over a five-year window. The 10 most prominent private-equity firms in the world are:

- The Blackstone Group

- Sycamore Partners

- Kohlberg Kravis Roberts

- The Carlyle Group

- TPG Capital

- Warburg Pincus

- Advent International Corporation

- Apollo Global Management

- EnCap Investments

- CVC Capital Partners

Because private-equity firms are continuously in the process of raising, investing and distributing their private-equity funds, capital raised can often be the easiest to measure. Other metrics can include the total value of companies purchased by a firm or an estimate of the size of a firm's active portfolio plus capital available for new investments. As with any list that focuses on size, the list does not provide any indication as to relative investment performance of these funds or managers.

Preqin, an independent data provider, ranks the 25 largest private-equity investment managers. Among the larger firms in the 2017 ranking were AlpInvest Partners, Ardian (formerly AXA Private Equity), AIG Investments, and Goldman Sachs Capital Partners. Invest Europe publishes a yearbook which analyses industry trends derived from data disclosed by over 1,300 European private-equity funds.[96] Finally, websites such as AskIvy.net[97] provide lists of London-based private-equity firms.

Versus hedge funds

The investment strategies of private-equity firms differ from those of hedge funds. Typically, private-equity investment groups are geared towards long-hold, multiple-year investment strategies in illiquid assets (whole companies, large-scale real estate projects, or other tangibles not easily converted to cash) where they have more control and influence over operations or asset management to influence their long-term returns. Hedge funds usually focus on short or medium term liquid securities which are more quickly convertible to cash, and they do not have direct control over the business or asset in which they are investing.[98] Both private-equity firms and hedge funds often specialize in specific types of investments and transactions. Private-equity specialization is usually in specific industry sector asset management while hedge fund specialization is in industry sector risk capital management. Private-equity strategies can include wholesale purchase of a privately held company or set of assets, mezzanine financing for startup projects, growth capital investments in existing businesses or leveraged buyout of a publicly held asset converting it to private control.[99] Finally, private-equity firms only take long positions, for short selling is not possible in this asset class.

Private-equity funds

Private-equity fundraising refers to the action of private-equity firms seeking capital from investors for their funds. Typically an investor will invest in a specific fund managed by a firm, becoming a limited partner in the fund, rather than an investor in the firm itself. As a result, an investor will only benefit from investments made by a firm where the investment is made from the specific fund in which it has invested.

- Fund of funds. These are private-equity funds that invest in other private-equity funds in order to provide investors with a lower risk product through exposure to a large number of vehicles often of different type and regional focus. Fund of funds accounted for 14% of global commitments made to private-equity funds in 2006.

- Individuals with substantial net worth. Substantial net worth is often required of investors by the law, since private-equity funds are generally less regulated than ordinary mutual funds. For example, in the US, most funds require potential investors to qualify as accredited investors, which requires $1 million of net worth, $200,000 of individual income, or $300,000 of joint income (with spouse) for two documented years and an expectation that such income level will continue.

As fundraising has grown over the past few years, so too has the number of investors in the average fund. In 2004 there were 26 investors in the average private-equity fund, this figure has now grown to 42 according to Preqin ltd. (formerly known as Private Equity Intelligence).

The managers of private-equity funds will also invest in their own vehicles, typically providing between 1–5% of the overall capital.

Often private-equity fund managers will employ the services of external fundraising teams known as placement agents in order to raise capital for their vehicles. The use of placement agents has grown over the past few years, with 40% of funds closed in 2006 employing their services, according to Preqin ltd. Placement agents will approach potential investors on behalf of the fund manager, and will typically take a fee of around 1% of the commitments that they are able to garner.

