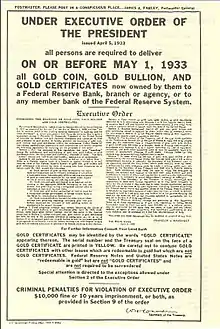

Executive Order 6102

Executive Order 6102 is an executive order signed on April 5, 1933, by US President Franklin D. Roosevelt "forbidding the hoarding of gold coin, gold bullion, and gold certificates within the continental United States." The executive order was made under the authority of the Trading with the Enemy Act of 1917, as amended by the Emergency Banking Act in March 1933.

| Forbidding the Hoarding of Gold Coin, Gold Bullion and Gold Certificates | |

| |

.jpg.webp) Saint Gaudens Double Eagle | |

Executive Order 6102 | |

| Type | Executive order |

|---|---|

| Executive Order number | 6102 |

| Signed by | Franklin Delano Roosevelt on 5 April 1933 |

| Summary | |

| |

The limitation on gold ownership in the United States was repealed after President Gerald Ford signed a bill legalizing private ownership of gold coins, bars, and certificates by an Act of Congress, codified in Pub.L. 93–373,[1] which went into effect December 31, 1974.

Rationale

The stated reason for the order was that hard times had caused "hoarding" of gold, stalling economic growth and worsened the depression.[2][3]

On April 6, 1933, The New York Times wrote, under the headline Hoarding of Gold, "The Executive Order issued by the President yesterday amplifies and particularizes his earlier warnings against hoarding. On March 6, taking advantage of a wartime statute that had not been repealed, he issued Presidential Proclamation 2039 that forbade the hoarding 'of gold or silver coin or bullion or currency', under penalty of $10,000 and/or up to five to ten years imprisonment."[4]

The main rationale behind the order was actually to remove the constraint on the Federal Reserve preventing it from increasing the money supply during the depression. The Federal Reserve Act (1913) required 40% gold backing of Federal Reserve Notes that were issued. By the late 1920s, the Federal Reserve had almost hit the limit of allowable credit, in the form of Federal Reserve demand notes, which could be backed by the gold in its possession (see Great Depression).

Effects

Executive Order 6102 required all persons to deliver on or before May 1, 1933, all but a small amount of gold coin, gold bullion, and gold certificates owned by them to the Federal Reserve in exchange for $20.67 (equivalent to $408 in 2019)[5] per troy ounce. Under the Trading with the Enemy Act of 1917, as amended by the recently passed Emergency Banking Act of March 9, 1933, a violation of the order was punishable by fine up to $10,000,(equivalent to $198,000 in 2019)[5] up to ten years in prison, or both.

The order specifically exempted "customary use in industry, profession or art," a provision that covered artists, jewelers, dentists, signmakers, etc.. The order also permitted any person to own up to $100 in gold coins, a face value equivalent to 5 troy ounces (160 g) of gold valued at approximately $10,000 in 2020. The same paragraph also exempted "gold coins having recognized special value to collectors of rare and unusual coins," which protected recognized gold coin collections from legal seizure and likely melting.

The price of gold from the Treasury for international transactions was then raised by the Gold Reserve Act to $35 an ounce (equivalent to $691 in 2019)[5]. The resulting profit that the government realized funded the Exchange Stabilization Fund, established by the 1934 Gold Reserve Act.

The regulations prescribed in the executive order were modified by Executive Order 6111 on April 20, 1933, both of which were ultimately revoked and superseded by Executive Orders 6260 and 6261 on August 28 and 29, 1933, respectively.[6]

Executive Order 6102 also led to the extreme rarity of the 1933 Double Eagle gold coin. The order caused all gold coin production to cease and all 1933 minted coins to be destroyed. About 20 illegal coins were stolen, leading to an outstanding US Secret Service warrant for arrest and confiscation of the coin. A legalized surviving coin sold for over $7.5 million in 2002, making it one of the most valuable coins in the world.[7]

Prosecutions

Numerous individuals and companies were prosecuted related to Roosevelt's Executive Order 6102. The prosecutions took place under the subsequent Executive Orders 6111,[8] 6260,[9] 6261[10] and the Gold Reserve Act of 1934.

