Taxation in New Zealand

Taxes in New Zealand are collected at a national level by the Inland Revenue Department (IRD) on behalf of the Government of New Zealand. National taxes are levied on personal and business income, and on the supply of goods and services. There is no capital gains tax, although certain "gains" such as profits on the sale of patent rights are deemed to be income – income tax does apply to property transactions in certain circumstances, particularly speculation. There are currently no land taxes, but local property taxes (rates) are managed and collected by local authorities. Some goods and services carry a specific tax, referred to as an excise or a duty, such as alcohol excise or gaming duty. These are collected by a range of government agencies such as the New Zealand Customs Service. There is no social security (payroll) tax.

| Taxation |

|---|

|

| An aspect of fiscal policy |

New Zealand went through a major program of tax reform in the 1980s. The top marginal rate of income tax was reduced from 66% to 33% (changed to 39% in April 2000, 38% in April 2009 and 33% on 1 October 2010) and corporate income tax rate from 48% to 28% (changed to 30% in 2008 and to 28% on 1 October 2010). Goods and services tax was introduced, initially at a rate of 10% (then 12.5% and now 15%, as of 1 October 2010). Land taxes were abolished in 1992.[1]

Tax reform continues in New Zealand. Issues include:

Individual income tax

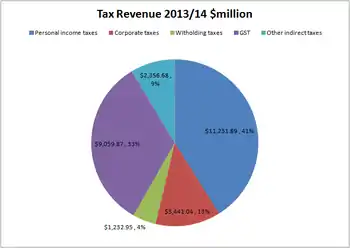

New Zealand residents are liable for tax on their worldwide taxable income. In 2005–06, 43% of the New Zealand Government's core revenue ($22.9bn) came from individuals' income taxes.[5]

Types of taxable income

- salary and wages

- business and self-employed income

- income from investments (interest, dividends, certain property transactions,[6] etc.)

- rental income

- overseas income (including income from an overseas pension)

Tax rates

Income tax varies dependent on income levels in any specific tax year (personal tax years run from 1 April to 31 March).

2017–2018

| Income | Tax rate | Effective tax rate | Max tax of bracket | Cumulative tax |

|---|---|---|---|---|

| $0 – $14,000 | 10.5% | 10.5% | $1,470 | $1,470 |

| $14,001 – $48,000 | 17.5% | 10.5 - 15.5% | $5,950 | $7,420 |

| $48,001 – $70,000 | 30% | 15.5 - 20.0% | $6,600 | $14,020 |

| Over $70,000 | 33% | 20.0 - 33.0% | $14,020 + 33% | |

| No-notification rate | 48% | 45% |

Rates are for the tax year 1 April 2017 to 31 March 2018, and are based on tax code M (primary income without student loan) and excludes the ACC earners' levy. The earners' levy rate (including GST) for the period 1 April 2017 to 31 March 2018 is 1.39% ($1.39 per $100).[7][8]

In New Zealand, the income is taxed by the amount that falls within each tax bracket. For example, persons who earn $70,000 will pay only 30% on the amount that falls between $48,001 and $70,000 rather than paying on the full $70,000. Consequently, the corresponding income tax for that specific income will accumulate to $14,020— which comes to an overall effective tax rate of 20.02% of the entire amount.

Tax credits

The amount of tax actually payable can be reduced by claiming tax credits, e.g. for donations, childcare and housekeeper, independent earners, and payroll donations.[9] Credits on income under $9,880 and for children were removed effective from 1 April 2013.[10]

Tax deducted at source

In most cases employers deduct the relevant amount of income tax from salary and wages prior to these being paid to the individual. This system, known as pay-as-you-earn, or PAYE, was introduced in 1958, prior to which employees paid tax annually.

In addition, banks and other financial institutions deduct the relevant amount of income tax on interest and dividends as these are earned. This withholding tax is known as either resident withholding tax[11](RWT) or non-resident withholding tax[12](NRWT), depending on the status of the lender; NRWT is at a higher rate.

At the end of each tax year, individuals who may not have paid the correct amount of income tax are required to submit a personal tax summary, to allow the IRD to calculate any under or overpayment of tax made during the year.

Double taxation agreements

Individuals who are tax resident in more than one country may be liable to pay tax more than once on the same income. New Zealand has double taxation agreements with various countries that set out which country will tax specific types of income.[13]

| Australia | India | Singapore |

| Austria | Indonesia | South Africa |

| Belgium | Ireland | Spain |

| Canada | Italy | Sweden |

| Chile | Japan | Switzerland |

| China | Korea | Taiwan |

| Czech Republic | Malaysia | Thailand |

| Denmark | Mexico | Turkey |

| Fiji | Netherlands | United Arab Emirates |

| Finland | Norway | United Kingdom |

| France | Philippines | United States of America |

| Germany | Poland | |

| Hong Kong | Russian Federation |

Some agreements protect pension payments as well. The agreement with the United States, for example, prohibits New Zealand from taxing American social security or government pension payments, and the reverse is also true.[14]

ACC earner's levy

All employees pay an earner's levy to cover the cost of non-work related injuries. It is collected by Inland Revenue on behalf of the Accident Compensation Corporation (ACC).

