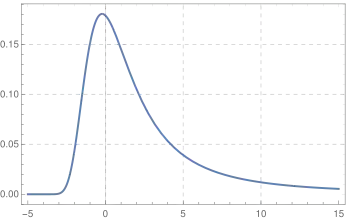

Landau distribution

In probability theory, the Landau distribution[1] is a probability distribution named after Lev Landau. Because of the distribution's "fat" tail, the moments of the distribution, like mean or variance, are undefined. The distribution is a particular case of stable distribution.

|

Probability density function  | |||

| Parameters | — location parameter | ||

|---|---|---|---|

| Support | |||

| Mean | Undefined | ||

| Variance | Undefined | ||

| MGF | Undefined | ||

| CF | |||

Definition

The probability density function, as written originally by Landau, is defined by the complex integral:

where a is an arbitrary positive real number, meaning that the integration path can be any parallel to the imaginary axis, intersecting the real positive semi-axis, and refers to the natural logarithm.

The following real integral is equivalent to the above:

The full family of Landau distributions is obtained by extending the original distribution to a location-scale family of stable distributions with parameters and ,[2] with characteristic function:[3]

where and , which yields a density function:

Let us note that the original form of is obtained for and , while the following is an approximation[4] of for and :

Related distributions

- If then .

- The Landau distribution is a stable distribution with stability parameter and skewness parameter both equal to 1.

References

- Landau, L. (1944). "On the energy loss of fast particles by ionization". J. Phys. (USSR). 8: 201.

- Gentle, James E. (2003). Random Number Generation and Monte Carlo Methods. Statistics and Computing (2nd ed.). New York, NY: Springer. p. 196. doi:10.1007/b97336. ISBN 978-0-387-00178-4.

- Zolotarev, V.M. (1986). One-dimensional stable distributions. Providence, R.I.: American Mathematical Society. ISBN 0-8218-4519-5.

- Behrens, S. E.; Melissinos, A.C. Univ. of Rochester Preprint UR-776 (1981).