There was a need to strengthen Executive Order 6102, as the one prosecution under the order was ruled invalid by Federal Judge John M. Woolsey, on the grounds that the order was signed by the President, instead of the Secretary of the Treasury as required.[11]

The circumstances of the case were that a New York attorney named Frederick Barber Campbell had one deposit at Chase National Bank of over 5,000 troy ounces (160 kg) of gold. When Campbell attempted to withdraw the gold, Chase refused, and Campbell sued Chase. A federal prosecutor then indicted Campbell on the following day (September 27, 1933) for failing to surrender his gold.[12] Ultimately, the prosecution of Campbell failed, but the authority of the federal government to seize gold was upheld, and Campbell's gold was confiscated.

The case was cause for the Roosevelt administration to issue a new order under the signature of the Secretary of the Treasury, Henry Morgenthau, Jr., Executive Orders 6260, 6261, related to the seizure of gold and the prosecution of gold hoarders. A few months later, Congress passed the Gold Reserve Act of 1934, which ratified Roosevelt's orders. A new set of Treasury regulations was issued providing civil penalties of confiscation of all gold and imposition of fines equal to double the value of the gold seized.

Prosecutions of US citizens and noncitizens followed the new orders, with a few notable cases:

Gus Farber, a diamond and jewelry merchant from San Francisco, was prosecuted for the sale of thirteen $20 gold coins without a license. Secret Service agents discovered the sale with the help of the buyer. Farber, his father, and 12 others were arrested in four American cities after a sting operation conducted by the Secret Service. The arrests took place simultaneously in New York and three California cities: San Francisco, San Jose, and Oakland. Morris Anolik was arrested in New York with $5,000 in U.S. and foreign gold coins; Dan Levin and Edward Friedman of San Jose were arrested with $15,000 in gold; Sam Nankin was arrested in Oakland; in San Francisco, nine men were arrested on charges of hoarding gold. In all, $24,000 in gold was seized by Secret Service Agents during the operation.[13]

David Baraban and his son Jacob owned a refining company. The Barabans' license to deal in unmelted scrap gold was revoked and so the Barabans operated their refining business under a license issued to a Minnie Sarch. The Barabans admitted that Minnie Sarch had nothing to do with the business and that she had obtained the license so that the Barabans could continue to deal in gold. The Barabans had a cigar box full of gold-filled scrap jewelry visible in one of the showcases. Government agents raided the Barabans' business and found another hidden box of US and foreign gold coins. The coins were seized and Baraban was charged with conspiracy to defraud the United States.[14]

Louis Ruffino was one individual indicted on three counts purporting to violations of the Trading with the Enemy Act of 1917, which restricted trade with countries hostile to the United States. Eventually, Ruffino appealed[15] the conviction to the Circuit Court of Appeals 9th District in 1940; however, the judgment of the lower courts was upheld based on the President's executive orders and the Gold Reserve Act of 1934. Ruffino, a resident of Sutter Creek in California-gold country, was convicted of possessing 78 ounces of gold and was sentenced to 6 months in jail, paid a $500 fine, and had his gold seized.[16]

Foreigners also had gold confiscated and were forced to accept paper money for their gold. The Uebersee Finanz-Korporation, a Swiss banking company, had $1,250,000 in gold coins for business use. The Uebersee Finanz-Korporation entrusted the gold to an American firm for safekeeping, and the Swiss were shocked to find that their gold was confiscated. The Swiss made appeals, but they were denied; they were entitled to paper money but not their gold. The Swiss company would have lost 40% of their gold's value if they had tried to buy the same amount of gold with the paper money that they received in exchange for their confiscated gold.[17]

Another type of de facto gold seizure occurred as a result of the various executive orders involving bonds, gold certificates and private contracts. Private contracts or bonds that were written in terms of gold were to be paid in paper currency instead of gold although all of the contracts and the bonds proclaimed that they were payable in gold, and at least one, the fourth Liberty Bond, was a federal instrument. The plaintiffs in all cases received paper money, instead of gold, despite the contracts' terms. The contracts and the bonds were written precisely to avoid currency debasement by requiring payment in gold coin. The paper money which was redeemable in gold was instead irredeemable based on Nortz v. United States, 294 U.S. 317 (1935). The consolidated Gold Clause Cases were the following:

- Perry v. United States, 294 U.S. 330 (1935)

- U.S. v. Bankers' Trust Co., 294 U.S. 240 (1935)[18]

- Norman v. Baltimore & Ohio R. Co., 294 U.S. 240 (1935)

- Nortz v. United States, 294 U.S. 317 (1935)

The Supreme Court upheld all seizures as constitutional, with Justices James Clark McReynolds, Willis Van Devanter, George Sutherland, and Pierce Butler dissenting.[19] The four justices were nicknamed the "Four Horsemen" by the press, as their conservative views were in opposition to Roosevelt's New Deal.