The amount of time that a private-equity firm spends raising capital varies depending on the level of interest among investors, which is defined by current market conditions and also the track record of previous funds raised by the firm in question. Firms can spend as little as one or two months raising capital when they are able to reach the target that they set for their funds relatively easily, often through gaining commitments from existing investors in their previous funds, or where strong past performance leads to strong levels of investor interest. Other managers may find fundraising taking considerably longer, with managers of less popular fund types (such as US and European venture fund managers in the current climate) finding the fundraising process more tough. It is not unheard of for funds to spend as long as two years on the road seeking capital, although the majority of fund managers will complete fundraising within nine months to fifteen months.

Once a fund has reached its fundraising target, it will have a final close. After this point it is not normally possible for new investors to invest in the fund, unless they were to purchase an interest in the fund on the secondary market.

Size of the industry

The state of the industry around the end of 2011 was as follows.[100]

Private-equity assets under management probably exceeded $2.0 trillion at the end of March 2012, and funds available for investment totalled $949bn (about 47% of overall assets under management).

Some $246bn of private equity was invested globally in 2011, down 6% on the previous year and around two-thirds below the peak activity in 2006 and 2007. Following on from a strong start, deal activity slowed in the second half of 2011 due to concerns over the global economy and sovereign debt crisis in Europe. There was $93bn in investments during the first half of this year as the slowdown persisted into 2012. This was down a quarter on the same period in the previous year. Private-equity backed buyouts generated some 6.9% of global M&A volume in 2011 and 5.9% in the first half of 2012. This was down on 7.4% in 2010 and well below the all-time high of 21% in 2006.

Global exit activity totalled $252bn in 2011, practically unchanged from the previous year, but well up on 2008 and 2009 as private-equity firms sought to take advantage of improved market conditions at the start of the year to realise investments. Exit activity however, has lost momentum following a peak of $113bn in the second quarter of 2011. TheCityUK estimates total exit activity of some $100bn in the first half of 2012, well down on the same period in the previous year.

The fund raising environment remained stable for the third year running in 2011 with $270bn in new funds raised, slightly down on the previous year's total. Around $130bn in funds was raised in the first half of 2012, down around a fifth on the first half of 2011. The average time for funds to achieve a final close fell to 16.7 months in the first half of 2012, from 18.5 months in 2011. Private-equity funds available for investment ("dry powder") totalled $949bn at the end of q1-2012, down around 6% on the previous year. Including unrealised funds in existing investments, private-equity funds under management probably totalled over $2.0 trillion.

Public pensions are a major source of capital for private-equity funds. Increasingly, sovereign wealth funds are growing as an investor class for private equity.[101]

Private-equity fund performance

Due to limited disclosure, studying the returns to private equity is relatively difficult. Unlike mutual funds, private-equity funds need not disclose performance data. And, as they invest in private companies, it is difficult to examine the underlying investments. It is challenging to compare private-equity performance to public-equity performance, in particular because private-equity fund investments are drawn and returned over time as investments are made and subsequently realized.

An oft-cited academic paper (Kaplan and Schoar, 2005)[102] suggests that the net-of-fees returns to PE funds are roughly comparable to the S&P 500 (or even slightly under). This analysis may actually overstate the returns because it relies on voluntarily reported data and hence suffers from survivorship bias (i.e. funds that fail won't report data). One should also note that these returns are not risk-adjusted. A more recent paper (Harris, Jenkinson and Kaplan, 2012)[103] found that average buyout fund returns in the U.S. have actually exceeded that of public markets. These findings were supported by earlier work, using a different data set (Robinson and Sensoy, 2011).[104]

Commentators have argued that a standard methodology is needed to present an accurate picture of performance, to make individual private-equity funds comparable and so the asset class as a whole can be matched against public markets and other types of investment. It is also claimed that PE fund managers manipulate data to present themselves as strong performers, which makes it even more essential to standardize the industry.[105]

Two other findings in Kaplan and Schoar (2005): First, there is considerable variation in performance across PE funds. Second, unlike the mutual fund industry, there appears to be performance persistence in PE funds. That is, PE funds that perform well over one period, tend to also perform well the next period. Persistence is stronger for VC firms than for LBO firms.

