Taxation in Spain

Taxes in Spain are levied by national (central), regional and local governments. Tax revenue in Spain stood at 36.3% of GDP in 2013.[1] A wide range of taxes are levied on different sources, the most important ones being income tax, social security contributions, corporate tax, value added tax; some of them are applied at national level and others at national and regional levels. Most national and regional taxes are collected by the Agencia Estatal de Administración Tributaria which is the bureau responsible for collecting taxes at the national level. Other minor taxes like property transfer tax (regional), real estate property tax (local), road tax (local) are collected directly by regional or local administrations. Four historical territories or foral provinces (Araba/Álava, Bizkaia, Gipuzkoa and Navarre) collect all national and regional taxes themselves and subsequently transfer the portion due to central Government after two negotiations called Concierto (in which the first three territories, that conform the Basque Autonomous Community, agree their defense jointly) and the Convenio (in which the territory and Community of Navarre defense itself alone). The tax year in Spain follows the calendar year. The tax collection method depends on the tax; some of them are collected by self-assessment, but others (i.e. income tax) follow a system of pay-as-you-earn tax with monthly withholdings that follow a self-assessment at the end of the term.

| Taxation |

|---|

|

| An aspect of fiscal policy |

Income tax

Personal income tax in Spain, known as IRPF, was introduced in 1900. It represents nearly 38% of government revenues.[2] Since 2007, the responsibility for regulating and collecting personal income tax has been decentralized, the autonomous regions being responsible for collecting 50% of tax revenue (although all the returns and amounts are actually received by the central tax authority on their behalf). A single national rate applies per taxation band for the whole national portion of the income tax. Tax rates on the regional portion vary between regions, Madrid having the lowest and Catalonia the highest. Tax is withheld by the employer monthly on behalf of the tax authority. Tax returns are submitted between April and June of the following year and refunds are normally paid between May and July, however the Government has until the end of the year to liquidate before the tax payer has a right to interest for the outstanding money: any payments not paid by this date are paid with interest from the beginning of the next year.

As in other jurisdictions income tax is payable by both residents and non-residents with different rates applying. Individual residents are subject to personal income tax (IRPF) based on their income from around the globe. Non-residents are subject to IRPF only on their Spanish-sourced income.[3] Residence status must be established when filing a Spanish tax return and has consequences for the amount of tax due. The rules are complex.[4] Spain considers any alien to be resident if they were living in Spain for more than 183 days in the tax year. Sporadic periods of time outside of Spain are not counted towards establishing oneself as non-resident for tax purposes. An alien is also considered resident if s/he has a spouse or underage child who are residents, as well as any alien who has their main economic centre in Spain. When there is a residence conflict double taxation agreement must be checked.

Allowances and deductions

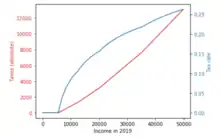

Some amounts are subtracted from the income tax base before the rate is applied. Allowances are adjusted annually by law. Allowances vary depending on whether the income is from labor, the tax payer is single or lives with elderly relatives or dependants, challenge conditions of the tax payer or those they live with, the autonomous community where they live, and other issues. Also, the amount may be reduced by declaring income with your spouse if you are married and some expenditures (like contributions to unions, personal pension funds, etc.). The figures given below are valid for the year 2019.[5]

The personal tax allowance differs depending on age. For the year 2019 under 65s the personal tax allowance is €5,550. Individuals aged between 65 and 75 are allowed a €6,700 personal allowance. Anyone above 75 receives the highest personal allowance at €8,100.

There is an elderly relative allowance which lowers the taxable income and applies to those tax payers who live with relatives older than 65 (or with relatives of any age with a disability graded at 33% or more) who do not have income themselves. This allowance is €1,150 if the relative is aged up to 75 and €2,550 above the age of 75.

There is also a dependants allowance which also lowers the taxable income base. It applies to tax payers who live with dependants younger than 25 (or with dependants of any age with a disability graded at 33% or more). For the first dependent, the allowance is €2,400. The allowance for the second dependent is €2,700, the allowance for the third dependent is €4,000, and each further child has an allowance of €4,400. In addition to dependant allowances, there is a maternity allowance which is €1,200 for each child under the age of 3.

There are also other reductions and deductions applicable for expenditures and housing (home rental and purchasing). The exact amount of the deduction depends on the amount of the expenditure though it is topped.