Subsequent events and abrogation

The Gold Reserve Act of 1934 made gold clauses unenforceable and authorized the President to establish the gold value of the dollar by proclamation. Immediately following its passage, Roosevelt changed the statutory price of gold from $20.67 to $35 per ounce, thereby devaluing the US dollar, which was based on gold. That price remained in effect until August 15, 1971, when President Richard Nixon announced that the US would no longer convert dollars to gold at a fixed value, thus abandoning the gold standard for foreign exchange (see Nixon Shock).

The private ownership of gold certificates was legalized in 1964, and they can be openly owned by collectors but are not redeemable in gold. The limitation on gold ownership in the US was repealed after President Gerald Ford signed a bill to "permit United States citizens to purchase, hold, sell, or otherwise deal with gold in the United States or abroad" with an act of Congress codified in Pub.L. 93–373,[20][21][22] which went into effect December 31, 1974. However, P. L. 93-373 did not repeal the Gold Repeal Joint Resolution,[23][24] which banned any contracts that specified payment in a fixed amount of money as gold or a fixed amount of gold. That is, contracts remained unenforceable if they used gold monetarily, rather than as a commodity of trade. However, an Act enacted on Oct. 28, 1977, Pub. L. No. 95-147, § 4(c), 91 Stat. 1227, 1229 (originally codified at 31 U.S.C. § 463 note, recodified as amended at 31 U.S.C. § 5118(d)(2)) amended the 1933 Joint Resolution to make it clear that parties could again include so-called gold clauses in contracts made after 1977.[25]

Hoax of safe deposit box seizures

According to a hoax, Roosevelt ordered all safe deposit boxes in the country seized and searched for gold by an official of the Internal Revenue Service. A typical example of the text of the alleged order reads:

By Executive Order Of The President of The United States, March 9, 1933.

By virtue of the authority vested in me by Section 5 (b) of the Act of October 6, 1917, as amended by Section 2 of the Act of March 9, 1933, in which Congress declared that a serious emergency exists, I as President, do declare that the national emergency still exists; that the continued private hoarding of gold and silver by subjects of the United States poses a grave threat to the peace, equal justice, and well-being of the United States; and that appropriate measures must be taken immediately to protect the interests of our people.

Therefore... I hereby proclaim that such gold and silver holdings are prohibited, and that all such coin, bullion or other possessions of gold and silver be tendered within fourteen days to agents of the Government... for compensation at the official price, in the legal tender of the Government.

All safe deposit boxes in banks or financial institutions have been sealed.... All sales or purchases or movements of such gold and silver... are hereby prohibited.

Your possession... and/or safe deposit box to store them is known by the government from bank and insurance records. Therefore... your vault box must remain sealed, and may only be opened in the presence of an agent of the Internal Revenue Service.

By lawful order..., the President of the United States.

The first known reference to the hoax was in the book After the Crash: Life In the New Great Depression.[26] The fake text refers only to gold, not to silver, which was added by 1998 to Internet references. It claims to be an executive order, but its text was written it to apply to specific individuals ("Your possession"), and so if the text originated from the government, it would have been sent to individuals, not published as an executive order. The first paragraph starts with the actual text of Executive Order 6102, then edits it slightly (changing "said national emergency" to "a national emergency" and "still continues to exist" to "still exists") and then adds apparently-invented text. The minor edits and the way that the real text and fake text are combined mid-sentence make it almost certainly an intentionally-designed hoax, rather than an accident.

Most of the text does not appear in the actual executive order.[27] In fact, safe deposit boxes held by individuals were not forcibly searched or seized under the order, and the few prosecutions that occurred in the 1930s for gold "hoarding" were executed under different statutes. One of the few such cases occurred in 1936, when a safe deposit box containing over 10,000 troy ounces (310 kg) of gold belonging to Zelik Josefowitz, who was not a US citizen, was seized with a search warrant as part of a prosecution for tax evasion.[28]

The US Treasury also came into possession of a large number of safe deposit boxes due to bank failures. During the 1930s, over 3000 banks failed, and the contents of their safe deposit boxes were remanded to the custody of the Treasury. If no one claimed the box, it remained in the possession of the Treasury. In October 1981, there were 1605 cardboard cartons in the basement of the Treasury, each carton containing the contents of one unclaimed safe deposit box.[29]