The application of the Freedom of Information Act (FOIA) in certain states in the United States has made certain performance data more readily available. Specifically, FOIA has required certain public agencies to disclose private-equity performance data directly on their websites.[106]

In the United Kingdom, the second largest market for private equity, more data has become available since the 2007 publication of the David Walker Guidelines for Disclosure and Transparency in Private Equity.[107]

Debate

Recording private equity

There is a debate around the distinction between private equity and foreign direct investment (FDI), and whether to treat them separately. The difference is blurred on account of private equity not entering the country through the stock market. Private equity generally flows to unlisted firms and to firms where the percentage of shares is smaller than the promoter- or investor-held shares (also known as free-floating shares). The main point of contention is that FDI is used solely for production, whereas in the case of private equity the investor can reclaim their money after a revaluation period and make investments in other financial assets. At present, most countries report private equity as a part of FDI.[108]

Cognitive bias

Private-equity decision-making has been shown to suffer from cognitive biases such as illusion of control and overconfidence.[109]

See also

- History of private equity and venture capital

- Private investment in public equity

- Publicly traded private equity

- Specialized investment fund

Organizations

- Institutional Limited Partners Association – advocacy organization for investors in private equity

- American Investment Council – advocacy and research organization for the industry

Notes

- Investments in private equity An Introduction to Private Equity, including differences in terminology. Archived 5 January 2016 at the Wayback Machine

- "Private Company Knowledge Bank". Privco.com. Retrieved 18 May 2012.

- Winning Strategy For Better Investment Decisions In Private Equity. USPEC, Retrieved 27 January 2020.

- Eileen Appelbaum and Rosemary Batt. Private Equity at Work, 2014.

- Duggan, Marie Christine. "Diamond Turning Innovation in the Age of Impatient Finance". Dollars & Sense – via www.academia.edu.

- Priem, Randy (2017). "Syndication of European buyouts and its effects on target-firm performance". Journal of Applied Corporate Finance. 28 (4). doi:10.1111/jacf.12209 (inactive 18 January 2021).CS1 maint: DOI inactive as of January 2021 (link)

- "Investopedia LBO Definition". Investopedia.com. 15 February 2009. Retrieved 18 May 2012.

- The balance between debt and added value. Financial Times, 29 September 2006

- "Frequently Asked Question: What is a tuck-in acquisition?". Investopedia. 30 September 2008. Retrieved 5 January 2013.

- "Add-On/Bolt-On Acquisition defined". PrivCo. Retrieved 5 January 2013.

- Note on Leveraged Buyouts. Tuck School of Business at Dartmouth: Center for Private Equity and Entrepreneurship, 2002. Accessed 20 February 2009

- Ulf Axelson, Tim Jenkinson, Per Strömberg, and Michael S. Weisbach. Leverage and Pricing in Buyouts: An Empirical Analysis Archived 27 March 2009 at the Wayback Machine. 28 August 2007

- Steven N. Kaplan and Per Strömberg. Leveraged Buyouts and Private Equity, Social Science Research Network, June 2008

- Trenwith Group "M&A Review," (Second Quarter, 2006)

- Peston, Robert (2008). Who runs Britain?. London: Hodder & Stoughton. pp. 28–67. ISBN 978-0-340-83942-3.

- "Zephyr Annual M&A Report: Global Private Equity, 2013" (PDF). Bureau van Dijk. Bureau van Dijk. 2014. Retrieved 22 May 2014.

- "Growth Capital Law and Legal Definition | USLegal, Inc". definitions.uslegal.com.

- "GROWTH CAPITAL MANAGEMENT". Archived from the original on 24 October 2011.

- Loewen, Jacoline (2008). Money Magnet: Attract Investors to Your Business: John Wiley & Sons. ISBN 978-0-470-15575-2.