Some autonomous communities (like Cantabria, Castilla-La Mancha and Madrid) have different allowances for their own share of the income tax and also establish their own deductions.

Retired expatriates living in Spain who receive an income within Spain for tax purposes and a pension from their native country will need to calculate their income tax[6] and allowances by first identifying their marginal rate of income tax. This can be quite complex given the differing tax rates and thresholds within specific tax regions and variances in allowances.

Current rates

Once the gross income has been reduced by the legal allowances, reductions, and deductions, the taxpayer has to apply the rate to find out the actual tax.

As of January 1, 2015, the income tax has been reformed and simplified. It's important to note that these rates vary between each region. The rates shown below apply to the Community of Madrid. The communities of Andalusia and Catalonia apply a higher regional income tax than Madrid. The top rate of income tax in Andalusia and Catalonia is 49%.

| From (euros) | Up to (euros) | Tax Rate |

|---|---|---|

| €0 | €12,450 | 19% |

| €12,450 | €20,200 | 24% |

| €20,200 | €35,200 | 30% |

| €35,200 | €60,000 | 37% |

| €60,000 & Above | 45% | |

It's also noteworthy that these rates apply to the general income. Some kinds of income, like income bound to saving accounts, have different rates.

Tax on investment income

- Interest, coupon, bonds, insurance and dividends are generally withheld at 21% rate, but are added to savings base and taxed at savings scale. The first 1,500 € of dividends are exempt (since 2015 this exemption does not apply).

- Long term (+1 year) capital gains on: stocks, investment funds and real estate, are also taxed at savings scale.

- Short term (-1 year) capital gains are taxed at general scale (24,75%-52%). Since 2015 short and long term capital gains are taxed at savings scale.

Savings scale 2014

* up to 6,000 €: 21% * from 6,000 to 24,000 €: 25% * over 24,000 €: 27%

Savings scale 2015/2016

* up to 6,000 €: 20%/19% * from 6,000 to 50,000 €: 22%/21% * over 50,000 €: 24%/23%

Value added tax

VAT (IVA in Spanish: impuesto sobre el valor añadido or impuesto sobre el valor agregado) is due on any supply of goods or services sold in Spain. The current normal rate is 21% which applies to all goods which do not qualify for a reduced rate or are exempt. There are two lower rates of 10% and 4%. The 10% rate is payable on most drinks, hotel services and cultural events. The 4% rate is payable on food, books and medicines.[7] An EU directive means that all countries of the European Union have VAT. All exempt goods and services are listed below.

- Education provided by the state

- Tutoring

- Sporting services

- Cultural services

- Insurance

- Postal stamps

- Artists, writers and composers

As of January 1, 2013, new properties are taxed at the reduced rate of 10%. Second-hand properties are not subject to VAT, but a transfer tax, known as Impuestos sobre Transmisiones Patrimoniales or ITP. The tax is levied by the autonomous regional governments and therefore varies by region. The rate varies from 6% to 8%.[7]

Corporate tax

As of January 1, 2015, the corporate tax rate is 28%. In 2016 the tax will be further reduced to 25%. There is a lower tax rate for newly formed companies. The rate, which was introduced in 2015, is set at 15% for the first 2 years in which the company obtains taxable profit.[8]

In the Canary Islands, you have access to 4% Income Taxes if you enter into the Canarian Special Zone (ZEC).

Social Security contributions

Most sorts of employment income earned are subject to social security contributions, by both the employee and the employer. The standard rate for the employee is 6.35%. The employer pays what corresponds to 29.90% of the employee salary. The current maximum monthly Social Security base is EUR3,596.98 (2015). Any income exceeding that maximum base is not subject to both employee and employer contributions.[9]

References

- "Tax GDP".

- "Spanish Tax Authority Tax Report 2013". Archived from the original on 5 June 2015. Retrieved 1 June 2015.

- "Taxation in Spain". Moving to Valencia. Retrieved 13 July 2016.

- Tax Residence concept. http://jullastres.es/wordpress/?p=400

- "Tax-free thresholds, reductions and deductions on the Personal Income Tax". Retrieved 17 August 2019.

- "Spanish Income Tax Calculator 2017/18". iCalculator - Spanish Income Tax Calculator 2017/18. Retrieved 2017-11-07.

- "Guide to company tax in Spain for 2020". www.spainaccountants.com.

- "Social Security in spain KPMG".