Similar laws in other countries

In Australia, Part IV of the Banking Act 1959 allows the Commonwealth government to seize private citizens' gold in return for paper money where the Governor-General is satisfied that it is expedient so to do, for the protection of the currency or of the public credit of the Commonwealth.[30] On January 30, 1976, the operation of that part of the Act was suspended.[31]

See also

- Causes of the Great Depression

- Emergency Banking Act March 9, 1933

- Executive Order 6814, a similar Order pertaining to silver, signed in 1934

- Fiat money

- Gold

- Gold Clause Cases

- Great Contraction

- Gold Standard

References

- ,

- West, Howard (2018). The 13th Chapter: Humanity's Final Chapter. Howard West Books. p. 121. ISBN 978-0-557-67854-9.

- "Hoarders Face Heavy Penalty Under U.S. Writ". Chattanooga Daily Times. April 6, 1933. p. 1. Retrieved December 19, 2019.

- "Hoarding of Gold". The New York Times. April 6, 1933. p. 16.

- Federal Reserve Bank of Minneapolis. "Consumer Price Index (estimate) 1800–". Retrieved January 1, 2020.

- Roosevelt, Franklin D. (1938). Public Papers and Addresses of Franklin D. Roosevelt, Volume II, The Year of Crisis, 1933. New York: Random House. p. 352. OCLC 690922370.

- Suzan, Clarke (2013-01-29). "Rare silver dollar coin sets world record auction price". ABC News. Retrieved 4 March 2014.

- Wikisource:Executive Order 6111

- Wikisource:Executive Order 6260

- Wikisource:Executive Order 6261

- "Sequels". Time. November 27, 1933. Archived from the original on November 15, 2009.

- "Gold Indictment No. 1". Time. October 9, 1933.

- "Bootleg Gold Ring Smashed in California: 13 Men Are Accused Of Violating Federal Restrictions". The Evening Independent. April 13, 1939.

- "FindACase: United States v. Scrap". Ny.findacase.com. 1938-01-10. Retrieved 2013-12-30.

- "Archived copy" (PDF). Archived from the original (PDF) on 2013-08-15. Retrieved 2013-04-26.CS1 maint: archived copy as title (link)

- "Ruffino V. United States". Leagle.com. Retrieved 2013-12-30.

- "Uebersee Finanz-Korporation, Etc. V. Rosen". Leagle.com. Retrieved 2013-12-30.

- "FindLaw | Cases and Codes". Caselaw.lp.findlaw.com. Retrieved 2013-12-30.

- "Perry v. United States - 294 U.S. 330 (1935): Justia US Supreme Court Center". Supreme.justia.com. Retrieved 2013-12-30.

- Public Law 93-373 (PDF), Government Printing Office, August 14, 1974

- United States Congress (August 14, 1974). "An Act to provide for increased participation by the United States in the International Development Association and to permit United States citizens to purchase, hold, sell, or otherwise deal with gold in the United States or abroad". Pub.L. 93–373.

- "Statements of Policy: Gold". FDIC Law, Regulations, Related Acts. Federal Deposit Insurance Corporation.

- Wikisource:Gold Repeal Joint Resolution

- Norman v. Baltimore & Ohio Railroad Co., 294 U.S. 240 (1935).

- 216 Jamaica Avenue, LLC v. S & R Playhouse Realty Co., 540 F.3d 433 (United States Court of Appeals, Sixth Circuit 2008).

- Michael Haga. After the Crash: Life In the New Great Depression, Acclaim Publishing Co., 1996, pp. 193-194.

- Roosevelt, Franklin D. (April 5, 1933). "Executive Order 6102: Requiring Gold Coin, Gold Bullion and Gold Certificates to Be Delivered to the Government".

- "Josefowitz Gold". Time. March 2, 1936.

- Apcar, Leonard M. (October 15, 1981). "Treasury's Vaults Disgorge Treasures from the Depression: Memorabilia, Valuables Taken When Banks Were Closed May Be Opened For Claims". Wall Street Journal.

- Parliament of Australia (1959). "Banking Act 1959". Commonwealth Consolidated Acts. Commonwealth of Australia.

- Suchecki, Bron (August 4, 2008). "A History of Gold Controls in Australia". Gold Chat. Self-published.

External links

| Wikisource has original text related to this article: |

- Text of Executive Order 6102 from The American Presidency Project.

- 1933 Audio of FDR's Banking Crisis Fireside Chat