- Driving Growth: How Private Equity Investments Strengthen American Companies Archived 7 November 2015 at the Wayback Machine. Private Equity Council. Accessed 20 February 2009

- When Private Mixes With Public; A Financing Technique Grows More Popular and Also Raises Concerns. The New York Times, 5 June 2004

- Gretchen Morgenson and Jenny Anderson. Secrets in the Pipeline. The New York Times, 13 August 2006

- Marks, Kenneth H. and Robbins, Larry E. The handbook of financing growth: strategies and capital structure. 2005

- Mezz Looking Up; It's Not A Long Way Down. Reuters Buyouts, 11 May 2006 "Buyouts". Archived from the original on 20 January 2012. Retrieved 15 October 2012.

- A higher yield Archived 12 November 2010 at the Wayback Machine. Smart Business Online, August 2009

- In the United Kingdom, venture capital is often used instead of private equity to describe the overall asset class and investment strategy described here as private equity.

- Joseph W. Bartlett. "What Is Venture Capital?" Archived 28 February 2008 at the Wayback Machine The Encyclopedia of Private Equity. Accessed 20 February 2009

- Joshua Lerner. Something Ventured, Something Gained. Harvard Business School, 24 July 2000. Retrieved 20 February 2009

- A Kink in Venture Capital’s Gold Chain. The New York Times, 7 October 2006

- An equation for valuation. Financial Post, 27 June 2009

- Paul A. Gompers. The Rise and Fall of Venture Capital Archived 27 September 2011 at the Wayback Machine. Graduate School of Business University of Chicago. Accessed 20 February 2009

- Equity Financing Globe & Mail, 4 March 2011

- The Principles of Venture Capital Archived 1 August 2013 at the Wayback Machine. National Venture Capital Association. Accessed 20 February 2009

- The turnaround business Archived 12 June 2013 at the Wayback Machine. AltAssets, 24 August 2001

- Guide to Distressed Debt. Private Equity International, 2007. Accessed 27 February 2009

- Distress investors take private equity cues. Reuters, 9 August 2007

- Bad News Is Good News: 'Distressed for Control' Investing. Wharton School of Business: Knowledge @ Wharton, 26 April 2006. Accessed 27 February 2009

- Distressed Private Equity: Spinning Hay into Gold. Harvard Business School: Working Knowledge, 16 February 2004. Accessed 27 February 2009

- "Distressed Private Equity". thehedgefundjournal.com. Retrieved 5 July 2020.

- The Private Equity Secondaries Market, A complete guide to its structure, operation and performance The Private Equity Secondaries Market, 2008

- Grabenwarter, Ulrich. Exposed to the J-Curve: Understanding and Managing Private Equity Fund Investments, 2005

- A discussion on the J-Curve in private equity Archived 12 June 2013 at the Wayback Machine. AltAssets, 2006

- A Secondary Market for Private Equity is Born, The Industry Standard, 28 August 2001

- Investors Scramble for Infrastructure (Financial News, 2008)

- Is It Time to Add a Parking Lot to Your Portfolio? (The New York Times, 2006

- [Buyout firms put energy infrastructure in pipeline] (MSN Money, 2008)

- "Merchant Banking: Past and Present". Fdic.gov. Archived from the original on 14 February 2008. Retrieved 18 May 2012.

- Joseph Haas (9 September 2013). "DRI Capital To Pursue Phase III Assets With Some of Its Third Royalty Fund". The Pink Sheet Daily.

- Wilson, John. The New Ventures, Inside the High Stakes World of Venture Capital.

- A Short (Sometimes Profitable) History of Private Equity, Wall Street Journal, 17 January 2012.

- "Who Made America? | Innovators | Georges Doriot". www.pbs.org.

- "Private Equity » Private equity, history and further development".

- "Joseph W. Bartlett, "What Is Venture Capital?"". Vcexperts.com. Archived from the original on 28 February 2008. Retrieved 18 May 2012.

- The Future of Securities Regulation speech by Brian G. Cartwright, General Counsel U.S. Securities and Exchange Commission. University of Pennsylvania Law School Institute for Law and Economics Philadelphia, Pennsylvania. 24 October 2007.