The earner's levy is payable on salary and wages plus any other income that is subject to PAYE, for example overtime, bonuses or holiday pay. The levy is 1.39% for the year from 1 April 2017 to 31 March 2018. It is payable on income up to $124,053.[15]

Capital gains tax

New Zealand does not have a capital gains tax.

A bright line test on property speculation was introduced on 1 October 2015, specifying certain purchases and sales of property as income (and thus taxed at the seller's income tax rate). The test does not apply to the family home, death estate, or property sold as part of a relationship settlement. The main aim of the test is to collect money off property speculation – originally houses bought and sold within two years were subject to the tax.[16] In 2018 the two-year threshold was expanded to five years. The proceeds from properties bought and sold within five years will be treated as income for tax purposes, subject to limits around family homes, etc.[17]

Generally profits made from frequent stock trading will be deemed taxable income.[18]

Business taxes

Business income tax

Businesses in New Zealand pay income tax on their net profit earned in any specific tax year. For most businesses the tax year runs from 1 April to 31 March but businesses can apply to the IRD for this to be changed.

A provisional tax payer is a person or a company that had a residual income tax of more than $2500 in the previous financial year. There are three options for paying provisional tax; standard method, estimated method and GST Ratio option.

- Under the standard method provisional tax payers make three provisional tax installments through the year based on the previous years tax liability.[19]

- The standard method is the most common method. However a provisional tax payer can choose to estimate their provisional tax payments. Estimation allows the business owner to pay less or more tax depending on how they think their business is performing. Any underpayment is subject to interest, and no interest is paid on over payment, so it is important that they estimate their profit accurately.[19]

- A provisional tax payer can also pay provisional tax using the GST ratio option. This is based on what your previous year's residual tax liability was and what your GST Taxable supplies were for that year. You then apply this percentage to your current period GST return. Under this option you pay provisional tax at the same time as you pay GST.[20]

At the end of the year the business files a tax return (due on the following 7 July for businesses with a tax year ending 31 March) and any under or overpayment is then calculated. Tax pooling was introduced in 2003 to remove some of the worry associated with estimating provisional tax payments by allowing businesses to pool their payments together so the underpayments by some can be offset by the overpayments of others to reduce/enhance the interest they pay/receive.[21][22]

Companies pay income tax at 28% on profits.[23] Tax rates for individuals operating as a business (that is, individuals who are self-employed) are the same as for employees.[24] (See individual tax rates, above.)

Goods and Services Tax

Goods and services tax (GST) is an indirect tax introduced in New Zealand in 1986. This represented a major change in New Zealand taxation policy as until this point almost all revenue had been raised via direct taxes. GST makes up 24% of the New Zealand Government's core revenue as of 2013.[25]

Most products or services sold in New Zealand incur GST at a rate of 15%. The main exceptions are financial services (e.g. banking and life insurance) and the export of goods and services overseas.

All businesses are required to register for GST once their turnover exceeds (or is likely to exceed) $60,000 per annum.[26] Once registered, businesses charge GST on all goods and services they supply and can reclaim any GST they have been charged on goods and services they have purchased.

Fringe benefit tax

Employers are liable to pay fringe benefit tax (FBT) on benefits given to employees in addition to their salary or wages (e.g. motor vehicles or low interest loans).[27] There are several methods available for calculating FBT liability, including an option of paying a flat rate of 49.25% on all benefits provided.[28]

Excise duties

Excise or duty is charged on a number of products, including alcohol products, tobacco products, and some fuels.[29]

Land taxes

New Zealand makes a distinction between "land taxes" and "property taxes". The traditional concept of property tax may choose to apply the same rate both to improvement values and to land values. A pure land tax exempts improvement values from taxation altogether and taxes only land values. A graded, dual-rate, or split-rate property tax applies a lower rate to improvement values. The term "land tax valuation" is used to represent both its pure and partial forms.[30] Conceptually, a property tax is a proxy for income tax - rightly or wrongly presuming that a certain level of property holdings indicate a certain ability to pay taxes on a regular basis. In contrast, an LVT applies to the land itself – taking into account its scarcity, immovability and centrality to human activity.[31]

Although the Land Tax Abolition Act (1990) which took effect from 31 March 1992 abolished New Zealand's land tax, a land tax was the very first direct tax ever imposed on New Zealanders, by the Land Tax Act (1878). A property tax followed the next year (per the Property Tax Act 1879). When first enacted, this charged a rate of one penny in the pound (i.e. 1/240th or 0.4%), but a massive £500 exemption applied, exempting most people from tax liability.

The land tax initially provided a major proportion of government revenue. In 1895 it made up 76% of the total land and income tax revenue received by the government.[32] In 1960 land tax contributed 6% of direct tax revenues, and by 1967, in a report recommending the abolition of land taxes, a committee chaired by Auckland accountant Lewis Ross noted that a mere 0.5% of total government revenue now came from land taxes. The government did not act on the Ross recommendation to abolish land taxes.