- On 21 January 1955, McLean Industries, Inc. purchased the capital stock of Pan Atlantic Steamship Corporation and Gulf Florida Terminal Company, Inc. from Waterman Steamship Corporation. In May McLean Industries, Inc. completed the acquisition of the common stock of Waterman Steamship Corporation from its founders and other stockholders.

- Marc Levinson, The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger, pp. 44–47 (Princeton Univ. Press 2006). The details of this transaction are set out in ICC Case No. MC-F-5976, McLean Trucking Company and Pan-Atlantic American Steamship Corporation—Investigation of Control, 8 July 1957.

- "Lewis B. Cullman '41 | Obituaries | Yale Alumni Magazine". yalealumnimagazine.com.

- Reier, Sharon; Tribune, International Herald (10 July 2004). "Book Report : CAN'T TAKE IT WITH YOU" – via NYTimes.com.

- Trehan, R. (2006). The History Of Leveraged Buyouts. 4 December 2006. Retrieved 22 May 2008

- [spam filter website: investmentu.com/research/private-equity-history.html The History of Private Equity] (Investment U, The Oxford Club

- Burrough, Bryan. Barbarians at the Gate. New York : Harper & Row, 1990, p. 133-136

- Taylor, Alexander L. "Buyout Binge". TIME magazine, 16 July 1984.

- David Carey and John E. Morris, King of Capital The Remarkable Rise, Fall, and Rise Again of Steve Schwarzman and Blackstone (Crown 2010), pp. 15–26

- Opler, T. and Titman, S. "The determinants of leveraged buyout activity: Free cash flow vs. financial distress costs." Journal of Finance, 1993.

- King of Capital, pp. 31–44

- 10 Questions for Carl Icahn by Barbara Kiviat, TIME magazine, 15 February 2007

- TWA – Death Of A Legend Archived 21 November 2008 at the Wayback Machine by Elaine X. Grant, St Louis Magazine, Oct 2005

- Game of Greed (TIME magazine, 1988)

- Wallace, Anise C. "Nabisco Refinance Plan Set." The New York Times, 16 July 1990.

- King of Capital, pp. 97–99

- Stone, Dan G. (1990). April Fools: An Insider's Account of the Rise and Collapse of Drexel Burnham. New York City: Donald I. Fine. ISBN 978-1-55611-228-7.

- Den of Thieves. Stewart, J. B. New York: Simon & Schuster, 1991. ISBN 0-671-63802-5.

- New Street Capital Inc. – Company Profile, Information, Business Description, History, Background Information on New Street Capital Inc. at ReferenceForBusiness.com

- SORKIN, ANDREW ROSS and ROZHON, TRACIE. "Three Firms Are Said to Buy Toys 'R' Us for $6 Billion ." The New York Times, 17 March 2005.

- ANDREW ROSS SORKIN and DANNY HAKIM. "Ford Said to Be Ready to Pursue a Hertz Sale." The New York Times, 8 September 2005

- PETERS, JEREMY W. "Ford Completes Sale of Hertz to 3 Firms." The New York Times, 13 September 2005

- SORKIN, ANDREW ROSS. "Sony-Led Group Makes a Late Bid to Wrest MGM From Time Warner." The New York Times, 14 September 2004

- "Capital Firms Agree to Buy SunGard Data in Cash Deal." Bloomberg L.P., 29 March 2005

- Samuelson, Robert J. "The Private Equity Boom". The Washington Post, 15 March 2007.

- Dow Jones Private Equity Analyst as referenced in U.S. private-equity funds break record Associated Press, 11 January 2007.

- Dow Jones Private Equity Analyst as referenced in Private equity fund raising up in 2007: report, Reuters, 8 January 2008.

- SORKIN, ANDREW ROSS. "HCA Buyout Highlights Era of Going Private." The New York Times, 25 July 2006.

- WERDIGIER, JULIA. "Equity Firm Wins Bidding for a Retailer, Alliance Boots." The New York Times, 25 April 2007

- Lonkevich, Dan and Klump, Edward. KKR, Texas Pacific Will Acquire TXU for $45 Billion Archived 13 June 2010 at the Wayback Machine Bloomberg, 26 February 2007.

- SORKIN, ANDREW ROSS and de la MERCED, MICHAEL J. "Private Equity Investors Hint at Cool Down." The New York Times, 26 June 2007

- SORKIN, ANDREW ROSS. "Sorting Through the Buyout Freezeout." The New York Times, 12 August 2007.

- Turmoil in the markets, The Economist 27 July 2007

- "Private equity deal making post-AIFMD: asset stripping rules". www.dirittobancario.it. 13 March 2014.

- "Private equity deal making post-AIFMD: notification and disclosure rules". www.dirittobancario.it. 31 March 2014.

- "Staying Private Longer: Why Go Public?". www.americanbar.org. Retrieved 22 April 2020.

- "Upcounsel".

- King of Capital, pp. 213–214

- M. Nicolas J. Firzli : ‘The New Drivers of Pension Investment in Private Equity’, Revue Analyse Financière, Q3 2014 – Issue N°52

- Per Stromberg:'The new demography of Private Equity', Master Thesis, Swedish Institute for Financial Research, Stockholm School of Economics Archived 4 March 2016 at the Wayback Machine

- "PEI 300" (PDF). PEI Media. Archived from the original (PDF) on 28 August 2017. Retrieved 20 August 2015.] from PEI Media

- "Invest Europe - The Voice of Private Capital". www.investeurope.eu. Retrieved 5 May 2017.

- "London-based PE funds". Askivy.net. Retrieved 18 May 2012.

- Private equity versus hedge funds, QuantNet, 9 July 2007.

- Understanding private equity strategies Archived 30 March 2012 at the Wayback Machine, QFinance, June 2008.

- Private Equity Report, 2012 Archived 23 April 2015 at the Wayback Machine. TheCityUK.

- "Why Rubenstein Believes SWFs May Become the Biggest Single Capital Source for Private Equity". Sovereign Wealth Fund Institute. 5 March 2014. Retrieved 8 January 2021.

- Kaplan, Steven Neil; Schoar, Antoinette (2005). "Private Equity Performance: Returns, Persistence, and Capital Flows". The Journal of Finance. 60 (4): 1791–1823. doi:10.1111/j.1540-6261.2005.00780.x. hdl:1721.1/5050. Retrieved 10 February 2012.

- Harris, Robert S.; Jenkinson, Tim; Kaplan, Steven N. (10 February 2012). "Private Equity Performance: What Do We Know?". Social Science Research Network. SSRN 1932316. Accessed 10 February 2012. Cite journal requires

|journal=(help) - Robinson, David T.; Sensoy, Berk A. (15 July 2011). "Private Equity in the 21st Century: Liquidity, Cash Flows and Performance from 1984–2010" (PDF). National Bureau of Economic Research. Retrieved 10 February 2012.

- "Academic pans PE returns, Real Deals". Realdeals.eu.com. 17 June 2011. Archived from the original on 23 May 2012. Retrieved 18 May 2012.

- In the United States, FOIA is individually legislated at the state level, and so disclosed private-equity performance data will vary widely. Notable examples of agencies that are mandated to disclose private-equity information include CalPERS, CalSTRS and Pennsylvania State Employees Retirement System and the Ohio Bureau of Workers' Compensation

- "Guidelines for Disclosure and Transparency in Private Equity" (PDF). Archived from the original (PDF) on 4 July 2008. Retrieved 4 January 2019.

- Private Equity and India's FDI boom Archived 6 May 2011 at the Wayback Machine. The Hindu Business Line, 1 May 2007

- S.X. Zhang & J. Cueto (2015). "The Study of Bias in Entrepreneurship". Entrepreneurship Theory and Practice. 41 (3): 419–454. doi:10.1111/etap.12212. S2CID 146617323.