By 1982 only 5% of total land value was taxed, and land taxes were also thought to be duplicative due to their similarity to local-authority property-rate levies, with property taxes (rates) making up 57% of local-government income by 2001.[33]

The economic reforming zeal of the Labour government elected in 1984 saw a move away from taxes on capital in all forms, and in 1990 Parliament passed the Land Tax Abolition Act (1990),[34] ending New Zealand's history of central government taxing land. There has been talk of revisiting the concept of a land tax, but nothing substantive has eventuated.[35]

See also

- Tax Working Group

- Absentee Tax, historical

References

- https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2841132 at page 573

- "NZ Government discussion document on business taxes" (PDF). ird.govt.nz. Archived from the original (PDF) on 3 October 2006. Retrieved 5 April 2018.

- "NZ Government discussion document on taxation of investment income". ird.govt.nz. Archived from the original on 9 September 2006. Retrieved 5 April 2018.

- "NZ Government media release on forthcoming international tax review". ird.govt.nz. Archived from the original on 3 October 2006. Retrieved 5 April 2018.

- "Archived copy". Archived from the original on 18 September 2006. Retrieved 2 September 2006.CS1 maint: archived copy as title (link) Key facts for taxpayers from the NZ Treasury website

- "Tax and your property transactions" (PDF). Inland Revenue Department. 11 December 2014.

- http://www.ird.govt.nz/how-to/taxrates-codes/rates/ Income tax rates for individuals from the IRD website

- http://www.ird.govt.nz/income-tax-individual/different-income-taxed/salaries-wages/acc/iit-salaries-acc.html ACC earners' levy on income from personal effort

- Tax credits (Individual income tax). Ird.govt.nz (24 August 2009). Retrieved on 19 August 2011.

- "Budget 2012 announcements". Inland Revenue Department. 30 May 2012. Retrieved 28 November 2012.

- "Resident withholding tax".

- "NRWT (Non-resident withholding tax)". Inland Revenue. Retrieved 5 April 2018.

- http://www.ird.govt.nz/yoursituation-nonres/double-tax/ Double tax agreements from the IRD website

- "(See Article 18, Pensions and Annuities)" (PDF). irs.gov. Retrieved 5 April 2018.

- "Te tāke moni whiwhi mō ngā tāngata takitahi Income tax for individuals". Retrieved 19 April 2017.

- "Govt to tighten tax on capital gains". Radio New Zealand. 17 May 2015. Retrieved 1 June 2015.

- "Selling your house". New Zealand government. Retrieved 13 September 2018.

- "Capital Gains Tax New Zealand: What You Should Know | Canstar Blue". Canstar Blue. 16 February 2016. Retrieved 29 October 2020.

- http://www.nztax.net/node/45.html Provisional Tax Breakdown

- http://www.nztax.net/node/45.html GST Ratio Option

- "Pool system designed to ease taxing interest rates". The New Zealand Herald. 12 June 2003. ISSN 1170-0777. Retrieved 7 February 2017.

- "Tax policy news - 13 June 2003 - Tax pooling launched". taxpolicy.ird.govt.nz. Retrieved 7 February 2017.

- http://www.ird.govt.nz/business-income-tax/paying-tax/tax-rates/bit-taxrates-companytax.html Taxing companies from the IRD website

- http://www.ird.govt.nz/business-income-tax/paying-tax/tax-rates/bit-taxrates-soletradertax.html Taxing sole traders from the IRD website

- "Common questions about GST from the IRD website". ird.govt.nz. Archived from the original on 24 August 2006. Retrieved 5 April 2018.

- "Fringe benefit tax". Inland Revenue. Retrieved 5 April 2018.

- "Fringe benefit tax rates". Inland Revenue.

- "Archived copy". Archived from the original on 22 March 2012. Retrieved 21 March 2012.CS1 maint: archived copy as title (link)

- Richard F Dye and Richard W England, "The Principles and Promises of Land Value Taxation" in Richard F Dye and Richard W England (eds), Land Value Taxation: Theory, Evidence, and Practice (Lincoln Institute of Land Policy, 2009) 3, 4 n 1.

- https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2841132 p 575

- Taxation in New Zealand: Report of the Taxation Review Committee (Government Printer, 1967) ("Ross Report") 410.

- G Bush, "Local Government", in R Miller (ed), New Zealand Government and Politics (Oxford University Press, 2003) 161, 164 .

- "Land Tax Abolition Act 1990". New Zealand Legislation. Retrieved 6 December 2019.

- Victoria University of Wellington Tax Working Group, A Tax System for New Zealand’s Future: Report of the Victoria University of Wellington Tax Working Group (Centre for Accounting, Governance and Taxation Research, Victoria University of Wellington, 2010) ("Tax Working Group") and also, for example, International Monetary Fund, New Zealand: 2011 Article IV Consultation (International Monetary Fund, 2011) 14.