Further reading

- David Stowell (2010). An Introduction to Investment Banks, Hedge Funds, and Private Equity: The New Paradigm. Academic Press.

- Lemke, Thomas P.; Lins, Gerald T.; Hoenig, Kathryn L.; Rube, Patricia S. (2013). Hedge Funds and Other Private Funds: Regulation and Compliance. Thomson West.

- Cendrowski, Harry; Martin, James P.; Petro, Louis W. (2008). Private Equity: History, Governance, and Operations. Hoboken: John Wiley & Sons. ISBN 978-0-470-17846-1.

- Kocis, James M.; Bachman, James C.; Long, Austin M.; Nickels, Craig J. (2009). Inside Private Equity: The Professional Investor's Handbook. Hoboken: John Wiley & Sons. ISBN 978-0-470-42189-5.

- Davidoff, Steven M. (2009). Gods at War: Shot-gun Takeovers, Government by Deal and the Private Equity Implosion. Hoboken: John Wiley & Sons. ISBN 978-0-470-43129-0.

- Davis, E. Philip; Steil, Benn (2001). Institutional Investors. MIT Press. ISBN 978-0-262-04192-8.

- Maxwell, Ray (2007). Private Equity Funds: A Practical Guide for Investors. New York: John Wiley & Sons. ISBN 978-0-470-02818-6.

- Leleux, Benoit; Hans van Swaay (2006). Growth at All Costs: Private Equity as Capitalism on Steroids. Basingstoke: Palgrave Macmillan. ISBN 978-1-4039-8634-4.

- Fraser-Sampson, Guy (2007). Private Equity as an Asset Class. Hoboken, NJ: John Wiley & Sons. ISBN 978-0-470-06645-4.

- Bassi, Iggy; Jeremy Grant (2006). Structuring European Private Equity. London: Euromoney Books. ISBN 978-1-84374-262-3.

- Thorsten, Gröne (2005). Private Equity in Germany – Evaluation of the Value Creation Potential for German Mid-Cap Companies. Stuttgart: Ibidem-Verl. ISBN 978-3-89821-620-3.

- Rosenbaum, Joshua; Joshua Pearl (2009). Investment Banking: Valuation, Leveraged Buyouts, and Mergers & Acquisitions. Hoboken, NJ: John Wiley & Sons. ISBN 978-0-470-44220-3.

- Lerner, Joshua (2000). Venture Capital and Private Equity: A Casebook. New York: John Wiley & Sons. ISBN 978-0-471-32286-3.

- Grabenwarter, Ulrich; Tom Weidig (2005). Exposed to the J Curve: Understanding and Managing Private Equity Fund Investments. London: Euromoney Institutional Investor. ISBN 978-1-84374-149-7.

- Loewen, Jacoline (2008). Money Magnet: Attract Investors to Your Business. Canada, Toronto: John Wiley & Sons. ISBN 978-0-470-15575-2.

- Private Inequity by James Surowiecki, The Financial Page, The New Yorker, 30 January 2012.

- Gilligan, John; Mike Wright (2020). Private Equity Demystified. 4th Edition. London: OUP. ISBN 978-0-198-86699-2.

- Gladstone, David; Laura Gladstone (2004). Venture Capital Investing, the complete handbook for investing in new businesses. Upper Saddle River, NJ: Pearson Education. ISBN 978-0-13-101885-3.

- Plant, Nicholas; Gajer, Paul; Rist, Steven. "Private Equity Transactions in the UK". Transaction Advisors. ISSN 2329-9134.

External links

![]() Media related to Private equity at Wikimedia Commons

Media related to Private equity at Wikimedia Commons

| Investment types |  | ||||||

|---|---|---|---|---|---|---|---|

| History | |||||||

| Terms and concepts |

| ||||||

| Investors | |||||||

| Related financial terms | |||||||

| |||||||